30th Apr 2026 07:00

FOR IMMEDIATE RELEASE

30 April 2026

Predator Oil & Gas Holdings Plc / Index: LSE / Epic: PRD / Sector: Oil & Gas

Predator Oil & Gas Holdings Plc

("Predator" or the "Company" and together with its subsidiaries "the Group")

Financial Statements for the Year Ended 31 December 2025

Predator Oil & Gas Holdings Plc (LSE: PRD), the Jersey based Oil and Gas Company with hydrocarbon operations focussed on production in Trinidad and appraisal and near-term development in Morocco, is pleased to announce its audited financial statements for the year ended 31 December 2025, extracts of which are set out below.

The Company's Annual Report is available to shareholders to download from the Company's website at www.predatoroilandgas.com. In line with ESG best practice no hard copies of the Annual Report will be printed.

In addition, a copy of the 2025 Annual Report will be uploaded to the National Storage Mechanism and will be available for viewing at

https://data.fca.org.uk/#/nsm/nationalstoragemechanism.

The financial information set out below does not constitute the Company's statutory accounts for the year ending 31 December 2025.

Highlights of Financial Results for 2025

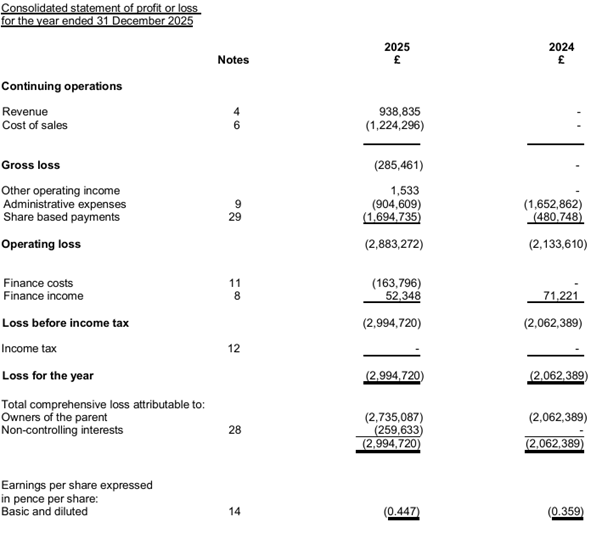

· GBP 938,835 net petroleum sales revenue.

· The Company has no debt OR outstanding directors' loans as of 31 December 2025.

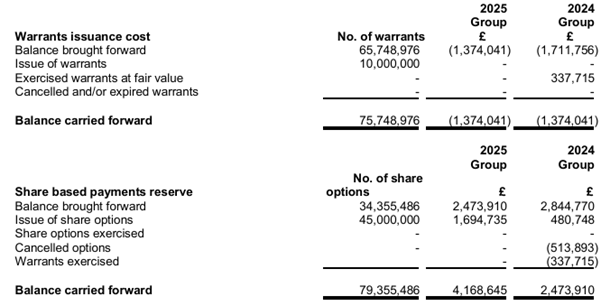

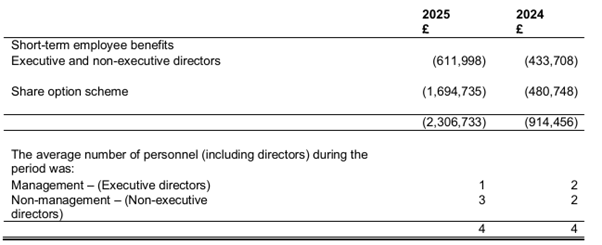

· Loss from operations of GBP 2,994,720 (GBP 2,062,389 in 2024). The increase in gross operating loss is primarily attributable to the higher number of share options issued in 2025, contributing to a share-based payment charge of GBP 1,694,735 (GBP 480,748 in 2024).

· Administrative expenses for the period to 31 December 2025 were GBP 904,609 (GBP 1,652,862 for the period to 31 December 2024).

Prudent management of corporate overheads was achieved despite increased activity which saw: the acquisition of 3 additional producing oil fields in Trinidad; the execution of a Master Services Agreement with NABI Construction to eliminate exposure to operating expenses and licence work programme commitments; and Group re-structuring to preserve inherited tax losses in the companies holding the acquired assets.

Actions taken in 2025 have increased the potential for future divestment options following the implementation of a programme for production enhancement and reduction in field operating costs.

· Technical services consultancy fees reduced to GBP 144,871 (GBP 265,836 for the period to 31 December 2024). The lower fees are attributable to the reduction in executive directors from two in the prior year period to one director in the reporting period.

A significant increase in the project portfolio focussed on acquiring production and near-term drilling activities, has been managed as a result of actions taken in 2024 to slim corporate technical personnel through Board re-structuring to improve efficiency and reduce out-sourcing costs.

· Legal and professional fees decreased to GBP 158,263 (GBP294,282 for the period to 31 December 2024).

This was achieved, despite greatly increased corporate activity, by making full use of the Company's inhouse legal and corporate experience.

· Executive directors' fees have decreased to GBP 120,572 (GBP 341,976 for the period to 31 December 2024).

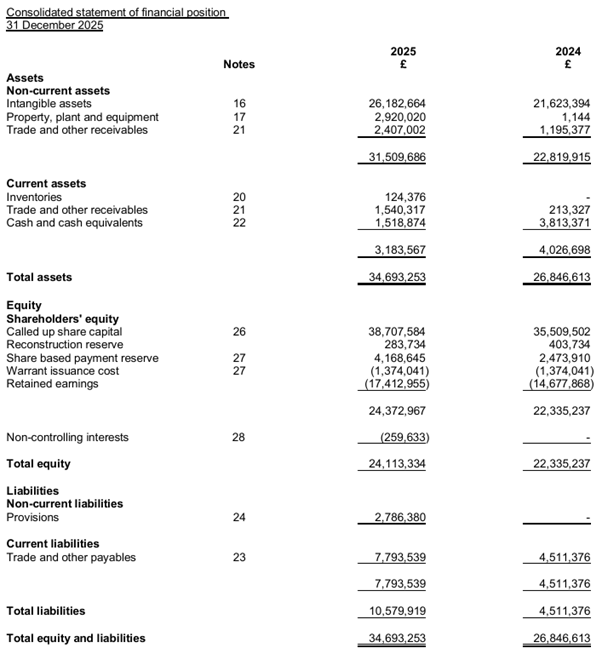

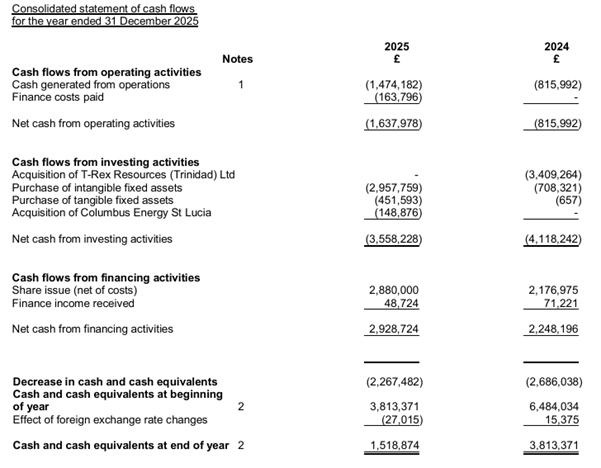

· Cash reserves at the end of the reporting period were GBP 1,518,874 (GBP 3,813,371 for the period to 31 December 2024).

Restricted cash of USD1,500,000 (USD1,500,000 for the period ended 31 December 2024) in the form of the security deposit for the Guercif Bank Guarantee was held in favour of ONHYM and USD419,000 was held in Trinidad companies available for Heritage licence performance bonds.

Post the reporting period the Company raised GBP 4.5 million (before expenses) in a placing of shares by AlbR Capital Limited and Oak Securities, acting jointly

· 1,020,000, 600,000, 690,000 and 549,885 Broker warrants exercisable at 10.5p, 15p, 9p and 8p respectively lapsed.

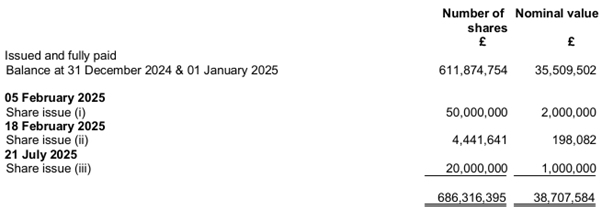

· 50,000,000 shares at a price of 4p per share were issued to Strategic Investors for a consideration of GBP 2,000,000. 10,000,000 warrants exercisable at 6p per share were issued.

· 20,000,000 shares at a price of 5p per share were placed for a consideration of GBP 1,000,000. 1,600,000 warrants exercisable at 5p per share were issued.

The net proceeds raised were to pay on 31 August 2025 deferred Consideration of USD500,000 for the acquisition of CEG assets in Trinidad and Tobago.

· 4,411,641 shares were issued to Challenger Energy ("CEG") to satisfy an initial cash-equivalent Consideration deposit of USD250,000 for the acquisition of all of CEG's business, producing assets and operations in Trinidad and Tobago.

· No broker warrants or share options were exercised.

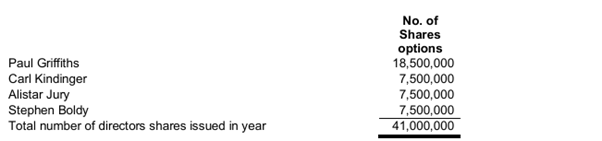

· 45,000,000 share options exercisable at 5.5p per share were issued to Company directors and a director of Tr-Rex Resources (Trinidad) Limited with vesting conditions and dates linked to activity milestones in Trinidad and Morocco being reached.

· The Company is adequately capitalised to progress planning and well inventory purchases for its proposed 2026 drilling operations in Trinidad and Morocco, free of debt and is in a position to deploy prudent levels of administrative expenditure focussed on enhancing and promoting the potential of the Company's portfolio.

· Following the admission of the Placing Shares and share Consideration for the acquisition of the CEG assets in Trinidad the issued share capital increased to 686,316,395 shares by the end of the period to 31 December 2025 (611,874,754 shares for the period ended 31 December 2024).

· 12.16% shareholder dilution in 2025 is measured against the Board's medium-term business growth strategy to:

- maintain sufficient working capital to grow the business through acquisitions and drilling to achieve materiality;

- to maintain 100% asset ownership at the pre-development stage to avoid partner pre-emption rights weakening the market for divestment opportunities;

- to retain operational control of timelines and strengthen negotiating leverage free of partner constraints;

- to retain 100% of operating profits without debt and interest payments and partner dilution;

- to maintain a minimum market capitalisation and share liquidity in difficult global public markets to facilitate acquisitions of producing assets.

Sentiment for investment and deal-making in the sector changed significantly during 2025 and the Company is well positioned for growth in 2026, having retained all critical personnel.

Highlights of key Operational Activities in 2025

Trinidad - Cory Moruga

· Access to reprocessed 3D seismic identified two primary targets for the Snowcap-3 ("SC-3") appraisal/development well based on two existing wells on the licence.

Herrera #8 Sand initial flow rate 1,450 bopd in Snowcap-1 discovery well (2010/11) and now newly correlated with Rochard-1 tested interval with an initial flow rate of 696 bopd.

Herrera #1 Sand initial flow rate 240 bopd in Rochard-1 discovery well (1955).

· 2025 focused on acquisition of assets with field operating staff, infrastructure, oil storage tanks and a sales point into Heritage Petroleum's oil pipeline network.

- necessary for targeting 2026 early production sales revenues from SC-3;

- sufficient oil storage capacity critical at production start-up;

- SC-3 to keep flowing, even if necessary at reduced rates, to prevent wax build-up (as has been the historical issue with intermittent production on the licence); and

- initial sales point capacity is required.

· SC-3 well design, replacing deviated well with a vertical well, rig discussions and drilling programme accelerated after completion of acquisition of strategic facilities.

· 2P/2C resources for the Snowcap Structure remain unchanged at 14.31 MM barrels oil.

Trinidad - Bonasse oil field

· Bonasse field brought back into wellhead production at a stabilised rate of 37 bopd by the end of 2025.

· 6 light well workovers, 2 heavy workovers and 2 new shallow infield development wells were completed.

· New potential shallow reservoir targets have been identified, as well as deeper targets, that will be evaluated for drilling in 2026.

Trinidad - Goudron. Inniss-Trinity and Icacos oil fields

· Production increased from 285 bopd on acquisition of the fields to 321 bopd on 31 December 2025.

· Focus on field infrastructure improvements and reduction of operating costs.

· GY-211 heavy well workover successfully completed, adding a stabilised rate of 22 bopd.

· Targets for new infield development wells identified in the Inniss-Trinity and Goudron fields.

Morocco - Guercif

Biogenic gas

· Rigless perforating of the "A" Sand in MOU-3 with, for the first time, larger perforating guns confirmed the extent of formation damage due to heavy mud weights used whilst drilling MOU-3, which shut off observed gas inflow.

· Results critical for Company's new drilling team to provide for:

- improved well planning to balance the optimum mud weight to maintain borehole stability without formation damage and preserve gas inflow from unconsolidated reservoirs; and

- the correct drilling mud chemistry to suppress reactive clays and clay swelling whilst drilling.

· Desktop studies prioritised the TGB-6 Submarine Fan Sand (incorporating the former terms "Ma Sand" and "TGB-6 Sand") for an initial pilot Compressed Natural Gas ("CNG") development.

· Net 2C resources of 61.95 BCF for that part of the TGB-6 Submarine Fan Sand penetrated within structural closure at MOU-3 (11 km²).

· Higher risk 81km² TGB-6 Submarine Fan Sand stratigraphic trap identified surrounding the MOU-3 structural closure.

· Results have been the catalyst to accelerate negotiations for a Gas Sales Agreement incorporating a third-party carry for a pre-development well (MOU-6) to -/- 950 metres to determine potential for a commercial gas flow rate.

MOU-5 drilling results

· MOU-5 was successfully drilled by the new drilling team to 1137 metres under-budget and using the new mud weight strategy developed by the Company. Excellent quality wireline logs, in contrast to MOU-3, were recorded.

- Unexpected occurrence of salt mobilised from a deeper source meant that the pre-drill Jurassic target did not come in as expected.

- Exploration focus has shifted to the Triassic gas potential below MOU-5 following the potential for a Triassic salt seal;

- A helium show and helium background spikes in sands at the base of the well

provided some support for the Company's helium generation model.

Highlights of ESG

· In 2025 the Company spent 4,127,683 Dirhams in Morocco on local services in relation to its 2025 rigless testing and MOU-5 drilling operations.

· Beneficiaries included civil engineering contractors; provision of Guercif warehouse staff (renting of warehouse in Guercif city); provision of water and waste disposal; fuel supplies; transport and drivers; and local hotel accommodation for rig and well services crews; This was a significant boost for the local economy around the city of Guercif.

· In Trinidad the Company has safe-guarded 45 jobs following the acquisition of the Goudron, Inniss-Trinity and Icacos oilfields.

· It sponsors a local soccer team.

· It remains committed to developing gas in Morocco as a contribution to reducing a reliance on power generation from coal, which generates higher C02 emissions.

· In Trinidad, the reservoirs in the mature oil fields acquired by the Company in 2025 still represent the only practical and economic option for C02 sequestration to reduce Trinidad's emissions to the atmosphere of CO2 from ammonia plants. The Company's Inniss-Trinity CO2 EOR project in 2020/21 demonstrated the potential. Trinidad's Green Levy Fund could be put to use to help fund practical CO2 sequestration.

Highlights of Directorate Changes

· There were no changes to the Board in 2025.

Post Period End:

7 January 2026

The Company announced daily oil production up at 367 bopd at 04/01/26 (308 bopd at 30/11/25).

B0N-17 development well in the Bonasse field and GY-211 heavy well workover in the Goudron field completed.

Transformer installed at the Goudron field.

20 January 2026

The Company announced that it had conditionally placed 128,571,419 million new ordinary shares at a placing price of 3.5 pence each to raise £4.5 million (before expenses). The placing was completed by AlbR Capital Limited and Oak Securities, acting jointly.

22 January 2026

The Company announced that drilling operations under the Master Services with NABI Construction commenced in the Bonasse field on 20 January 2026 with the first well in a multi-well programme, BON-18.

25 February 2026

The Company announced progress on a Pre-drill Independent Technical Report ("ITR") update for the proposed Snowcap-3 ("SC-3") appraisal well and transaction activity, together with an update on the Bonasse field drilling programme.

The key ITR conclusions are:

- SC-3 is targeting unrisked P50 Prospective Resources of 8.73 MM bbl of oil

- Net-back is USD32.6/bbl at WTI spot price of US$60/bbl

5 March 2026

The Company announced that further to the release of 25 February 2026 in respect of an operations update for Trinidad, the Company is publishing the Independent Technical Report ("ITR") by Scorpion Geoscience Ltd. for the proposed Snowcap-3 ("SC-3") appraisal well in the Cory Moruga Exploration and Production Licence.

5 March 2026

The Company announced gross sales revenues from production for the month of February from its four oil fields onshore Trinidad.

Field | Barrels sold | US$/barrel | Total US$ gross revenue |

Goudron | 4360 | 197,378 | |

Inniss-Trinity | 3912 | 95,377 | |

Icacos | 277 | 16,679 | |

Bonasse¹ | 459 | 27,637 | |

CUMULATIVE | 9,008 | 60.213 | 337,071 |

During February two new development wells, BON-18 and 19, have been drilled and completed in the Bonasse field and are online and producing.

Six offline wells in the Inniss-Trinity and Goudron fields have been brought back on production.

Paul Griffiths, Chief Executive Officer of Predator Oil & Gas Holdings Plc commented:

"2025 has been a transformational year for the Company with the addition of revenue-generating production through the acquisition of 3 oilfields in Trinidad. These have potential for improved operational efficiencies and enhanced oil production as we enter a cycle of rising commodity prices. The acquisitions have safe-guarded local jobs and services and have ensured that the management of the fields are to best practice environmental standards.

The facilities and infrastructure that have been acquired are vital for the accelerated development of the Snowcap oil accumulation. The SC-3 appraisal/development well is forecast to deliver a material uplift in the Company's production by the end of 2026, again capitalising on rising oil prices to support the investment in drilling. Executing SC-3 drilling operations are the absolute number one priority for the Company in 2026.

In Morocco we have taken a giant step to de-risk the operational drilling issues that prevented the Company from flowing gas from its 2021 to 2023 drilling programme. When the Company entered this undrilled area of the Guercif Basin there was no legacy well data or discoveries to formulate the most appropriate drilling programme for the undrilled and unknown geology. Consequently, Rharb Basin experience was used for pre-drill well planning which, following the drilling results and information gathering, proved to be inappropriate for this area. Concerted and aligned efforts by our technical management and new drilling team have supported the investment case to parties that have shown interest in buying the potential gas off-take. Every effort will be made during 2026 to build upon the successful 2025 work programme to deliver an application for an Exploitation Concession in 2026.

Despite the increase in drilling and testing operations and acquisition activity, the running costs and administrative expenses for the Company have been kept below the 2024 numbers. The Company is growing its business activities, remaining free of debt and burdensome interest payments, and maintaining 100% of its original project equities only because of a judicious level of shareholder dilution, including for its founder and Chief Executive Officer, through the placing from time to time of shares. From the very early beginnings of the Company, positions in Morocco and Trinidad were sought in assets that were identified by highly experienced management as having the necessary materiality and risk profile to potentially deliver value orders of magnitude above current market capitalisation. If this were simple then these assets would have been coveted by others, prepared to put as much work into them as the Company, and would never have become available to management.

Predator is now one of the few independent foreign oil producers onshore Trinidad. This is a proven oil- and gas-rich region recently brought to refreshed prominence by ExxonMobil's exploration success offshore Guyana. Predator is drilling one of the biggest onshore oil wells in Trinidad for several years. In Morocco we stand on the cusp of the first potential CNG development in the country. For that reason, delivering the risk-reward proposition will take as long as it takes in 2026 to underpin the likelihood of commercial success. We thank shareholders for their continued support and hope that they understand the balance between shareholder dilution and material gain that the Board is trying to progress in the way it believes is appropriate for the unusually volatile times we have all lived in over the past 6 years."

For further information visit www.predatoroilandgas.com

Follow the Company on X @PredatorOilGas.

This announcement contains inside information for the purposes of Article 7 of the Regulation (EU) No 596/2014 on market abuse.

Enquiries:

Predator Oil & Gas Holdings Plc Paul Griffiths Chief Executive Officer

| Tel: +44 (0) 1534 834 600 |

AlbR Capital Limited David Coffman / Jon Belliss

OAK Securities Jerry Keen / Calvin Mann

|

Tel: +44 (0)207 469 0930

Tel: +44 (0) 20 3973 3678

|

Flagstaff Strategic and Investor Communications Tim Thompson Alison Alfrey Fergus Mellon

| Tel: +44 (0)207 129 1474 |

Notes to Editors:

Predator is an oil & gas company with a portfolio of assets including unique and highly prospective onshore Moroccan gas exposure and production, appraisal and exploration projects onshore Trinidad.

Morocco offers a potentially faster route to commercialisation of shallow biogenic gas through a CNG or micro-LNG development. The structure penetrated by the MOU-1 and MOU-3 wells is currently defined as having the best potential for an application for an Exploitation Concession in 2026. The Company is committed to partnering with entities capable of supporting a future development decision and who have already identified the opportunity as one warranting the execution of a Collaboration Agreement and a Memorandum of Understanding. Moroccan gas prices are high, and the fiscal terms are some of the best in the world. The presence of gas export infrastructure adjacent to the MOU-1 and MOU-3 structure allows for a scalable gas development after initial CNG or micro-LNG gas production over time establishes the extent of connected gas volumes and the capability of reservoirs to deliver at plateau rates over time.

Trinidad offers the security of a mature onshore oil province that has been producing hydrocarbons for over 50 years. Predator has assembled a portfolio of onshore producing fields with opportunities for production enhancement and additional infill development and appraisal drilling. Significant legacy tax losses, economies of scale and the application of new low-cost technologies are factors that can improve profit margins per barrel of oil produced. A Master Services Agreement with local operator NABI Construction relieves the Company of the burden and costs of operating the fields and executing drilling and heavy well workovers. In return the Company receives 30% of gross sales revenues for which it can use its acquired tax losses to substantially reduce Petroleum Profit Tax from 50% to an effective rate of 12.5%.

Predator has an experienced technical, financial and legal management team with particular knowledge of the Moroccan and Trinidad sub-surface and operations and an ability to complete M & A transactions in Trinidad and receive regulatory approvals in a timely manner and without any unnecessary advisory fees for transactions. The Company's strategy is to operate at a much reduced overhead compared to other operators with portfolios of assets of similar extent to maintain competitiveness.

Predator Oil & Gas Holdings plc is listed on the Equity Shares (transition) category of the Official List of the London Stock Exchange's main market for listed securities (symbol: PRD).

For further information, visit www.predatoroilandgas.com

The accompanying accounting policies and notes on the following pages form an integral part of these financial statements.

All items in the above statement derive from continuing operations.

The accompanying accounting policies and notes on the following pages form an integral part of these financial statements.

The financial statements were approved by the Board of Directors and authorised for issue on ............................................. and were signed by:

.......................................................................

Paul Griffiths - Director

The accompanying accounting policies and notes on the following pages form an integral part of these financial statements.

The accompanying accounting policies and notes on the following pages form an integral part of these financial statements.

Statement of accounting policies

For the year ended 31 December 2025

1. General information

Predator Oil & Gas Holdings Plc ("the Company") and its subsidiaries (together "the Group") are engaged principally in the operation of an oil and gas development business in the Republic of Trinidad and Tobago and an exploration and appraisal portfolio in Ireland and Morocco. The Company's ordinary shares are on the Official List of the UK Listing Authority in the premium listing section of the London Stock Exchange.

Predator Oil & Gas Holdings plc was incorporated in 2017 as a public limited company under Companies (Jersey) Law 1991 with registered number 125419. It is domiciled and registered at 3rd Floor, One The Esplanade, St Helier, Jersey, JE2 3QA.

2. Statutory information

Predator Oil & Gas Holdings PLC is a private company, registered in Jersey. The Company's registered number and registered office address can be found on the General Information page.

3. Accounting policies

Basis of preparation

The principal accounting policies adopted in the preparation of the financial information are set out below. The policies have been consistently applied throughout the current year and prior year, unless otherwise stated. These financial statements have been prepared in accordance with International Financial Reporting Standards (IFRSs and IFRIC interpretations) as adopted by the European Union and with those parts of the Companies (Jersey) Law, 1991 applicable to companies preparing their accounts under IFRS. The Company has adopted the exemption under Companies (Jersey) Law 1991 Article 105 (11) not to prepare separate accounts.

The consolidated financial statements incorporate the results of Predator Oil & Gas Holdings Plc and its subsidiary undertakings as at 31 December 2025.

The financial statements are prepared under the historical cost convention on a going concern basis. The financial statements of the subsidiaries are prepared for the same reporting period as the parent company, using consistent accounting policies. All intra-group balances, transactions, income and expenses and profits and losses resulting from intra-group transactions that are recognised in assets, are eliminated in full. Subsidiaries are fully consolidated from the date of acquisition, being the date on which the Group obtains control, and continue to be consolidated until the date that such control ceases.

Change in Accounting Standards

At the date of approval of these financial statements, certain new standards, amendments and interpretations have been published by the International Accounting Standards Board but are not as yet effective and have not been adopted early by the Group. All relevant standards, amendments and interpretations will be adopted in the Group's accounting policies in the first period beginning on or after the effective date of the relevant pronouncement.

At the date of authorisation of these financial statements, a number of Standards and Interpretations were in issue but were not yet effective. The Directors do not anticipate that the adoption of these standards and interpretations, or any of the amendments made to existing standards as a result of the annual improvements cycle, will have a material effect on the financial statements in the year of initial application.

Standards and amendments to existing standards effective 1 January 2025

- Amendment to IAS 1 - Classifications of Liabilities as Current or Non-current

- Amendment to IFRS 16 - Lease Liability in a Sale and Leaseback

- Amendment to IAS 1 - Non-current Liabilities with Covenants

- Amendments to IAS 7 and IFRS 7 - Supplier Finance Arrangements

- Amendments to IAS 12 - International Tax Reform - Pillar Two Module Rules

New Standards, amendments and interpretations effective after 1 January 2026 and have not been early adopted

The Group does not believe that the standards not yet effective, will have a material impact on the consolidated financial statements.

Areas of estimates and judgement

The preparation of the group financial statements in conformity with generally accepted accounting principles requires the use of estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Although these estimates are based on management's best knowledge of current events and actions, actual results may ultimately differ from those estimates.

Provisions

Provisions are recognised when the Group has a present obligation (legal or constructive) as a result of a past event and it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation and a reliable estimate can be made of the amount of the obligation. Where the Group expects some or all of a provision to be reimbursed, the reimbursement is recognised as a separate asset but only when the reimbursement is virtually certain. The expense relating to any provision is presented in the statement of comprehensive income net of any reimbursement. If the effect of the time value of money is material, provisions are discounted using a current pre-tax rate that reflects, where appropriate, the risks specific to the liability. Where discounting is used, the increase in the provision due to the passage of time is recognised as a borrowing cost.

Going concern

The Group's cash flow projections indicate that the Group should have sufficient resources to continue as a going concern. As at 31 December 2025 the Group had cash of £1.52m and no debt. Licence commitments for funding in 2026 have been satisfied by a placing completed in January 2026 and the terms of the NABI MSA. As a result, the Group's overheads will not require funding for a minimum of 12 months from the date of this review taking into account the forecast production revenues from Trinidad. In addition, the Group is fully funded for all firm operational commitments for 2026 up to and including April 2027.

The Group is generating production revenues from operations from Trinidad following the 2025 acquisition of the CEG Business and these are expected to increase during 2026.

The Group's subsidiaries are funded by inter-company loans advanced by Predator Oil & Gas Holdings plc (the Company'). The recoverability of the inter-company loans advanced depends also on the subsidiaries realising their cash flow projections will depend on raising equity, debt finance, licence and/or joint venture partnerships, and potential partial or complete divestment of its assets in Morocco, if an attractive opportunity to monetise is presented to finance the Group's projects to maturity and revenue generation.

The Board have reviewed a range of potential cash flow forecasts for the period to 30 April 2027, including reasonable possible downside scenarios. Going forward the Group has a number of different options, independent of also being able to reduce corporate costs, raise equity funds (as it has shown to be consistently capable of doing since listing as a public company in 2018), and accessing reserves-based lending, to potentially increase its working capital if required as follows:

The existing Trinidad licences are expected to become self-funding when production commences in the course of 2026. Pursuant to a placing in January 2026, a total capital of £4.5m before expenses was raised. In 2026 a quantum of these funds will be applied to drilling and testing Snowcap-3 ("SC-3") appraisal and development well. The well is scheduled for Q2 2026 and is expected to take up to 20 days to drill and log to a depth of approximately 5300 feet. It is intended to put the well in production in Q3 2026 after drilling and testing completes.

SC-3 will potentially unlock the 3P resources for the Herra #1, #2 #3 and #4 Sands of 56.9MM barrels of oil. The cash flow forecasts for Trinidad production are robust and use available tax losses to increase the net-back per barrel of oil. Cash flows are sufficient to cover any Working Capital Forecast shortfall during 2026. Costs in maintaining the operations in the existing fields ('workovers') will be funded from existing cash flows.

The Group will progress joint venture partnering for the Guercif gas asset to agree principles for funding the drilling and testing of the MOU-6 well and a Phase 1 gas development contingent on the application in 2026 for an Exploitation Concession.

Any intention to pursue various incremental activities in Trinidad and Morocco are likely to be funded through a farm down of some project equity interest or fresh equity raises if need be. Significant cost savings are forecast for the Group by apportioning operating costs and administrative costs over a larger portfolio of producing assets.

In Ireland, if awarded, the Corrib South licence will not require funding in 2026 due to a provisional commitment reached with a farm-in partner. Progressing these discretionary activities will be dependent on a combination of potentially further equity and/or funds raised from farm out and in the case of Trinidad will be supported by the proceeds of oil production following the aforesaid workovers. Directors are confident that the Group will be able to meet requirements over the course of the foreseeable future.

1. Trinidad - Cory Moruga licence

For Predator Oil & Gas Trinidad Ltd., where production revenues from its wholly Trinidad owned subsidiary, T-Rex Resources (Trinidad) Limited (TRex') are forecast to be generated in 2026 following the drilling of the Snowcap-3 appraisal/development well. The well will be funded out of existing cash resources from the January 2026 placing. The Cory Moruga Production Licence provides the Group with the potential to generate strongly positive cashflows so as possibly to contribute organically towards further development of the Group's assets. Capital required for a staged field development in 2026 could be funded from operating profits generated from an increasing level of accrued gross production net profits following the Snowcap-3 well. The Group may resort to the option of raising equity funding to accelerate this development if this proves to be commercially advantageous. The Group also has the option to seek a partial or complete divestment of any of its rehabilitated producing assets to indigenous local companies, where the Group's ability to offer CO2 EOR services and expertise, accrued tax losses and the application of a patented chemical wax treatment new to Trinidad potentially enhances the value of the Group's assets.

The Initial Work Programme agreed by TRex with the MEEI will be conducted in 2026 with the completion of the drilling of Snowcap-3.

2. Morocco - Guercif licence

In the case of Predator Gas Ventures Ltd., recovery of inter-company loans is dependent upon the Guercif drilling and rigless testing programmes successfully recovering commercial quantities of gas that can be developed and brought to market. Following significant gas discoveries in 2021 and 2023 a programme of rigless testing was undertaken in 2024 and 2025. Information gained from these work programmes has enabled the Group to enter into substantive discussions for third-party funding for the drilling of an appraisal/development well (MOU-6) as a prelude to an application for an Exploitation Concession and a fully-funded pilot CNG development.

If an application for an Exploitation Concession is submitted in Q4 2026, the Group has until Q1 2027 to elect whether or not to carry out further exploration on the Guercif Licence in the area outside the limits of any Exploitation Concession. Electing whether or not to enter the Second Extension Period of the Guercif Petroleum Agreement, which involves committing to 3D seismic and the drilling of one well, will depend upon a final review of exploration prospects and the potential availability of funds arising from any repayment of past costs related to the ongoing joint venture partnering negotiations/

If electing not to go forward into the First Extension Period the Group will have satisfied all its exploration licence commitments and will be entitled to the return of its USD1.5m bank guarantee.

3. Ireland

In the case of Predator Oil and Gas Ventures Ltd., the quantum of inter-company loan is relatively small and no material expenditures are anticipated going forward in 2026. The Group is awaiting the outcome of an application for a successor authorisation to Licensing Option 16/26 (Corrib South) which is under active consideration as confirmed by the Department of the Environment, Climate and Communications ("DECC"). Acceptance of any licence award would be at the Group's sole discretion. There are not likely to be any significant funding implications emerging from this process in 2026. In the future, the potential exists for the Company, as promoters of an LNG project to receive introduction and service providers' fees and a free minority equity position in a joint venture vehicle to move to the project development stage. Under these circumstances the inter-company loan would constitute past costs contributing to the level of free equity. Recovery of the relatively modest inter-company loan therefore has a variety of ways of being repaid. A potential award of the Corrib South successor licence and a closing of a farm down to one of the Corrib gas field owners would potentially grant the Group access rights to the Corrib infrastructure with which to re-purpose the Mag Mell FSRU project to deliver LNG to the Corrib pipeline and for potential gas storage at Corrib South. The change in the Irish Government coalition and the deteriorating situation with relation to gas supplies and gas storage in Europe provides an incentive for a new government policy in relation to security of energy and gas supply. The proposed non-commercial Gas Networks Ireland Strategic Gas Reserve, based on a FSRU moored in the Shannon Estuary, does not address the current demands for gas for peak-time electricity generation, when renewables are weather dependent, and for subsurface gas storage as in other European countries.

Share based payments

The Group has applied the requirements of IFRS 2 Share-based Payment for all grants of equity instruments. The Group operates an equity settled share option scheme for directors. The increase in equity is measured by reference to the fair value of equity instruments at the date of grant. The liabilities incurred under these arrangements are assumed to be converted into shares in the parent company, under an option arrangement. The fair value of the service received in exchange for the grant of options and warrants is recognised as an expense. Equity-settled share-based payments are measured at fair value (excluding the effect of non-market based vesting conditions) at the date of grant. The fair value determined at the grant date of equity-settled share-based payment is expensed over the vesting period, based on the Group's estimate of shares that will eventually vest and adjusted for the effect of non-market based vesting conditions.

During the year, the Company issued warrants in lieu of fees to stockbrokers and as part of a placing ordinary shares. The warrant agreements do not contain vesting conditions and therefore the full share-based payment charge, being the fair value of the warrants using the Black-Scholes model, has been recorded immediately. The charge is recognised within the statement of changes in equity. The valuation of these warrants involves making a number of estimates relating to price volatility, future dividend yields and continuous growth rates (see Note 29).

The fair value of the share options is estimated by using the Black Scholes model on the date of grant based on certain assumptions. Those assumptions are described in note 30 and include, among others, the expected volatility and expected life of the options. The expected life used in the model has been adjusted, based on management's best estimate, for the effects of non-transferability exercise restrictions and behavioural considerations. The market price used in the model is the market price at the date of the issue of the options. Where the terms and conditions of options are modified before they vest, the increase in the fair value of the options, measured immediately before and after the modification, is also charged to profit or loss over the remaining vesting period.

Where equity instruments are granted to persons or entities other than staff, the fair value of goods and services received is charged to profit or loss, except where it is in respect to costs associated with the issue of shares, in which case, it is charged to the share premium account.

The fair values calculated are inherently subjective and uncertain due to the assumptions made and the limitation of the calculations used. Further details of the specific amounts concerned are given in note 29.

Business combinations

Business combinations are accounted for using the acquisition method. The cost of an acquisition is measured as the fair value of the assets given, equity instruments issued, and liabilities incurred or assumed at the acquisition date.

Identifiable assets acquired and liabilities assumed are measured and recognized at their fair value at the date of the acquisition, with the exception of income taxes, and lease liabilities. Any deferred tax asset or liability arising from a business combination is recognized at the acquisition date. Transaction costs associated with a business combination are expensed as incurred. Results of acquisitions are included in the financial statements from the closing date of the acquisition. If the consideration of the acquisition is less than the fair value of the net assets received, the difference is recognized immediately in the statements of comprehensive income. If the consideration of the acquisition is greater than the fair value of the net assets received, the difference is recognised as goodwill on the consolidated balance sheet.

The directors have included provisional fair values within the business combination note as presented above, which represent their best estimates using information available at the year end. Under IFRS 3, there is a measurement period which shall not exceed one year from the acquisition date, during which the company can, if necessary, retrospectively adjust the provisional amounts recognised at the acquisition date to reflect new information obtained about facts and circumstances that existed as of the acquisition date.

Basis of consolidation

Where the Group has control over an investee, it is classified as a subsidiary. The Group controls an investee if all three of the following elements are present: power over the investee, exposure to variable returns from the investee, and the ability of the investor to use its power to affect those variable returns. Control is reassessed whenever facts and circumstances indicate that there may be a change in any of these elements of control.

The consolidated financial statements present the results of the Company and its subsidiaries ("the Group") as if they formed a single entity. Inter-company transactions and balances between Group companies are therefore eliminated in full. Uniform accounting policies are applied across the Group.

The consolidated financial statements incorporate the results of business combinations using the acquisition method. In the statement of financial position, the acquirer's identifiable assets, liabilities and contingent liabilities are initially recognised at their fair values at the acquisition date. The results of acquired operations are included in the consolidated statement of comprehensive income from the date on which control is obtained. They are deconsolidated from the date on which control ceases.

Intangible assets - exploration and evaluation assets

Exploration and evaluation expenditure incurred which relates to more than one area of interest is allocated across the various areas of interest to which it relates on a proportionate basis. Exploration and evaluation expenditure incurred by or on behalf of the Group is accumulated separately for each area of interest. The area of interest adopted by the Group is defined as a petroleum title.

Expenditure in the area of interest comprises direct costs and an appropriate portion of related overhead expenditure but does not include general overheads or administrative expenditure not linked to a particular area of interest. Direct costs incurred in the exploration and evaluation of potential resources include exploration licences, researching and analysing historical exploration data, exploratory drilling, trenching, sampling and the costs of pre-feasibility studies.

As permitted under IFRS 6, exploration and evaluation expenditure for each area of interest, other than that acquired from the purchase of another entity, is carried forward as an asset at cost provided that one of the following conditions is met:

· the costs are expected to be recouped through successful development and exploitation of the area of interest, or alternatively by its sale; or

· exploration and/or evaluation activities in the area of interest have not, at the reporting date, reached a stage which permits a reasonable assessment of the existence or otherwise of economically recoverable reserves, and active and significant operations in, or in relation to, the area of interest are continuing.

Such costs are initially capitalised as intangible assets and include payments to acquire the legal right to explore, together with the directly related costs of technical services and studies, seismic acquisition, exploratory drilling and testing. Exploration and evaluation expenditure which fails to meet at least one of the conditions outlined above is taken to the consolidated statement of comprehensive income.

Expenditure is not capitalised in respect of any area of interest unless the Group's right of tenure to that area of interest is current.

Intangible exploration and evaluation assets in relation to each area of interest are not amortised until the existence (or otherwise) of commercial reserves in the area of interest has been determined.

Exploration and evaluation assets are assessed for impairment when facts and circumstances suggest that the carrying amount may exceed its recoverable amount. In accordance with IFRS 6, the Group reviews and tests for impairment on an ongoing basis and specifically if the following occurs:

a) the period for which the Group has a right to explore in the specific area has expired during the period or will expire in the near future, and is not expected to be renewed;

b) substantive expenditure on further exploration for and evaluation of hydrocarbon resources in the specific area is neither budgeted nor planned;

c) exploration for and evaluation of hydrocarbon resources in the specific area have not led to the discovery of commercially viable quantities of mineral resources and the Group has decided to discontinue such activities in the specific area; or

d) sufficient data exists to indicate that although a development in the specific area is likely to proceed the carrying amount of the exploration and evaluation asset is unlikely to be recovered in full from successful development or by sale.

An impairment loss is recognised for the amount by which the asset's carrying value exceeds its recoverable amount. The recoverable amount is the higher of an asset's fair value less costs to sell and value in use. For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash inflows which are largely independent of the cash inflows from other assets or groups of assets (cash-generating units).

Net proceeds from any disposal of an exploration asset are initially credited against the previously capitalised costs. Any surplus proceeds are credited to the consolidated statement of comprehensive income.

Oil and gas development/producing assets and commercial reserves

If the field is determined to be commercially viable, the attributable costs are transferred to development/production assets within tangible assets in single field cost centres. Subsequent expenditure is capitalised only where it either enhances the economic benefits of the development/producing asset or replaces part of the existing development/producing asset. Decreases in the carrying amount are charged to the consolidated statement of comprehensive income.

Net proceeds from any disposal of development/producing assets are credited against the previously capitalised cost. A gain or loss on disposal of a development/producing asset is recognised in the consolidated statement of comprehensive income to the extent that the net proceeds exceed or are less than the appropriate portion of the net capitalised costs of the asset.

Commercial reserves are proven and probable oil and gas reserves, which are defined as the estimated quantities of crude oil, natural gas and natural gas liquids which geological, geophysical and engineering data demonstrate with a specified degree of certainty to be recoverable in future years from known reservoirs and which are considered commercially producible. There should be at least a 50% statistical probability that the actual quantity of recoverable reserves will be more than the amount estimated as a proven and probable reserves.

Depletion and amortisation

All expenditure carried within each field is amortised from the commencement of production on a unit of production basis, which is the ratio of oil and gas production in the period to the estimated quantities of commercial reserves at the end of the period plus the production in the period, generally on a field-by-field basis. In certain circumstances, fields within a single development area may be combined for depletion purposes. Costs used in the unit of production calculation comprise the net book value of capitalised costs plus the estimated future field development costs necessary to bring the reserves into production. Changes in the estimates of commercial reserves or future field development costs are dealt with prospectively.

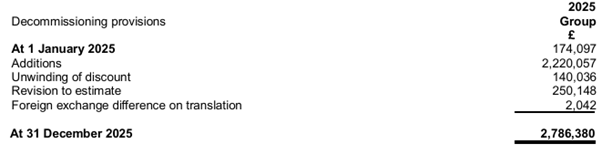

Decommissioning

Where a material liability for the removal of production facilities and site restoration at the end of the productive life of a field exists, a provision for decommissioning is recognised. The amount recognised is the present value of estimated future expenditure determined in accordance with local conditions and requirements. The cost of the relevant tangible fixed asset is increased with an amount equivalent to the provision and depreciated on a unit of production basis. Changes in estimates are recognised prospectively, with corresponding adjustments to the provision and the associated fixed asset.

Property, Plant and equipment

Property, plant and equipment is stated in the consolidated statement of financial position at cost less accumulated depreciation and any recognised impairment loss. Depreciation on property, plant and equipment other than exploration and production assets, is provided at rates calculated to write off the cost less estimated residual value of each asset on a straight-line basis over its expected useful economic life.

Depreciation rates applied for each class of assets are detailed as follows:

Furniture, fittings and equipment: 1 - 5 years

Motor vehicles: 5 years

Leasehold improvements: Over the life of the lease

The assets' residual values and useful lives are reviewed, and adjusted if appropriate, at each balance sheet date.

An asset's carrying amount is written down immediately to its recoverable amount if the asset's carrying amount is greater than its estimated recoverable amount with any impairment charge being taken to the consolidated statement of comprehensive income.

Gains and losses on disposals are determined by comparing proceeds with carrying amount and are recognised in the consolidated statement of comprehensive income.

Financial assets

The Financial assets currently held by the Group are classified as loans and receivables and cash and cash equivalents. These assets are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They are initially recognised at fair value plus transaction costs that are directly attributable to their acquisition or issue and are subsequently carried at amortised cost using the effective interest rate method less provision for impairment.

Impairment provisions are recognised when there is objective evidence (such as significant financial difficulties on the part of the counterparty or default or significant delay in payment) that the Group will be unable to collect all of the amounts due under the terms receivable, the amount of such a provision being the difference between the net carrying amount and the present value of the future expected cash flows associated with the impaired receivable. For receivables, which are reported net, such provisions are recorded in a separate allowance account with the loss being recognised within administrative expenses in the statement of comprehensive income. On confirmation that the receivable will not be collectable, the gross carrying value of the asset is written off against the associated provision.

Cash and cash equivalents

These amounts comprise cash on hand and balances with banks. Cash equivalents are short term, highly liquid accounts that are readily converted to known amounts of cash. They include short-term bank deposits and short-term investments.

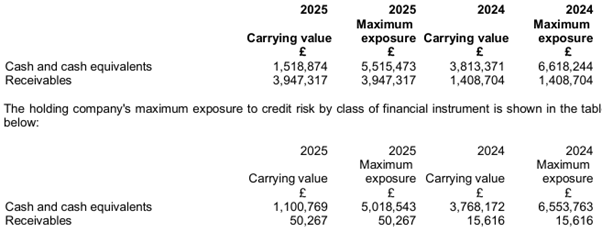

Any cash or bank balances that are subject to any restrictive conditions, such as cash held in escrow pending the conclusion of conditions precedent to completion of a contract, are disclosed separately as "Restricted cash". The security deposit is recognised within trade and other receivables in note 21.

There is no significant difference between the carrying value and fair value of receivables.

Derecognition

The Group derecognises a financial asset when the contractual rights to the cash flow from the asset expire, or it transfers the asset and substantially all the risk and rewards of ownership of the asset to another entity.

Financial liabilities

The Group's financial liabilities consist of trade and other payables (including short terms loans) and long term secured borrowings. These are initially recognised at fair value and subsequently carried at amortised cost, using the effective interest method. All interest and other borrowing costs incurred in connection with the above are expensed as incurred and reported as part of financing costs in profit or loss. Where any liability carries a right to convertibility into shares in the Group, the fair value of the equity and liability portions of the liability is determined at the date that the convertible instrument is issued, by use of appropriate discount factors.

Derecognition

The Group derecognises a financial liability when the obligations are discharged, cancelled or they expire.

Foreign currency

The functional currency of the Group is the British Pound Sterling. Subsidiaries in the Group have the following functional currencies: United States Dollars, British Pound Sterling, and Trinidad & Tobago Dollars. Transactions in foreign currencies are translated at the exchange rate ruling at the date of each transaction. Foreign currency monetary assets and liabilities are retranslated using the exchange rates at the balance sheet date. Gains and losses arising from changes in exchange rates after the date of the transaction are recognised in the consolidated statement of comprehensive income. This treatment of monetary items extends to the Group's intercompany loans whereby gains and losses arising from changes in the exchange rate after the date of transaction are also recognised in the consolidated statement of comprehensive income. Intercompany loans are provided to subsidiaries in the Group with the expectation that these loans will be collected in the foreseeable future. Non-monetary assets and liabilities that are measured in terms of historical cost in a foreign currency are translated at the exchange rate at the date of the original transaction.

In the financial statements, the net assets of the Group are translated into its presentation currency at the rate of exchange at the balance sheet date. Income and expense items are translated at the average rates for the period. The resulting exchange differences are recognised in equity and included in the translation reserve.

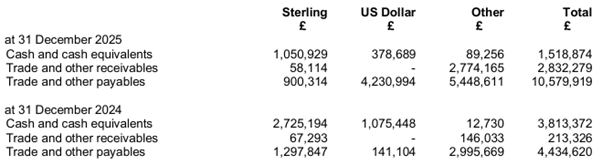

The exchange rates applied at each reporting date were as follows:

31 December 2025 - £1: £1 : US$ 1.345 , £1 : Euro 1.145 , £1 : MAD12.266 and £1: TT$ 9.122

31 December 2024 - £1: £1 : US$1.2548, £1 : Euro1.12059 , £1 : MAD12.6916 and £1: TT$ 8.53

Share options and Equity Instruments

Where the terms and conditions of options are modified before they vest, the increase in the fair value of the options, measured immediately before and after the modification, is also charged to profit or loss over the remaining vesting period. Where equity instruments are granted to persons other than consultants, the fair value of goods and services received is charged to profit or loss, except where it is in respect to costs associated with the issue of shares, in which case, it is charged to the share capital or share premium account.

Equity instruments

Share capital represents the amount subscribed for shares at each of the placings. The reconstruction reserve account represents premiums received on the share capital of subsidiaries and also includes directly related share issue costs.

Warrants issuance cost reserve includes any costs relating to warrants issued for services rendered accounted for in accordance with IFRS 2 - Equity-settled instruments.

The share-based payments reserve represents equity-settled shared-based employee remuneration for the fair value of the options issued.

Retained earnings include all current and prior period results as disclosed in the Statement of comprehensive income, less dividends paid to the owners of the Company.

Inventories

Inventories are stated at the lower of cost and net realisable value. Cost is determined by the weighted average cost formula, where cost is determined from the weighted average of the cost at the beginning of the period and the cost of purchases during the period. Net realisable value represents the estimated selling price less all estimated costs of completion and costs to be incurred in marketing, selling and distribution.

Revenue recognition

Crude oil sales are recognised when control of the crude oil has transferred, being when the crude is delivered to the customer by means of a custody transfer ticket document, the customer has full discretion over the channel and price to sell the crude oil, and there is no unfulfilled obligation that could affect the customer's acceptance of the crude oil. Revenue is recognised as this is the point in time that the consideration is unconditional because only the passage of time is required before the payment is due.

No element of financing is deemed present as typically, payment for the sale of the oil is received by the end of the month following the month in which the sale is recognised, which is consistent with market practice.

Taxation

The Company and all subsidiaries ('the Group') are registered in Jersey, Channel Islands and are taxed at the Jersey company standard rate of 0%. However, the Group's projects are situated in jurisdictions where taxation may become applicable to local operations.

The major components of income tax on the profit or loss include current and deferred tax.

Current tax

Current tax is based on the profit or loss adjusted for items that are non-assessable or disallowed and is calculated using tax rates that have been enacted or substantively enacted by the reporting date.

Tax is charged or credited to the statement of comprehensive income, except when the tax relates to items credited or charged directly to equity, in which case the tax is also dealt with in equity.

Deferred tax

Deferred tax assets and liabilities are recognised where the carrying amount of an asset or liability in the statement of financial position differs to its tax base, except for differences arising on:

· The initial recognition of an asset or liability in a transaction which is not a business combination and at the time of the transaction affects neither accounting or taxable profit; and

· Investments in subsidiaries and jointly controlled entities where the Group is able to control the timing of the reversal of the difference and it is probable that the differences will not reverse in the foreseeable future. Recognition of deferred tax assets is restricted to those instances where it is probable that taxable profit will be available against which the difference can be utilised.

The amount of the asset or liability is determined using tax rates that have been enacted or substantively enacted by the reporting date and are expected to apply when deferred tax liabilities/ (assets) are settled/ (recovered). Deferred tax balances are not discounted.

Cash and cash equivalents

Cash and cash equivalents include cash on hand and deposits held at call with financial institutions with original maturities of three months or less. For the purposes of the statement of cash flows, restricted cash is not included within cash and cash equivalents (refer to note 21 for details of restricted cash).

Share capital

Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of new shares or options are deducted, net of tax, from the share premium. Net proceeds are disclosed in the statement of changes in equity.

Costs of share issues are written off against the premium arising on the issues of share capital.

Finance costs

Borrowing costs are recognised as an expense when incurred.

Borrowings

Borrowings are initially recognised at fair value, net of any applicable transaction costs incurred. Borrowings are subsequently carried at amortised cost; any difference between the proceeds (net of transaction costs) and the redemption value is recognised in the income statement over the period of the borrowings using the effective interest method (if applicable).

Interest on borrowings is accrued as applicable to that class of borrowing.

Notes to the financial statements

For the year ended 31 December 2025

4. Revenue

The Group's revenue was derived from crude oil to the state oil company in the Trinidad and Tobago, Heritage Petroleum Company Limited and amounted to £938,835 (2024: £Nil). All sales are made from the Group's own production. The Group does not engage in oil trading, nor does not buy or sell oil forwards, derivatives, or any other form of non-physical contract.

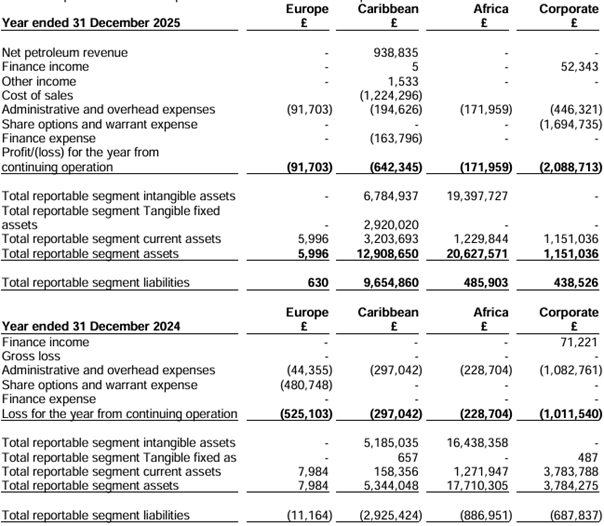

5. Segmental reporting

The Group operates in one business segment, the exploration, appraisal and development of oil and gas assets. The Group has interests in three geographical segments being Africa (Morocco), Europe (Ireland) and the Caribbean (Trinidad and Tobago).

The Group's operations are reviewed by the Board (which is considered to be the Chief Operating Decision Maker ('CODM')) and split between oil and gas exploration and development and administration and corporate costs. Exploration and development are reported to the CODM only on the basis of those costs incurred directly on projects. Administration and corporate costs are further reviewed on the basis of spend across the Group.

Decisions are made about where to allocate cash resources based on the status of each project and according to the Group's strategy to develop the projects. Each project, if taken into commercial development, has the potential to be a separate operating segment. Operating segments are disclosed below on the basis of the split between exploration and development and administration and corporate.

6. Cost of sales

7. Auditors remuneration

8. Finance income

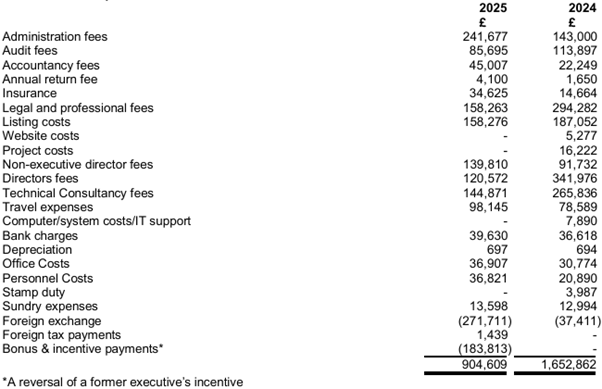

9. Administration expenses

10. Performance and compensation bonus

11. Finance expense

12. Income Tax

No charge to taxation arises due to the losses incurred in all jurisdictions and or in the case of Jersey a 0% rate of tax applies.

Predator Gas Ventures Limited is subject to tax in its operating jurisdiction of Morocco; however, the Company is loss making and has no taxable profits to date. There is a 10 year corporation tax holiday in Morocco commencing on the date of award of an Exploitation Concession.

TRex is subject to tax in its operating jurisdiction of Trinidad and Tobago during the year the Company incurred costs of £778,730 (TTD 7,103,635) which are available to be carried forward against future taxable profits.

No deferred tax asset has been recognised on accumulated tax losses because of uncertainty over the timing of future taxable profits against which the losses may be offset.

No deferred tax asset or liability has been recognised as the Standard Jersey corporate tax rate is 0%.

Tax losses of GBP36.2m for the Group's Trinidad and Tobago companies include losses confirmed (GBP36.0m) with the BIR up to and including 2024 and also estimates of (GBP.2m) for 2025 based on computations.

13. Director's fees and share based compensation

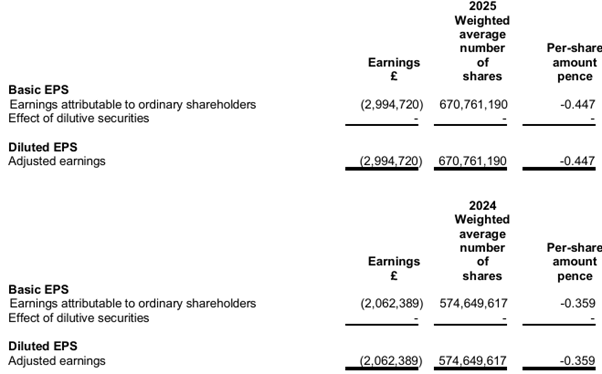

14. Earnings per share

Basic earnings per share is calculated by dividing the earnings attributable to ordinary shareholders by the weighted average number of ordinary shares outstanding during the period.

Diluted earnings per share is calculated using the weighted average number of shares adjusted to assume the conversion of all dilutive potential ordinary shares.

The effect of potential dilutive ordinary shares has not been shown, as the Group incurred a loss for the year and the inclusion of such shares would be anti dilutive. Accordingly, diluted earnings per share has not been disclosed.

Reconciliations are set out below.

15. Loss for the financial year

The Group has adopted the exemption in terms of Companies (Jersey) law 1991 and has not presented its own separate individual income statement in these financial statements for the Parent Company.

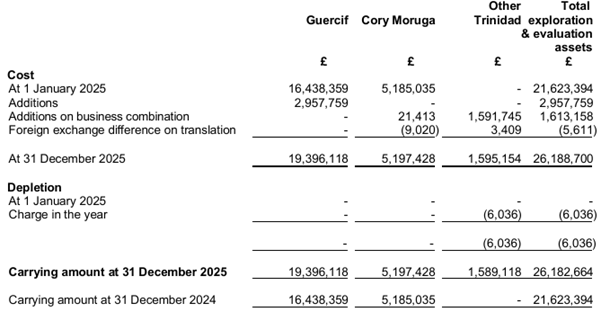

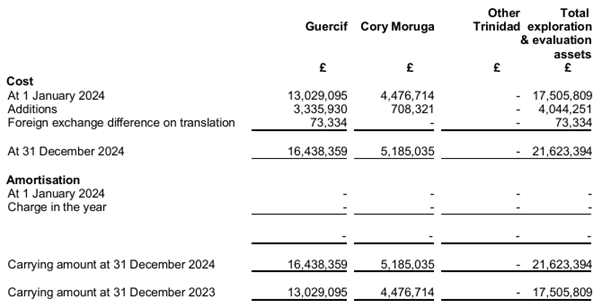

16. Intangible assets

Project Guercif

The total carrying amount of Project Guercif at 31 December 2025 of £19,397,727 (2024: £16,438,359) relates to costs incurred with wells MOU-1, MOU-2, MOU-3, MOU-4, MOU-5 and MOU-6.

Impairment Review Guercif

Predator Oil & Gas Plc ("The Company") accounts for its exploration and evaluation assets based on IFRS 6 (Exploration for and Evaluation of Mineral Resources). The Company's policy is to follow the successful efforts method. Exploration and appraisal activities are initially capitalised as intangible assets, pending determination of the existence of commercial reserves in the licence area. Such costs are classified as intangible assets based on the nature of the underlying asset, which does not yet have any proven physical substance. Exploration and appraisal costs are held, un-depreciated, until such a time as the exploration phase on the licence area is complete or commercial reserves have been discovered.

If no commercial reserves exist, then that particular exploration/appraisal effort was "unsuccessful" and the costs are written off to the income statement in the period in which the evaluation is made. The success or failure of each exploration/appraisal effort is judged on a field-by-field basis.

Morocco - Guercif Licence

Predator has a 75% interest in the Guercif Licence together with its partner ONHYM, the State oil company.

The capitalised value at 31 December 2025 of the Guercif licence costs is £19,397,727.

Exploration and Appraisal activity on Guercif

The current focus of activity is the evaluation of a number of potential gas and helium reservoirs based on NuTech petrophysical interpretation from 339 to 1425 metres measured depth in MOU-1, MOU-3 and MOU-4 and gas and helium samples collected in MOU-3. The rigless testing programme completed in Q3 2025 established for the first time the extent of reservoir formation damage caused by over-balanced drilling with excessive mud weights. A re-engineered appraisal/development well (MOU-6) is being programmed for 2026. An application to extend the First Extension Period of the Guercif Petroleum Agreement to 5 November 2026 has been submitted to ONHYM and the Ministry. This will enable a potential application for an Exploitation Concession to be submitted by 5 October 2026 for a pilot CNG development. As a consequence of these positive actions, the Group has been able to commence negotiations with a potential joint venture partner willing to finance the MOU-6 drilling and the CNG pilot development. In addition, under the terms of the agreement being negotiated, up to USD24.6m in past costs will be refunded, subject to contract. These include the costs of MOU-1, MOU-3 and MOU-4 and additionally MOU-2 (which penetrated a much thicker section of the interval where helium was sampled in MOU-3) and MOU-5 (which discovered salt and which the potential joint venture partner wishes to consider as an area for potential gas storage in salt caverns).

The MOU-1 well drilled in 2021 was completed for rigless well testing on the basis of the presence of formation gas and petrophysical wireline log interpretation by NuTech indicating gas in the primary and secondary pre-drill reservoir targets.

The well remains a potential gas producer. MOU-6, when drilled, will potentially provide the information to engineer a small-scale frac job to reach beyond the zone of reservoir formation damage.

The MOU-2 well was drilled in January 2023. The Company announced on 25 January 2023 that the MOU-2 well had been suspended at 1,260 metres measured depth above the primary pre-drill reservoir target. Subsequent re-interpretation of the wireline log whilst drilling and correlation with the later MOU-4 well log confirmed that the primary target was penetrated and contained a thick sand sequence equivalent of the Moulouya Fan interval that sampled helium and biogenic gas in MOU-3.

A re-entry of MOU-2 to sidetrack to the deeper target can be considered if the re-engineered MOU-6 well is drilled without encountering previous drilling issues.

3 gas samples were collected whilst drilling MOU-2 in the shallow section above 700 metres which is likely an extension of the formation gas shows encountered in MOU-3 at shallower depths down to 950 metres and including the "A" Sand, Ma Sand and TGB-6 Sand.

The MOU-3 well was drilled in June 2023 to a depth of 1,509 metres (TVD MD) and encountered gas shows in multiple zones including the primary targets, the Moulouya Fan sands and the Ma and TGB-6 sands, and a new shallow "A" Sand reservoir interval.

The well was completed for rigless testing.

The well remains a potential gas producer. MOU-6, when drilled, will potentially provide the information to engineer a small-scale frac job to reach beyond the zone of reservoir formation damage.

The MOU-4 well was drilled in July 2023 and confirmed the extension of the Moulouya Fan further to the southeast than previously prognosed. Better reservoir quality was interpreted as a result of the NuTech petrophysical analysis of the wireline logs. NuTech also indicated good gas saturations beyond the zone of suspected reservoir formation damage.

The well remains a potential gas producer. MOU-6, when drilled, will potentially provide the information to engineer a small-scale frac job to reach beyond the zone of reservoir formation damage.

The MOU-5 well was drilled in February 2025 and suspended for a possible re-entry. The primary target, a Jurassic carbonate bank, was encountered deeper than prognosed due to the presence of allochthonous salt.

MOU-5 remains a candidate for re-entry and side-tracking updip to the Jurassic carbonate objective and deepening to an underlying potential TAGI Triassic reservoir with a thick salt seal. The thickness of the potential salt will determine whether or not the interval can be considered a candidate for gas storage.

Guercif Permit - Summary

The Company has considered the possible indicators of potential impairment under IFRS6, and none of these applies to the Company's interest in the Guercif licence as at 31 December 2025, or currently, specifically -

· The Guercif licence has not expired. The permit was granted in 2019 and is valid until 2028, after a one-year force majeure extension due to COVID. An application has been made to extend the First Extension Period from 5 March 2026 to 5 November 2026. This would facilitate the drilling of the MOU-6 appraisal/development well and a subsequent application for an Exploitation Concession.

· Evaluation of the prospectivity of the licence area and including the Moulouya Fan, Ma Sand, TGB-6 Sand and "A" Sand and the Jurassic carbonate and the new Triassic prospect is ongoing. Substantive MOU-6 appraisal/development drilling and testing expenditure is planned for on the licence. This program is budgeted for on the basis of a successful conclusion of the current negotiations with a potential joint venture partner in a CNG gas development.

· There is no indication from data obtained and activities to date that a development in the area is likely to proceed where the carrying amounts of the E&E assets is unlikely to be recovered in full. An updated Independent Technical Report ("ITR") by Scorpion Geoscience Ltd., incorporating the information gathered from the 2025 MOU-3 rigless testing programme, will be available during Q1 2026. The ITR will focus on the gas resources in the MOU-3 area to be appraised by MOU-6 for a CNG development decision, but will also include the wider area should the testing and logging programme planned for MOU-6 demonstrtae a single vertical gas column in the Ma and TGB-6 Sands.

Accordingly the Directors believe that there are no indicators of impairment of the Company's Guercif assets at the current time, and no impairment adjustment is appropriate.

Trinidad - Cory Moruga Licence

The Company announced on 7th November 2023 the acquisition of T Rex Resources (Trinidad) Limited ("TRex") from Challenger Energy Group ("CEG"). TRex hold an 83.8% interest in the Cory Moruga licence onshore Trinidad. Consent for Completion of the Sale and Purchase Agreement executed between T-Rex Resources Trinidad Limited, a wholly owned subsidiary of Predator Oil & Gas Holdings Plc, and the third-party Trinidad partner for the assignment of the remaining 16.2% in Cory Moruga "E" Block was given by the Ministry of Energy and Energy Industries (*MEEI") in August 2024. The Cory Moruga Exploration and Production Licence includes the Snowcap oil discovery where oil was previously produced on test from Snowcap-1 and oil was encountered in Snowcap-2 but inconclusively tested due to operational issues impacting a previous operator. The consideration comprised an immediate payment of $1m to CEG and $1m payment directly to the MEEI as well as resolution of various liabilities between TRex and Predator and between TRex and MMEI.

The current capitalised value of the Cory Moruga licence is £5,197,428.

An appraisal well, Snowcap-3, is scheduled for 2026.

The results of an independent Technical Report ("ITR") by Scorpion Geosciences Ltd, dated 20 February 2026, for the Cory Moruga licence with project economics, supports a valuation of NPV @10% of £67m. The aforesaid appraisal well is intended to prove up the P90 resources case with an NPV @10% discount of £67 Million or 12 pence per share based on £159m undiscounted post-tax profits for the Base Case of approximately 8.33MMbbl recoverable using a 15 year production profile peaking at 3,500bopd which equates to c. 58.2% of available 2C + P50 (Unrisked) Prospective Resources.

In the ITR significant upside potential is now recognised with respect to deeper Cretaceous sand fairways which may be present within the Company's acreage. Ongoing work seeks to confirm whether this observation is part of the World Class discovery trend currently being worked by likes of ExxonMobil along the coast of Guyana, Venezuela and Trinidad.

Cory Moruga Licence - Summary

The Company has considered the possible indicators of potential impairment under IFRS6, and none of these applies to the Company's interest in the recently acquired Cory Moruga licence as at 31 December 2025, or currently.

Specifically -

· The licence is current and not due to expire - The Initial Work Program has been agreed with the MEEI for a period of three years to November 2026. An extension beyond this date is pending approval.

· The Company has outlined a Field Development Plan to the MEEI which includes up to 20 development wells as well as a longer-term CO2 EOR scheme. This will not be considered for implementation until after the Snowcap-3 appraisal well results in 2026.

· The current carrying value is well supported by the Scorpion Geoscience Independent Technical Report ("ITR").

Accordingly, the Directors believe that there are no indicators of impairment of the Company's Cory Moruga assets at the current time, and no impairment adjustment is appropriate.

Other Trinidad

The 29th August 2025 acquisitions that were concluded in Trinidad included the Goudron and Inniss-Trinity Incremental Production Sharing Contracts with Heritage and the Icacos Exploration and Production Licence with MEEI. These acquisitions gave rise to intangible assets totalling £1,591,745. This is shown in the above table under 'Other Trinidad'.

This valuation was determined based an innovative Master Services Agreement with NABI Construction for a 'cost-free to Predator' production ramp-up and revenue generation.

NABI is an exceptionally low-cost local operator which has transformed the economics for rehabilitating mature oil fields.

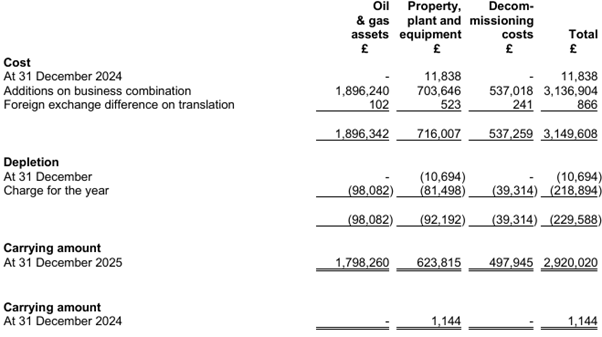

17. Tangible fixed assets

18. Investments

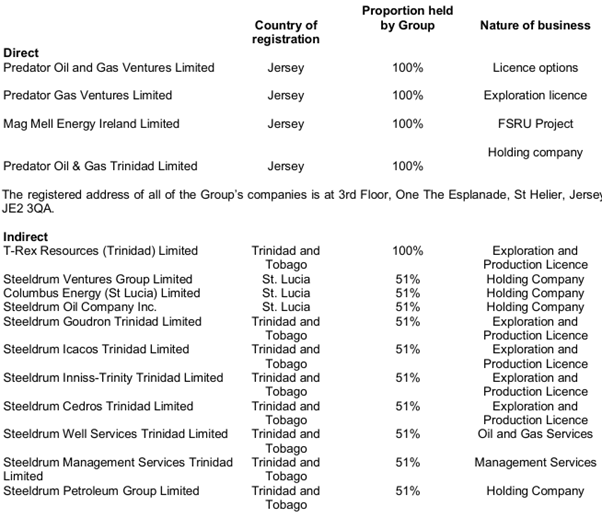

The principal subsidiaries of Predator Oil and Gas Holdings Plc, all of which are included in these consolidated Annual Financial Statements, are as follows:

All of the above indirect companies are included in these consolidated financial statements.

19. Acquisitions

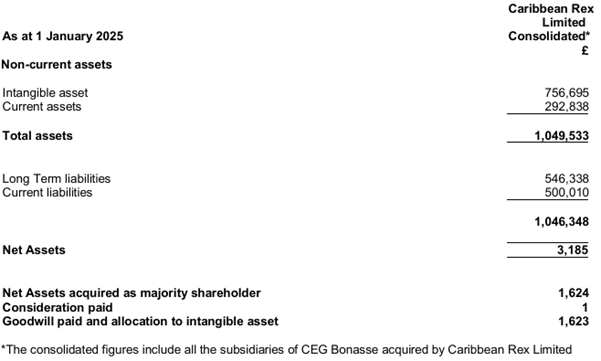

a. Acquisition of Caribbean Rex Limited (Steeldrum Ventrues Group Limited)

In January 2025 a Group subsidiary, TRex Resources Trinidad Limited acquired at an acquisition cost of USD1, 51% of the equity of Caribbean Rex Limited, later renamed to Steeldrum Ventures Group Limited, and its 100% owned subsidiary, CEG Bonasse Limited, later renamed to Steeldrum Cedros Limited.

An assessment of the fair value assets and liabilities of Caribbean Rex Limited and CEG Bonasse Limited have been undertaken. The board has determined that these assets taken as an integrated set of activities are capable of being managed and conducted for the purpose of providing a return and therefore constitute a business. Accordingly, the transaction has been accounted for in accordance with IFRS 3 'Business Combinations' which requires the assets acquired and liabilities assumed to be recognised on the acquisition date at their fair value.

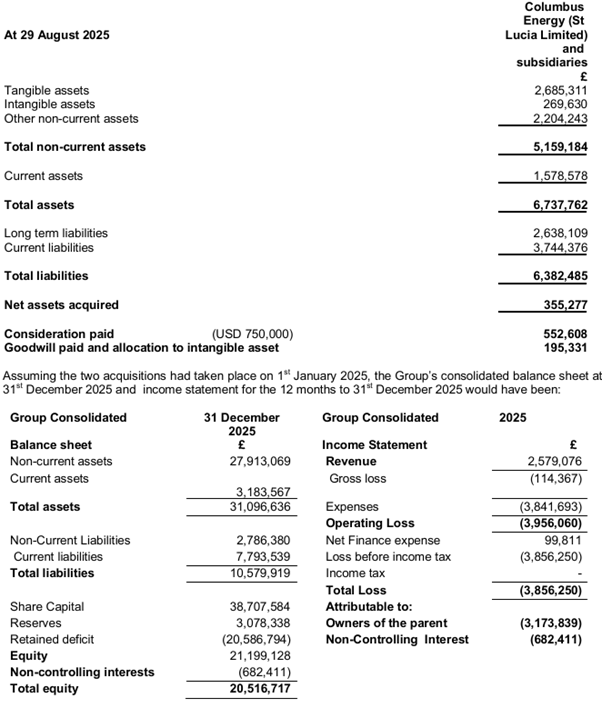

Acquisition of Columbus Energy (St Lucia) Limited

On 1 September 2025 a 51% owned Group subsidiary, Caribbean Rex Limited, later renamed to Steeldrum Ventures Group Limited, announced that the previously announced transaction for the purchase of the entirety of Challenger Energy Group Plc's St. Lucia-domiciled subsidiary company, Columbus Energy (St. Lucia) Limited ("CEG Trinidad") and its subsidiaries' business and operations in Trinidad and Tobago had been completed, with an effective date of 29 August 2025, following the receipt of all regulatory consents:

1. At completion, Challenger Energy Group Plc ("Challenger") had been paid a cash equivalent of USD250,000 (£182,238) in 4,441,641 Predator Oil & Gas Plc ordinary shares which were issued to Challenger and USD500,000 (£370,370) had been paid in cash