30th Jun 2026 14:08

30 June 2026

Bezant Resources Plc

("Bezant" or the "Company")

Final Results for year ended 31 December 2025

Bezant Resources plc ("Bezant" or the "Company"), the exploration and development company with projects located in Namibia, Botswana and Zambia reports its audited full year results for the year ended 31 December 2025.

The Annual Report and Financial Statements for the year ended 31 December 2025 are being sent to shareholders and will shortly be available on the Company's website https://www.bezantresources.com/

Please note that page references in the text below refer to the page numbers in the Annual Report and Financial Statements.

The audited financial information contained in this announcement does not constitute the Company's full financial statements for the year ended 31 December 2025, but is derived from those financial statements, approved by the board of directors. The auditors' report on the 2025 financial statements was unqualified and did not contain any statement under section 498(2) or (3) of the Companies Act 2006 but did as in 2024 contain a 'material uncertainty' paragraph relating to going concern. The full audited financial statements for the year ended 31 December 2025 will be delivered to the Registrar of Companies and filed at Companies House.

The information contained within this announcement is deemed by the Company to constitute inside information as stipulated under the Market Abuse Regulations (EU) No. 596/2014 as it forms part of UK Domestic Law pursuant to the Market Abuse (Amendment) (EU Exit) regulations (SI 2019/310).

Bezant Resources Plc Colin Bird Executive Chairman |

| |

Beaumont Cornish (Nominated Adviser) Roland Cornish / Asia Szusciak | +44 (0) 20 7628 3396 | |

Novum Securities Limited (Joint Broker) Jon Belliss |

+44 (0) 20 7399 9400 | |

Shard Capital Partners LLP (Joint Broker) Damon Heath |

+44 (0) 20 7186 9952 |

or visit http://www.bezantresources.com

Beaumont Cornish Limited ("Beaumont Cornish") is the Company's Nominated Adviser and is authorised and regulated by the FCA. Beaumont Cornish's responsibilities as the Company's Nominated Adviser, including a responsibility to advise and guide the Company on its responsibilities under the AIM Rules for Companies and AIM Rules for Nominated Advisers, are owed solely to the London Stock Exchange. Beaumont Cornish is not acting for and will not be responsible to any other persons for providing protections afforded to customers of Beaumont Cornish nor for advising them in relation to the proposed arrangements described in this announcement or any matter referred to in it.

Chairman's Statement

For the year ended 31 December 2025

Dear Shareholder,

The period under review has been an exciting and progressive period for the company. Generally surrounding the activities at the Hope and Gorob gold and copper project in Namibia.

We have had many material technical issues to satisfy, with the most important being testing that ore sorting works for the project and achieves the necessary ore recovery with the minimum of waste rejection. Our testing was carried out on a full-sized ore sorter and the final result demonstrated comprehensively that ore sorting will provide the necessary solution.

Having satisfied this material factor, we had the confidence to make the decision to mine and we thus moved on to further verification, expansion and test work on all other factors, completing our engineering and optimisation studies.

A further important aspect of course was the financing. We announced on 31 October 2025 that we had signed a binding term sheet for a US$7 million facility and post balance sheet on 11 June 2026, we announced the terms of the facility agreement signed with Hartree Metals for a USD7million. This facility will be paid in tranches through to the production of concentrates. The project however, commenced in earnest during the period under review, with all major contractors identified and selected including, but not limited to the earthmoving contractor, Unitrans, Steinhart the provider of the ore sorting equipment, Weir the provider of the pre-sorting crushing and screening equipment and USM for the upgrading of the NLZM Processing Plant acquired in December 2025 when we completed the acquisition of Namib Lead and Zinc Mining (Proprietary) Limited (since renamed Tsoaxaub Metals (Proprietary) for cash consideration of US$2.5 million. We will in the future also have to pay from operating income a combination of payments based on tonnage of rock treated by the NLZM Processing Plant and copper revenue royalties.

The formal ground breaking ceremony for the Hope and Gorob mine site was held last week and well attended by community members, government officials, contractor representatives and our growing number of Namibian employees. Mining development operations have already been well underway for several months at the Hope and Gorob mine site as are the upgrade and modifications work to the NLZM Processing Plant and we are well on course for first concentrate production by the end of third quarter 2026 latest.

During the period under review metal prices improved dramatically and by year end our basket of metals per tonne was valued some 60% higher than our original estimations used for the decision to mine analysis. This of course, has added to our confidence and applied our joint minds as to how we might make the operation larger in the shorter term. As soon as the operation becomes cash positive and we can release funds for drilling we will carry out further exploration on the Hope and Gorob licence and beyond where we hold exploration licences.

We are confident that we can considerably increase mineral resources and therefore the size of the operation over the coming years.

During the period under review and currently, there has been considerable increase in world geo-political tension as well as increasing commercial uncertainty relative to the USA president, Donald Trump, continually changing his stance on tariffs. In fairness, the president of the US has brought considerable attention to the fact that strategic and critical metals are generally located in the wrong countries relative to geo-political tension and has taken, and is taking, considerable financial steps to address the imbalance.

The Bezant board is convinced that the fundamentals for copper remain excellent, based as much on shortage of new supply as on the increase in demand. There is an acute shortage of major new copper projects, and we feel projects such as Hope and Gorob, which is expandable, will do much assist tomorrow's supply, although the supply will still be insufficient to meet new demand.

We are proud as an AIM company, to be one of the few companies that will take an exploration project through to production and it is our intention to continue with that model wherever the opportunity presents itself and to seek out other similar opportunities.

The Botswana manganese project has been subject to desk research and fieldwork, and it is our intention to carry out further drilling particularly at the borrow pit site to ascertain the overall production potential.

We have secured a very interesting exploration project in the Eastern Foreland of Zambia and have identified targets that are ready for drilling. We look forward to doing our first reconnaissance drilling towards the end of the dry season.

I would like to thank my fellow directors and management for their splendid efforts during the year and sincerely hope that we provide shareholders with a steady stable producing copper/gold mine before the end of the third quarter this year.

Yours sincerely,

Mr Colin Bird

Executive Chairman

30 June 2026

Board of directors

For the year ended 31 December 2025

Mr Colin Bird (Executive Chairman) (Appointed 2 March 2018)

Experience and Expertise

Executive Chairman Colin is a chartered mining engineer and a Fellow of the Institute of Materials, Minerals and Mining with more than 40 years' experience in resource operations management, corporate management, and finance. Colin has multi commodity mine management experience in Africa, Spain, Latin America and the Middle East. He has been the prime mover in a number of public company listings in the UK, Canada and South Africa. His most notable achievement was founding Kiwara Resources Plc and selling its prime asset, a copper property in Northern Zambia, to First Quantum Minerals for US$260 million in November 2009 which closed in January 2010.

Other current directorships

Includes African Pioneer Plc, Kendrick Resources Plc, Bird Leisure and Admin (Pty) Ltd, Galileo Resources Plc, Galileo Resources South Africa (Pty) Ltd, Glenover Phosphate (Pty) Ltd, Holyrood Platinum (Pty) Ltd, Lion Mining Finance Ltd , Mitte Resources Investment Ltd, New Age Metals Inc, Revelo Resources Corp, Sandown Holdings, Shamrock Holdings Inc, Umhlanga Lighthouse Café CC, Virgo Business Solutions (Pty) Ltd, Xtract Resources Plc, Camel Valley Holdings Inc, Crocus-Serv Resources (Pty) Ltd, Africibum (Pty) Ltd, Enviro Zambia Ltd, and Eureka Mine International Ltd.

Former directorships in the last 5 years

Braemore Resources Ltd, Camel Valley Holdings Inc, Crocus-Serv Resources (Pty) Ltd, Dullstroom Plats (Pty) Ltd, Enviro Mining Ltd, Enviro Processing Ltd, Enviro Props Ltd, Galagen (Pty) Ltd, Kabwe Operations Mauritius, Maude Mining & Exploration (Pty) Ltd, NewPlats (Tjate) (Pty) Ltd, Newmarket Holdings, Tjate Platinum Corporation (Pty) Ltd, Windsor Platinum Investments (Pty) Ltd, Windsor SA Pty Ltd, Tara Bar and Restaurant CC, Add X Trading 810 CC, Afminco (Pty) Ltd, Dialyn Café CC, Emanual Mining and Exploration (Pty) Ltd, Europa Metals Ltd, Isigidi Trading 413 CC, Jubilee Metals Group Plc, Jubilee Smelting & Refining (Pty) Ltd, Jubilee Tailings Treatment Company (Pty) Ltd, M.I.T. Ventures Group, Mokopane Mining & Exploration (Pty) Ltd, NDN Properties CC, Orogen Gold Plc, Pilanesberg Mining Co (Pty) Ltd, Pioneer Coal (Pty) Ltd, PowerAlt (Pty) Ltd, SacOil Holdings Ltd, Sovereign Energy Plc, Thos Begbie Holdings (Pty) Ltd, Tiger Alpha PLC, ,Mistral Resource Development Corporation ltd, Galileo Resources South Africa (Pty) Ltd and Holyrood Platinum (Pty) Ltd.

Special responsibilities

Executive Chairman of the Board & Remuneration Committee and member of the Audit Committee.

Interests in shares and options as at the date of these accounts

1,113,969,885 ordinary shares in the capital of the Company of which 30,769,231 were acquired on 31 March 2026.

60,000,000 warrants expiring on 18 December 2026 which give the right to subscribe for ordinary shares at a price of 0.06p per share.

100,000,000 warrants issued on 3 January 2025 expiring on 3 January 2028 which give the right to subscribe for ordinary shares at a price of 0.04p per share.

Interests in shares and options (continued)

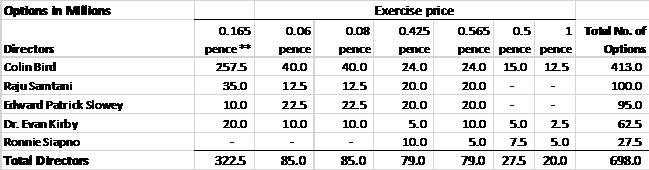

The following options over ordinary shares in the Company which all expire 21 June 2028

12,500,000 at an exercise price of 1 pence.

15,000,000 at an exercise price of 0.5 pence.

24,000,000 at an exercise price of 0.425 pence per share.

24,000,000 at an exercise price of 0.564 pence per share.

40,000,000 at an exercise price of 0.08 pence per share

40,000,000 at an exercise price of 0.06 pence per share

** 257,500,000 at an exercise price of 0.165 pence per share

** Issued 3 March 2026, 50% of these options will vest upon the breaking of ground at the Hope and Gorob mine site and the balance of 50% will vest upon the first sale of concentrate mine from the Hope and Gorob project

Dr. Evan Kirby (Non-Executive Director) (Appointed 4 December 2008)

Experience and Expertise

Dr Kirby, is a metallurgist with over 40 years of international involvement. His career started in South Africa with Impala Platinum, Rand Mines and then Rustenburg Platinum Mines. In 1992, he moved to Australia to work for Minproc Engineers and then Bechtel Corporation. After leaving Bechtel in 2002, he established his own consulting company and continued with international mining project involvement. Evan's personal "hands on" experience covers the financial, technical, engineering and environmental issues associated with a wide range of mining and processing projects.

Other current directorships

Non-executive director of Europa Metals Ltd (listed on AIM and AltX of the JSE). Kendrick Resources Plc (listed on LSE), and Linq Minerals (listing on ASX), and Director of private company, Metallurgical Management Services Pty Ltd

Former directorships in the last 5 years

Technical director of Jubilee Metals Group PLC (Aim traded).

Special responsibilities

Chairman of the Audit Committee and member of the Remuneration Committee.

Interests in shares and options as at the date of these accounts

65,710,062 fully paid ordinary shares in Bezant Resources Plc.

The following options over ordinary shares in the Company which all expire 21 June 2028

2,500,000 at an exercise price of 1 pence.

5,000,000 at an exercise price of 0.5 pence.

10,000,000 at an exercise price of 0.425 pence per share.

10,000,000 at an exercise price of 0.564 pence per share.

10,000,000 at an exercise price of 0.08 pence per share

10,000,000 at an exercise price of 0.06 pence per share

**20,000,000 at an exercise price of 0.165 pence per share

** Issued 3 March 2026, 50% of these options will vest upon the breaking of ground at the Hope and Gorob mine site and the balance of 50% will vest upon the first sale of concentrate mine from the Hope and Gorob project

Mr Ronnie Siapno (Non-Executive Director) (Appointed 25 October 2007)

Experience and Expertise

Mr Siapno, graduated from the Saint Louis University in the Philippines in 1986 with a Bachelor of Science degree in Mining Engineering and is a lifetime member of the Philippine Society of Mining Engineers. Since graduation, he has held various consulting positions such as Mine Planning Engineer to Benguet Exploration Inc., Mine Production Engineer to Pacific Chrome International Inc., Exploration Engineer to both Portman Mining Philippines Inc. and Phoenix Resources Philippines Inc. and Geotechnical Engineer to Pacific Falkon Philippines Inc.

Other current directorships

President of Crescent Mining and Development Corporation, Director of Gibbous Holdings , Inc. Non-Executive President and Director of Cleangrean Solutions, Inc.

Former directorships in the last 5 years

Former director of Asean Copper Investment Ltd.

Special responsibilities

Member of the Remuneration Committee.

Interests in shares and options as at the date of these accounts

1,333,334 fully paid ordinary shares in Bezant Resources Plc.

The following options over ordinary shares in the Company which all expire 21 June 2028

5,000,000 at an exercise price of 1 pence per share.

7,500,000 at an exercise price of 0.5 pence per share.

5,000,000 at an exercise price of 0.425 pence per share.

5,000,000 at an exercise price of 0.564 pence per share.

Mr Raju Samtani (Finance Director) (appointed 26 October 2020)

Experience and Expertise

Mr. Samtani is an Associate Chartered Management Accountant and also currently Finance Director of African Pioneer Plc (listed on the LSE) . Mr. Samtani's previous experience includes being one of the founder shareholders and Finance Director of Kiwara Plc which was acquired by First Quantum Minerals Ltd in January 2010. Earlier in his career he spent three years as Group Financial Controller at marketing services agency - WTS Group Limited ("WTS"), where he was appointed by the Virgin Group to oversee their investment in WTS. During the course of his career, Raju has been involved in senior managerial positions for several AIM/Johannesburg Stock Exchange listed companies predominantly in the natural resource sector and has also had roles in FCA compliance work in the investment business sector.

Other current directorships

None

Former directorships in the last 5 years

Tiger Alpha Plc and Myning Ventures Ltd

Special responsibilities

Mr. Samtani is the Company's Finance Director and member of the Audit Committee.

Interests in shares and options as at the date of these accounts

336,933,642 fully paid ordinary shares in Bezant Resources Plc of which 30,769,231 were acquired on 31 March 2026.

48,000,000 warrants expiring on 18 December 2026 which give the right to subscribe for ordinary shares at a price of 0.06p per share.

50,00,000 warrants issued on 3 January 2025 expiring on 3 January 2028 which give the right to subscribe for ordinary shares at a price of 0.04p per share.

The following options over ordinary shares in in the Company which all expire 21 June 2028

20,000,000 at an exercise price of 0.425 pence per share.

20,000,000 at an exercise price of 0.564 pence per share.

12,500,000 at an exercise price of 0.08 pence per share

12,500,000 at an exercise price of 0.06 pence per share

**35,000,000 at an exercise price of 0.165 pence per share

** Issued 3 March 2026, 50% of these options will vest upon the breaking of ground at the Hope and Gorob mine site and the balance of 50% will vest upon the first sale of concentrate mine from the Hope and Gorob project

Mr Edward Slowey (Technical Director) (appointed 26 October 2020)

Experience and Expertise

Mr. Slowey holds a BSc degree in Geology from the National University of Ireland and is a founder member of The Institute of Geology of Ireland. Mr. Slowey has more than 40 years' experience in mineral exploration, mining and project management including working as a mine geologist at Europe's largest zinc mine in Navan, Ireland and was exploration manager for Rio Tinto in Ireland for more than a decade, which led to the discovery of the Cavanacaw gold deposit. Mr. Slowey is an experienced exploration geologist, having worked in Africa, Europe, America and the FSU and his experience includes joint venture negotiation, exploration programme planning and management through to feasibility study implementation for a variety of commodities. As a professional consultant, Mr. Slowey's work has included completion of CPR's and 43-101 technical reports for international stock exchange listings and fundraising, while also undertaking assignments for the World Bank and European Union bodies. Mr. Slowey has also served as director of several private and public companies, including the role of CEO and Technical Director at AIM-listed Orogen Gold Plc which discovered the Mutsk gold deposit in Armenia.

Other current directorships

Silver Investments Limited

Galileo Resources plc

St Vincent Minerals US Inc

Camel Valley Holdings Inc

Crocus-Serv Resources Pty Ltd

Virgo Business Solutions Pty Ltd

St Vincent Minerals Inc

Former directorships in the last 5 years

None

Special responsibilities

Mr. Slowey is the Company's Technical Director with oversight over the Company's projects.

Interests in shares and options as at the date of these accounts

89,625,000 fully paid ordinary shares in Bezant Resources Plc.

The following options over ordinary shares in the Company which all expire 21 June 2028

20,000,000 at an exercise price of 0.425 pence per share.

20,000,000 at an exercise price of 0.564 pence per share.

22,500,000 at an exercise price of 0.08 pence per share

22,500,000 at an exercise price of 0.06 pence per share

**10,000,000 at an exercise price of 0.165 pence per share

** Issued 3 March 2026, 50% of these options will vest upon the breaking of ground at the Hope and Gorob mine site and the balance of 50% will vest upon the first sale of concentrate mine from the Hope and Gorob project

Strategic report

For the year ended 31 December 2025

Principal activity

The Company is registered in England and Wales, having been first incorporated on 13 April 1994 under the Companies Act 1985 with registered number 02918391 as a public company limited by shares, in the name of Yieldbid Public Limited Company. On 19 September 1994, the Company changed its name to Voss Net Plc, with a second change of name to that of Tanzania Gold Plc on 27 September 2006. On 9 July 2007, the Company adopted its current name of Bezant Resources Plc.

The Company was listed on AIM, a market operated by the London Stock Exchange, on 14 August 1995 and its FTSE Sector classification is that of Industrial Metals and Mining and FTSE Sub-sector that of General Mining.

The Group's strategy is to build a diversified portfolio of high-potential mineral assets across southern Africa by advancing exploration and development projects with a focus on copper and gold assets, with the aim of creating long-term value through resource discovery, licensing optimisation, and project advancement to commercial production.

The principal activity of the Group is natural resource exploration and development in; Namibia where the Hope and Gorob copper gold project has mining and exploration licences; in Zambia where it has an exploration licence in the Eastern Foreland and in Botswana where its Kanye project has a manganese exploration licence.

Review of Business and future prospects

The Chairman's statement contains a review of 2025 and refers to the Company's focus on its copper and gold asset portfolio and in particular the Hope and Gorob project in Namibia. During the coming year the Company intends to focus on the development of the Hope and Gorob project into an operating mine and its other projects in Southern Africa but will also consider other opportunities consistent with its Southern Africa focus.

Principal risks and uncertainties facing the Company

The principal risks and uncertainties facing the Company are disclosed in the Directors' report on pages 22 to 28.

Performance of the Company

The Company is an exploration and development entity whose assets are not yet at the production stage. Currently, no revenue has been generated from such projects therefore standard financial KPIs as per the table below are less relevant and the key performance indicators for the Company are therefore linked to the achievement of project milestones to increase overall enterprise value; for assets held as exploration and evaluation assets these are as detailed in note 12.1 and in note 13 in relation to the mine development asset

Financial highlights:

· Consolidated profit: £2,002K after tax (2024: £1,015k - loss)

· Approximately £430k cash at bank at the period end (2024: £88k)

· The basic and diluted profit / (losses) per share are summarised in the table below

Profit (Loss) per share (pence) | |||

2025 | 2024 | ||

Basic | Note 7 | 0.0124p | (0.01)p |

Diluted | 0.0088p | (0.01)p |

· Net assets as at 31 December 2025 was £8.3m (31 December 2024 £5m)

Significant milestone achievements during the year included the award in June 2025 of Mining Licence for ML 246 in relation to the Hope and Gorob project in Namibia which is valid until 31 March 2040 and the completion in December 2025 of the acquisition of a 90% shareholding in Namib Lead and Zing Mining (Proprietary) Limited (since renamed Tsoaxaub Metals (Proprietary) Limited) which owns the NLZM Processing Plant that will be used to process pre-concentrate from the Hope and Gorob mine.

Directors' section 172 statement

The following disclosure describes how the Directors have had regard to the matters set out in section 172 and forms the Directors' statement required under section 414CZA of The Companies Act 2006. This reporting requirement is made in accordance with the new corporate governance requirements identified in The Companies (Miscellaneous Reporting) Regulations 2018, which apply to company reporting on financial years starting on or after 1 January 2019.

The matters set out in section 172(1) (a) to (f) are that a Director must act in the way they consider, in good faith, would be most likely to promote the success of the Company for the benefit of its members as a whole, and in doing so have regard (amongst other matters) to:

a. the likely consequences of any decision in the long term.

b. the interests of the Company's employees.

c. the need to foster the Company's business relationships with suppliers, customers and others;

d. the impact of the Company's operations on the community and the environment;

e. the desirability of the Company maintaining a reputation for high standards of business conduct; and

f. the need to act fairly between members of the Company.

The analysis is divided into two sections, the first to address Stakeholder engagement, which provides information on stakeholders, issues and methods of engagement. The second section addresses principal decisions made by the Board and focuses on how the regard for stakeholders influenced decision-making.

Section 1: Stakeholder mapping and engagement activities within the reporting period

The Company continuously interacts with a variety of stakeholders important to its success, such as equity investors, employees, government bodies, local community and professional service providers. The Company works within the limitations of what can be disclosed to the various stakeholders with regards to maintaining confidentiality of market and/or commercially sensitive information.

Who are the key stakeholder groups | Why is it important to engage this group of stakeholders | How did Bezant engage with the stakeholder group | What resulted from the engagement |

Equity investors

All significant shareholders that own more than 3 per cent. of the Company's shares are listed in the Directors' Report.

Currently, no revenue is generated from the Company's projects. As such, existing equity investors and potential investment partners are important stakeholders. | As an exploration and development company without a revenue generating project access to capital is of vital importance to the long-term success of our business.

We are seeking to promote an investor base that is interested in a long term holding in the Company and will support the Company in achieving its strategic objectives.

| The key mechanisms of engagement include • The AGM and Annual and Interim Reports. • Investor roadshows and presentations. • Access to the Company's brokers and advisers • Regular news and project updates.

| The Company engaged with investors on topics of strategy, governance, project updates and performance.

Please see "Relationship with shareholders" section of the Corporate governance report which starts on page 31

|

Who are the key stakeholder groups | Why is it important to engage this group of stakeholders | How did Bezant engage with the stakeholder group | What resulted from the engagement |

Employees At the period end the group had one part-time employee in the U.K. and one full-time employee in Namibia and at the year-end the Company had five directors 4 of whom are resident outside the U.K. with one resident in the U.K.

|

The number of and location of future employees will be dependent upon the development of its projects which at the date of this report are situated in Namibia, Zambia and Botswana. The Directors consider workforce issues holistically for the Group as a whole and the Company's long-term success in developing its projects will be predicated on the development of a local workforce in the countries of its projects. (see the principal risk and uncertainty starting on page 22). |

• The Company maintained an open line of communication between its, professional service providers and Board of Directors. • The Executive Chairman reported regularly to the Board, including the provision of board information. • There is a formalised director induction into the Company's corporate governance policies and procedures. |

The Board met to discuss long term remuneration strategy. Board reporting has been optimised to include sections on engagement with local communities and prospects for future employment. Directors trained in aspects of corporate policies and procedures to engender positive corporate culture aligned with the Company code of conduct. Meetings were held with directors to provide project updates and ongoing business objectives.

|

Who are the key stakeholder groups | Why is it important to engage this group of stakeholders | How did Bezant engage with the stakeholder group | What resulted from the engagement |

Governmental bodies The Group is impacted by national, regional and local governmental organisations in the UK where it is incorporated and in countries in which it has interests in projects or investments which at the date of this report includes, Namibia, Zambia and Botswana |

The Group will only be able to develop its projects once it receives relevant licences and permits from local governments to explore, mine and undertake mineral processing. |

The Group maintained its good relations with the respective government bodies and frequently communicates progress. • The Group engages with the relevant departments of the relevant government in order to progress the operational licences it will require • The Group engages local in-country experts to advise it on regulatory matters.

|

The Group has given general corporate presentations to senior government officials in Namibia.

To date, the Group has received its requisite, exploration and mining licences and environmental and land use permits to enable its exploration and mine development activities. |

Community The local community at the Company's projects which as at the date of this report were in Namibia, Zambia and Botswana. |

The community provides social licence to operate. We need to engage with the local community to build trust. Having the community's trust will mean it is more likely that any fears the community has can be assuaged and our plans and strategies are more likely to be accepted. Community engagement will inform better decision making.

The Company will in due course have a social and economic impact on the local community and surrounding area. The Company is committed to ensuring sustainable growth minimising adverse impacts. The Company will engage these stakeholders as appropriate.

|

• The Company identifies key stakeholders within the local community based on work programs within the reporting period. • Bezant's modus operandi is to have open dialogue with the local government and community leaders regarding project development. • The Company has existing CSR policies and management structure at corporate level. The Company will expand on these policies and structures at a local project level as the Company moves into further exploration activities and ultimately into construction and then production. |

The Company has systems in place to engage with the local community as part its sustainability initiatives.

Stakeholder identification enables the Company to identify representatives of stakeholder groups and community groups to engage with as it develops its projects.

|

Who are the key stakeholder groups | Why is it important to engage this group of stakeholders | How did Bezant engage with the stakeholder group | What resulted from the engagement |

Professional service providers During the exploration and development phase of projects, we will be using key professional service providers who provide drilling, geochemical, geological analysis, assaying and other services under commercial contracts.

At a local level, we also partner with a variety of smaller companies / providers, some of whom are independent, or family run businesses. |

Our professional service providers are fundamental to ensuring that the Company can complete projects on time and budget. Using quality professional service providers ensures that as a business we meet the high standards of performance that we expect of ourselves and those we work with. |

• The Company continues to work closely with professional service providers to meet deliverables. • One on one meetings and regular project and work assignment updates with professional service providers. |

The use of third-party i) exploration services for analysis and field operations and ii) engineer and mine design services for mine licence applications and mine planning as required rather than the Company maintaining its own full time in-house exploration and mine development department.The use of third-party drilling contractors rather than conducting its own exploration activities in multiple countries with an in-house team provides very significant cost savings to the Company whilst enabling the Company to diversify its project and jurisdiction risks. |

Section 2: Principal decisions by the board post year end

Principal decisions are defined as both those that have long-term strategic impact and are material to the Group, but also those that are significant to key stakeholder groups. In making the following principal decisions, the Board considered the outcome from its stakeholder engagement, the need to maintain a reputation for high standards of business conduct and the need to act fairly between the members of the Company. The Company makes regular announcements of decisions that strategically impact the Company with decisions during the year being reported in the Chairman's letter to shareholders (page 4) and Directors' report on page 16. Decisions post the year end are referred to in note 26 to the financial statements which is a summary of post balance sheet events.

On behalf of the Board

Mr Colin Bird

Executive Chairman

30 June 2026

Directors' report

For the year ended 31 December 2025

The Directors present their report together with the audited financial statements of Bezant Resources Plc (the "Company") and its subsidiary undertakings (together, the "Group" or "Bezant") for the year ended 31 December 2025.

The principal activity, review of the business and future development disclosures are contained in the Chairman's Statement on page 4 and the Strategic Report on page 11.

Results and dividends

The Group's results for the year are set out in the financial statements. The Directors do not propose recommending any distribution by way of dividend for the year ended 31 December 2025.

Directors

The following directors have held office during and subsequent to the reporting year:

Colin Bird

Ronnie Siapno

Evan Kirby

Raju Samtani

Edward Slowey

Directors' interests

The beneficial and non-beneficial interests of the current directors and related parties in the Company's shares as at 31 December 2025 and the date of this report are as follows:

31 December 2025 | Date of this report | |||||||

Ordinary shares of 0.002p each | Percentage of issued share capital | Ordinary shares of 0.002p each | Percentage of issued share capital |

| ||||

C. Bird * | 1,083,200,654 | 6.22% | 1,113,969,885 | 4.99% |

| |||

E. Kirby | 65,710,062 | 0.38% | 65,710,062 | 0.29% |

| |||

R. Siapno | 1,333,334 | 0.01% | 1,333,334 | 0.01% |

| |||

R Samtani | 306,164,411 | 1.76% | 336,933,642 | 1.51% |

| |||

E Slowey | 89,625,000 | 0.51% | 89,625,000 | 0.40% |

| |||

* Includes 35,000,000 shares held by Lion Mining Finance Ltd a company controlled by Colin Bird and 55,200,000 shares held by Sylvia Vrska a person closely associated with Colin Bird

Directors' Warrants

The following warrants have been issued to Colin Bird and Raju Samtani.

Colin Bird:

60,000,000 warrants expiring on 18 December 2026 which give the right to subscribe for ordinary shares at a price of 0.06p per share; and

100,000,000 warrants issued on 3 January 2025 expiring on 3 January 2028 which give the right to subscribe for ordinary shares at a price of 0.04p per share.

Raju Samtani:

48,000,000 warrants expiring on 18 December 2026 which give the right to subscribe for ordinary shares at a price of 0.06p per share; and

50,000,000 warrants issued on 3 January 2025 expiring on 3 January 2028 which give the right to subscribe for ordinary shares at a price of 0.04p per share.

Directors' Share Options

The Company on 23 August 2018, 10 November 2020, 15 March 2024 and 3 March 2026 has announced the issue of options over ordinary shares of 0.002p each in the capital of the Company ("Ordinary Shares") pursuant to the Executive Share Option Scheme approved at the Company's Annual General Meeting held on 22 June 2018 ("2018 AGM") (the "Options"). The Options expire on 21 June 2028 being the ten year anniversary of the 2018 AGM. Of the 1.426 million Options which have been awarded as at the date of these accounts, 698 million have awarded to the current directors of the Company as detailed in the table below.

** 50% of the options will vest upon the breaking of ground at the Hope and Gorob mine site and the balance of 50% will vest upon the first sale of concentrate mine from the Hope and Gorob project

Report on directors' remuneration and service contracts

This report has been prepared in accordance with the requirements of Chapter 6 of Part 15 of the Companies Act 2006 and describes how the Board has applied the principles of good governance relating to Directors' remuneration set out in the QCA Corporate Governance Code.

Executive remuneration packages are prudently designed to attract, motivate and retain Directors of the necessary calibre and to reward them for enhancing value to shareholders. The performance measurement of the Executive Directors and key members of senior management and the determination of their annual remuneration packages is undertaken by the Remuneration Committee. The remuneration of Non-Executive Directors is determined by the Board within limits set out in the Articles of Association.

Executive Directors are entitled to accept appointments outside the Company providing the Board's permission is sought.

Aside from the Finance Director whose fees in 2025 were £40,000, the other Directors are entitled to receive between £12,000 and £18,000 per annum as Directors' Fees along with relevant Consulting Fees as applicable, with the aggregate of Salary, Directors' Fees and Consulting Fees detailed in the Directors' Remuneration Summary Table later in this report and in note 22.

Accordingly, given the development of the group's Hope and Gorob project it is likely that compensation packages for Executive Directors will need to move to a level more consistent with the market. Currently, Directors' remuneration is not subject to specific performance targets. The Company is sufficiently small that the Board does not consider that it is necessary to impose such targets as a matter of principle but believes that exceptional performance can be rewarded on an ad hoc basis.

Each Director is also paid all reasonable expenses incurred wholly, necessarily and exclusively in the proper performance of his duties.

The 2018 AGM approved a share option scheme which is to incentivise both Executive, non-Executive Directors, and consultants as well individuals holding positions of responsibility in the Company ("Share Option Scheme") on the following terms: (i) the number of options to be issued shall not exceed 10% of the issued share capital of the Company from time to time; (ii) the exercise price of the options shall be determined by the remuneration committee of the Board of directors of the Company based on the volume weighted average share price of the Company in the 30 days preceding the issue of the options; (iii) the allocation of the options shall be determined by the remuneration committee of the Board of Directors of the Company (iv) the options should vest in accordance with the terms of the Executive Share Option Scheme and (v) the options should be exercised by 21 June 2028. Details of the share options awarded to directors are in the preceding table of Directors' Options.

The 2024 Annual General Meeting approved revisions to the Company's incentive schemes The primary changes relate to the Annual Incentive Schemes so as to more closely align the annual incentive awards with the interest of shareholders which is primarily increases in the Company's share price (the "Revised Incentive Schemes"). The Revised Incentive Schemes put in place new short-term, annual and transaction incentive awards payable in cash and/or Company shares to align the interest of directors, officers, employees and consultants with those of shareholders. These awards are not intended to replace the Company's share option scheme and shall continue until the Board of the Company have put an alternative incentive scheme to the Company's shareholders which the Company's shareholders have approved. No awards have to date been made or proposed under the Revised Incentive Scheme. Eligible participants of the Revised Incentive Schemes are Directors, officers, employees and consultants of the Bezant Resources Plc group ("Eligible Participants"). Eligible Participants, who are good leavers, may continue to be eligible for awards for up to 12 months from their resignation or retirement. The remuneration committee of the Company will make awards to Eligible Participants to reward, retain and recruit Eligible Participants and reward performances against performance measures determined by the remuneration committee. A member of the remuneration committee will not participate in the determining of their own award. The remuneration committee will in determining awards take into account that it is the Company's remuneration policy to, seek where possible, to remunerate and incentivize Eligible Participants on the basis of lower base fees and on the basis that they will also be remunerated by participation in the Company's Incentive Schemes and in the case of non-executive directors be mindful of the potential effect towards objectivity and director independence that may result from significant performance linked awards. The remuneration committee will in making awards determine appropriate key performance indicators for the Eligible Participant to meet ("Award Triggers").

The Revised Incentive Schemes included short term awards to Eligible Participants with direct involvement in meeting short term operational targets for example production, project or exploration targets and annual incentive awards: The annual incentive awards will be awarded to Eligible Participants with a minimum of 80% of their awards being related to Company performance and the balance related to individual key performance indicators determined by the remuneration committee. The foregoing percentages are so as to more closely align the annual incentive awards with the interest of shareholders which is primarily increases in the Company's share price. Eligible Participants annual incentive award based on the Company performance will be based on improvements in the Company's share price in the preceding 12 month period ("Company Share Price Increase"). Following shareholder approval an annual Company Share Price Increase measure was introduced with effect from 30 June 2024. The base share price for the Company Share Price Increase was 0.04826 pence per share for the initial year being the higher of i) the VWAP for June 2024 and ii) the highest calendar monthly VWAP during the 12 months to 30 June 2024 in both cases multiplied by 120% (the "Initial Base Share Price"). In the second and subsequent years the Company Share Price Increase will be "high water marked" by the Base Share Price for the relevant year being the higher of i) the Initial Base Share Price and ii) the highest Year End Share Price (as defined below) for each previous year since the Initial Year multiplied by 120%. The year end share price for each year will be the 30 day VWAP in the last month of the 12 month period (the "Year End Share Price"). The participation rate in the Company Share Price Increase above the Base Share Price for the applicable year will be 5% (the "Participation Rate"). In the year ended 30 June 2025 there was no awards made under the Annual Incentive Awards,

Awards may, at the determination of the Board being mindful of the Company's cash position and working capital requirements, be paid in cash and / or Company shares and if in Company shares based on the 30-day VWAP following announcement of the Company's latest interim or final results prior to the award. Awards of Company shares to Directors and PDMRs in respect of their Annual Incentive Awards may, at the determination of the Board, be subject to a minimum holding period of up to 3 months and will in any 12 month period be in aggregate less than 5% of the issued share capital of the Company.

The Board considers the remuneration of Directors and senior staff and their employment terms and makes recommendations to the Board of Directors on the overall remuneration packages. No Director takes part in any decision directly affecting their own remuneration.

There has been no correspondence to date from shareholders relating to Directors' remuneration matters and therefore no such matters have been considered by the Board in formulating the Company's remuneration policy.

Pensions

The Group does not operate a pension scheme and has not paid any contributions to any pension scheme for Directors or employees.

Directors' remuneration during the year

Remuneration of the Directors for the years ended 31 December 2025 and 2024 was as follows:

2025 | |||||

Directors' Fees |

Salary and Consulting Fees | Totalcash paid year ended | Share based payment - share options | Totalcash and share based | |

£ | £ | £ | £ | £ | |

|

| ||||

C. Bird (note 1) | 12,000 | 48,000 | 60,000 | - | 60,000 |

E. Kirby | 13,665 | - | 13,665 | - | 13,665 |

R. Siapno | 12,000 | - | 12,000 | - | 12,000 |

R. Samtani (note 1) | 40,000 | - | 40,000 | - | 40,000 |

E. Slowey | 18,000 | 14,400 | 32,400 | - | 32,400 |

|

| ||||

Total | 95,665 | 62,400 | 158,065 | - | 158,065 |

Notes:

1. Mr Bird and Mr Samtani's Directors' fees include employee's NIC and UK payroll tax.

2024 | |||||

Directors' Fees |

Salary and Consulting Fees | Totalcash paid year ended | Share based payment - share options | Totalcash and share based | |

£ | £ | £ | £ | £ | |

|

| ||||

C. Bird (note 1) | 12,000 | 48,000 | 60,000 | 9,506 | 69,506 |

E. Kirby | 14,039 | - | 14,039 | 2,377 | 16,416 |

R. Siapno | 12,000 | - | 12,000 | - | 12,000 |

R. Samtani (note 1) | 40,000 | - | 40,000 | 2,971 | 42,971 |

E. Slowey | 18,000 | 15,300 | 33,300 | 5,347 | 38,647 |

|

| ||||

Total | 96,039 | 63,300 | 159,339 | 20,201 | 179,540 |

Notes:

1.Mr Bird and Mr Samtani's Directors' fees include employee's NIC and UK payroll tax.

2. Note 18 to the accounts provides information on Share-based payments.

An amount of £15,000 was paid during 2025 (2024: £15,000) to Lion Mining Finance Limited, a company controlled by C. Bird, for administration services and use of an office.

Environment, Health, Safety and Social Responsibility Policy Statement

The Company adheres to the above Policy, whereby all operations are conducted in a manner that protects the environment, the health and safety of employees, third parties and the entire local communities in general.

The Company is currently principally involved in exploration and development projects, located within, Namibia, Zambia and Botswana having sold its interest in the Eureka project in Argentina during the year and at the year-end had an equity investment in a project in the Philippines via its Blackstone Minerals shareholding.

During the period in Namibia the Company was awarded an Environmental Clearance Certificates (ECC) in relation to Mining Licence 246 in Exploration licence 5796.

During the year, current operations were closely managed in order to maintain our policy aims, with no matters of concern arising. There have been no convictions in relation to breaches of any applicable legislation recorded against the Group during the year.

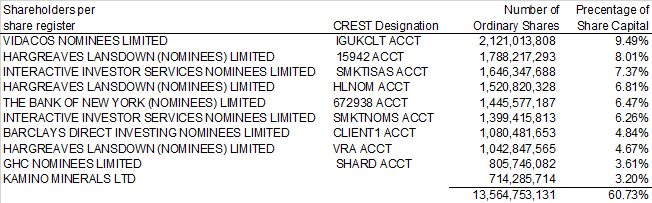

Substantial & Significant Shareholdings

The Company has been notified, in accordance with DTR 5 of the FCA's Disclosure Guidance and Transparency Rules, or is aware, of the following interests in its ordinary shares as at YY June 2026 of those shareholders with a 3% and above equity holding in the Company based on the Company having 22,338,672,557 ordinary shares in issue on 25 June 2026 ("25 June 2026 Shares in Issue").

On 26 June 2025 Breamline Pty Ltd a company controlled by Christian Cordier submitted a TR-1 notification to the Company that it has an indirect interest in 791,406,503 ordinary shares in relation to the following shareholdings of companies which Christian Cordier has an interest in Tonehill Pty Ltd acting for the ("aft") The Tonehill Trust 255,538,825 shares, Coreks Super Pty Ltd aft Coreks Superannuation Fund 151,163,350 shares and Breamline Pty Ltd aft Breamline Ministries 348,704,328 shares. Mr Cordier's interest represented 3.54% at the date of issue of the TR-1 and based on the 25 June 2026 Shares in Issue

On 27 February 2025 the Company announced that Sanderson Capital Partners Ltd had confirmed that they and associates as at that date were interested in 761,469,231 shares which represents 3.41% of the 25 June 2026 Shares in Issue.

Political and charitable contributions

There were no political or charitable contributions made by the Group during the year ended 31 December 2025 (2024: nil).

Information to Shareholders - Website

The Company has its own website (www.bezantresources.com) for the purposes of improving information flow to shareholders, as well as to potential investors.

Statement of Directors' responsibilities

The Directors are responsible for preparing the financial statements in accordance with applicable laws and UK adopted International Accounting Standards. Company law requires the Directors to prepare financial statements for each financial year which give a true and fair view of the state of affairs of the Group and of the Company and of the profit or loss of the Group for that year.

In preparing those financial statements, the Directors are required to:

- select suitable accounting policies and then apply them consistently;

- make judgements and estimates that are reasonable and prudent;

- state whether applicable accounting standards have been followed, subject to any material departures disclosed and explained in the financial statements; and

- prepare the financial statements on a going concern basis, unless it is inappropriate to presume that the Group will continue in business.

The Directors confirm that the financial statements comply with the above requirements.

The Directors are responsible for keeping adequate accounting records which at any time disclose with reasonable accuracy the financial position of the Company (and the Group) and enable them to ensure that the financial statements comply with the Companies Act 2006. The Directors are also responsible for safeguarding the assets of the Company (and the Group) and for taking steps for the prevention and detection of fraud and other irregularities.

In addition, they are responsible for the maintenance and integrity of the corporate and financial information included on the Company's website.

Statement of disclosure to auditor

So far as all the Directors, at the time of approval of their report, are aware:

- there is no relevant audit information of which the Company's auditors are unaware, and

- the Directors have taken all steps that they ought to have taken as Directors in order to make themselves aware of any relevant audit information and to establish that the Company's auditors are aware of that information.

Auditors

UHY Hacker Young have expressed their willingness to continue as the auditors of the Company, and in accordance with section 489 of the Companies Act 2006, a resolution to re-appoint them will be proposed at the Company's forthcoming Annual General Meeting.

Principal risks and uncertainties

The Group has identified the following risks to the ongoing success of the business and has taken various steps to mitigate these, the details of which in relation to its Continuing Operations are as follows:

Risk that mining operations have not yet commenced

The Group's ability to meet any production, timing and cost estimates for its properties cannot be assured. The Group does not currently have any mining operations but during the period was issued a mining licence in relation to the Hope and Gorob copper gold project in Namibia (the "Hope and Gorob Project") and acquired a 90% shareholding in Namib Lead and Zinc Mining (Proprietary) Limited ("NLZM") details of which are set out at note 11.2

which owns an ore processing plant (the "NLZM Processing Plant") to be used for the processing of preconcentrate from the Hope and Gorb mine.

Development and operating risks

Actual cash operating costs, production and economic returns in financial models which the Company uses to plan its activities may differ significantly from those anticipated by studies and estimates. There are a number of uncertainties inherent in the development of any mining project which are relevant to the Hope and Gorob Project. NLZM Processing Plant upgrades and modifications and the development of the Hope and Gorob Project into full mining operations involves a number of risks and hazards associated with mining operations, including mining and industrial accidents, metallurgical and other processing problems, unusual or unexpected geological conditions, equipment failure, labour disputes, environmental hazards, changes in the regulatory environment, and weather and other acts of nature such as earthquakes and floods. These risks may result in: damage to, or destruction of, the Group's properties or production facilities; personal injury or death; environmental damage; delays in mining; increased production costs; asset write downs; monetary losses; and legal liability.

Infrastructure risks

The Hope and Gorob Project is located in a remote area with limited infrastructure. Constructing and operating a mine in such a location will pose logistical challenges, including access to skilled labour, materials and services. The NLZM Plant, is situated in a more accessible area, which mitigates these risks in relation to the NLZM Plant but they still exist. The necessary repairs, modifications and optimisation of the NLZM Processing Plant depends to a significant degree on adequate infrastructure. In the course of developing the Project the Company will need to construct and support the construction of infrastructure, at the Hope and Gorob Project site and the NLZM Processing Plant site which includes but is not limited to water supplies, power, transport and logistics services which affect capital and operating costs. Unusual or infrequent weather phenomena, sabotage, government or other interference in the maintenance or provision of such infrastructure or any failure or unavailability in such infrastructure could materially adversely affect the Company's operations, at the Hope and Gorob Project and at the NLZM Processing Plant.

In future, the Group may experience higher costs and lower revenues than estimated due to unexpected problems

Mining operations can experience unexpected problems during the life of the mine which may result from events of nature, unexpected geological features or mechanical issues that can result in substantial disruption to operations. Such disruption could increase operating costs, delay revenue growth and have implications for the working capital requirements of the business.

Reliance on third parties

The Company is reliant on third party service providers and suppliers to provide equipment, infrastructure and upgrades to the NLZM Processing Plant and the development of the mining operations at the Hope and Gorob site including offering jobs to the locals. Although the Company believes that by acquiring the NLZM Processing Plant these risks are being reduced and that skilled labour will be available in the NLZM Plant location area, there can be no assurance that such parties will be able to provide such services in the time scale and at the cost anticipated by the Company.

Reliance on key personnel and management

The Company's success raising the required capital to finance the refurbishment of the NLZM Processing Plant and the development of the Hope and Gorob Project to create a successful mining operation and thus revenue generation, is substantially dependent on the expertise and continued services of its directors, employees and consultants and the ability of the Company to recruit an in-country management team, The loss of the services of any such persons / inability to recruit personnel could have a material adverse effect on the Company's ability to develop the Hope and Gorob Project. The Company cannot guarantee the retention of its directors, employees and consultants nor that it will be able to continue to attract and retain such employees, and failure to do so could have a material adverse effect on the operations of the Company at the Project.

Requirement for regulatory approvals, permits, permits and government support

The construction and operation of mining projects, production facilities and/or infrastructure will require regulatory approvals, permits and permits to operate, and in some circumstances government financial support. Even with careful planning and verification, it is possible that not all necessary permits or permits for the construction and operation of mining projects, production facilities and/or infrastructure will be obtained. Each of the Company's Projects is also subject to the risk that a particular permit or licence is altered, withdrawn or expires and cannot be extended, which can lead to suspension, delay, or restriction in operations. In addition, relevant authorities may impose conditions on the commencement or duration of the operation of mining projects, production facilities and/or infrastructure. This may delay or restrict the operation of the plants, facilities and/or infrastructure and/or increase the costs of operation. Furthermore, governments over time may change their level of financial support for mining projects, production facilities and/or infrastructure. As a result, these may have a material adverse effect on the Company's profitability and the price of the Ordinary Shares.

Risks relating to health and safety

The physical location, construction, maintenance, and operation of the Projects may pose health and safety risks to those involved or in the vicinity of the Projects. Construction and maintenance of a Project may result in bodily injury, industrial accidents, and even death. If an accident were to occur, the relevant Project could be liable for damages or compensation to the extent such loss is not covered under existing insurance policies. Health and safety concerns and/or accidents could result in the suspension (either temporary or long-term) of operations of a Project which will reduce the revenue of the Company from that Project. Liability for damages or compensation in relation to accidents and/or suspension of operations could have a material adverse effect on the Company's profitability and/or the price of the Ordinary Shares.

Loss of critical processes

The Group's future mining, processing, development and exploration activities depend on the continuous availability of the Group's operational infrastructure, in addition to reliable utilities and water supplies and access to roads.

Any failure or unavailability of operational infrastructure, for example, through equipment failure or disruption, could adversely affect future production output and/or impact exploration and development activities. The group would seek to mitigate this risk by ensuring that access to operational infrastructure is included in any pre mining feasibility studies.

Geological and other risks

Geological risk factors and adverse market conditions could cause actual results to materially deviate from estimated future production and revenue. Failure to achieve production or cost estimates or material increases in costs could have an adverse impact on the future business, cash flows, profitability, results of operations and financial condition. While steps, such as production and mining planning are in place to limit these risks, occurrences of such incidents do exist and should be noted.

Furthermore, the business of mining is subject to a variety of risks such as actual production and costs varying from estimated future production, cash costs and capital costs; revisions to mine plans; risks and hazards associated with mining; natural phenomena; unexpected labour shortages or strikes; delays in permitting and licensing processes; and the timely completion of expansion projects, including land acquisitions required for the expansion of operations from time to time. Geological grade and product value estimations are based on independent resource calculations, studies and historical sales records.

The Group seeks to mitigate these risks in relation to exploration and mine planning activities by using the geological and mining expertise of Board members to oversee and plan exploration and mine planning activities and by engaging the services of reputable external geologists, mine engineering and other experts with appropriate skills and experience to provide exploration and mine planning services for the Group.

Licensing and title risk

Governmental approvals, licences and permits are, as a practical matter, subject to the discretion of the applicable governments or government offices. The Group must generally and specifically in relation to future projects comply with known standards, existing laws and regulations that may entail greater or lesser costs and delays depending on the nature of the activity to be permitted and the interpretation of the laws and regulations by the permitting authorities.

New laws and regulations, amendments to existing laws and regulations, or more stringent enforcement could have a material adverse impact on the Group's result of operations and financial condition. The Group's exploration and mining activities are dependent upon the grant of appropriate licences, concessions, leases, permits and regulatory consents which may be withdrawn or made subject to limitation.

There is a risk that negotiations with the relevant government in relation to the renewal or extension of a licence may not result in the renewal or grant taking effect prior to the expiry of the previous licence and there can be no assurance as to the terms of any extension, renewal or grant. This is a risk that all resource companies are subject to, particularly when their assets are in emerging markets. The Group continually seeks to do everything within its control to ensure that the terms of each licence are met and adhered to.

Economic, political, judicial, administrative, taxation or other regulatory factors

The Group's assets are located in Namibia, Zambia and Botswana and it has an equity investment in a project in the Philippines held via an Australian company and mineral exploration and mining activities may be affected to varying degrees by political stability and government regulations relating to the mining industry.

The Group is exposed to sovereignty risks relating to potential changes of local Governments and possible subsequent changes in jurisdiction concerning the maintenance or renewal of licences and the equity position permitted to be held in the Company's subsidiaries, which the group seeks to mitigate by working with local advisors and / or partners familiar with the local regulatory environment.

Government regulation and political risk related to Namibia

Although Namibia is considered to be stable democracy and the Company's operating activities are subject to laws and regulations governing expropriation of property, health and worker safety, employment standards, waste disposal, protection of the environment, mine development, land and water use, prospecting, mineral production, exports, taxes, labour standards, occupational health standards, toxic wastes, the protection of endangered and protected species and other matters, there are risks relating to changes in mining policy, taxation, ownership requirements or royalties in particular given Namibia has significant dependence on mining for export revenue and thus may adjust its fiscal regime in future.

While the Company believes that the Hope and Gorob Project and the NLZM Processing Plant currently comply with all material current laws and regulations affecting its activities, future changes in applicable laws, regulations, agreements or changes in their enforcement or regulatory interpretation could result in changes in legal requirements or in the terms of existing permits and agreements applicable to the Group, which could have a material adverse impact.

Water, electricity and seasonal weather risks in Namibia

Much of Namibia is arid or semi‑arid and hence water is scarce. Large volumes of waters will be required for the mining operations for open‑pit mining and processing. The remote location of the Hope and Gorob Project means arrangements will need to be made for the water and electricity to be supplied for the mining operation at the Project side and any problems with making such adequate arrangements might delay the commencement of operations. Additionally, the seasonality of weather means that there can be heavy rainfall or seasonal storms that can cause pit flooding, erosion or landslides at open pit mining. Furthermore, rainy season may create flash floods or other conditions which worsen road conditions, which in turn would cause delay with transportation of preconcentrate from the Hope and Goro Project to the NLZM Processing Plant for processing.

Environmental regulation risks in Namibia

Whilst the Company has been awarded the required Environmental Clearance Certificate ("ECC") for its Hope and Gorob Project and NLZM has an ECC which covers the NLZM Processing Plant these are subject to periodic renewals.

In the future environmental and safety legislation (e.g. in relation to reclamation, disposal of waste products, protection of wildlife and otherwise relating to environmental protection) may change in a manner that may require stricter or additional standards than those now in effect, a heightened degree of responsibility for companies and their directors and/or employees and more stringent enforcement of existing laws and regulations. There may also be unforeseen environmental liabilities resulting from either the NLZM Processing Plant optimisation or future mining activities at the Hope and Gorob project site, which may be costly to remedy. If the Company is unable to fully remedy an environmental problem, it may be required to stop or suspend operations at the Project or enter into interim

compliance measures pending completion of the required remedy. The potential exposure may be significant and could have a material adverse effect on the Company. The Company has not purchased insurance for environmental risks (including potential liability for pollution or other hazards as a result of the disposal of waste products occurring from exploration and production) as it is not generally available at a price which the Company regards as reasonably proportionate to the risk.

In Namibia there is not a requirement to post a mine closure rehabilitation bond but it is good practice to provide for this cost in a mine owning company's financial statements and in the NLZM audited accounts for the year ended 31 December 2025 there is an aggregate decommissioning and rehabilitation provision of NAD 5.9M (GBP 264K) for the closure of the NLZM mine. If the NLZM mine is closed and / or if the NLZM mining licence is not renewed then NLZM will be liable to pay mine closure rehabilitation costs the amount of which will depend on the condition of the mine and prevailing environmental and other regulations at the date of closure.

Currency risk

The Group reports its financial results and maintains its accounts in Pounds Sterling, the currency in which the Group primarily operates. The Group's operations in Namibia, Botswana and Argentina and an equity investment in a project in the Philippines held via an Australian company make it subject to foreign currency fluctuations and such fluctuations may materially affect the Group's financial position and results (see note 16). The Group does not have any currency hedges in place and is exposed to foreign currency movements but seeks to mitigate this risk by converting funds from Pounds Sterling to other currencies when making material commitments in other currencies.

Copper-gold price volatility

The Group's operations and any future revenue is significantly affected by changes in realisable copper-gold prices. The price of copper-gold is denominated in US$ and can fluctuate widely and is affected by numerous factors beyond the Group's control, including demand, inflation and expectations with respect to the rate of inflation, the strength of the US$ and of other currencies, interest rates, global or regional political or financial events, and production and cost levels. The Group does not have any commodity price hedges in place as it is not mining and does not produce any copper and its investment in exploration projects are exposed to fluctuations in the prices of underlying commodities.

Competition

The Group competes with numerous other companies and individuals, in the search for and acquisition of exploration and development rights on attractive mineral properties and also in relation to the future marketing and sale of precious metals. There is no assurance that the Group will continue to be able to compete successfully with its competitors in acquiring exploration and development rights on such properties and also in relation to the future marketing and sale of precious metals.

Future funding requirements

As referred to in note 1.1 of these financial statements, the Group made a profit from all operations for the year ended 31 December 2025 after tax of £2,002,000 after a fair value adjustment gain of £2,224,000 (see note 11.1) (2024 - loss of £1,015,000 after a fair value adjustment loss of £157,000 .

The Group had negative cash flows from operations and is currently not generating revenues. Cash and cash equivalents were £430,000 as at 31 December 2025. Post the year end on 31 March 2026 the Company announced a £2,070,000 fundraise and on 11 June 2026 a US$7 million (approx. £5.2 million) secured prepayment facility and offtake agreement with Hartree Metals LLC and that the repayment date for the £700,000 drawdown under the Sanderson Capital Facility Agreement had been extended to 30 September 2027. The Company has post the year end sold the Blackstone Minerals shares held at the year-end for net proceeds of £1.2 million and has been developing the Hope and Gorb mine and modifying and upgrading the NLZM Processing Plant with a target of commencing operations in Q3 2026. Therefore in the year subsequent to the date of these accounts the Company may need to raise funding to provide additional working capital to finance its ongoing activities. Management has successfully raised money in the past, but there is no guarantee that adequate funds will be available when needed in the future.

Impact of War in Ukraine

The Directors are aware of the war in Ukraine and related sanctions and there is no direct impact on the Company as it has no assets or business activities or suppliers with links in Ukraine or Russia and is not aware of any persons sanctioned in relation to the Ukraine conflict owning shares in the Company. An indirect impact of the conflict in Ukraine is the effect that the conflict and sanctions have had on energy and other prices and this and the economic effects of the war in Ukraine may have an effect on the Company's costs. The Company seeks to mitigate this risk by obtaining quotes for and agreeing on material expenditure commitments in advance of engaging services so costs are known in advance but is not in a position to reduce inflation.

Impact of Iran War

The Directors consider as a result of the war in Iran and ongoing middle east conflict and related sanctions there is no immediate impact on the Company as it has no assets or business activities or suppliers with links to Iran and is not aware of any persons sanctioned in relation to Iran owning shares in the Company. The Company is monitoring the position given the uncertainty of the impact of the war in Iran on the supply of oil, gas and other resources from the Middle East and the effect this may have on supply chains, inflation and macro-economic factors.

Going Concern

As disclosed in Note 1.1 to the accounts based on the Board's assessment that the Company will be able to raise additional funds and sell Blackstone Mineral shares held at the year end to meet its working capital and capital expenditure requirements, the Board have concluded that they have a reasonable expectation that the Group can continue in operational existence for the foreseeable future. For these reasons, the Group continues to adopt the going concern basis in preparing the annual report and financial statements.

There is a material uncertainty related to the conditions as disclosed in Note 1.1 that may cast significant doubt on the Group's ability to continue as a going concern and therefore the Group may be unable to realise its assets and discharge its liabilities in the normal course of business.

The financial report does not include any adjustments relating to the recoverability and classification of recorded asset amounts or liabilities that might be necessary should the entity not continue as a going concern.

Post Balance Sheet events

Subsequent events are disclosed in note 28 to the Accounts and summarised below:

On 11 March 2027 the Company announced the signing of an exclusive mining and logistics services agreement between the companies 70% owned Namibian subsidiary Hope and Gorob Mining Pty Limited and Unitrans Namibia Pty Limited; services to be provided include drilling, blasting and secondary breaking of ore and waste, loading and hauling, road maintenance, short-term mine planning for the Hope and Gorob mine site and material handling at the NLZM Processing Plant. These services will form a substantial part of the Hope and Gorob project operating costs.

On 24 March 2026 the Company announced the purchase by the group from MKH Tangible Investments CC of an additional 20% shareholding in Hope and Gorob Mining Pty Limited it's 70% owned Namibian registered subsidiary the holder of the Hope and Gorob Project and the settlement of any remaining obligations due to MKH Tangible Investments CC under the original 2018 agreement between MKH Tangible Investments CC and the previous owner of the Hope and Gorob Project for £1,114,000 of which £557,000 was settled in cash and £557,000 by the issue of shares in the Company.

On 31 March 2026 the Company announced a fundraising of £2,070,000 at 0.065 pence per Ordinary Share ( the "Fundraising Price") and the issue of shares to settle accrued fees of £7,166 at the Fundraising Price.

On 11 June 2026 the Company announced a US$7 million (approx. £5.2 million) secured prepayment facility and offtake agreement with Hartree Metals LLC and that the repayment date for the £700,000 drawdown under the Sanderson Capital Facility Agreement had been extended to 30 September 2027.

Post the year end through to 19 June 2025 the Company has announced the exercise of 1,201,115,385 warrants which have been exercised for in aggregate £723K - note 28 to the Accounts.

Relations with Shareholders

The Company plan to hold an Annual General Meeting in late July or August 2026 and the wording of each resolution to be tabled will be set out in a formal Notice of Annual General Meeting to be sent to shareholders.

Shareholders who are unable to attend the Annual General Meeting and who wish to appoint a proxy in their place must ensure that their proxy is appointed in accordance with the provisions set out in the Notice of Annual General Meeting.

On behalf of the Board

Mr Colin Bird

Executive Chairman

30 June 2026

Corporate GovernanceFor the year ended 31 December 2025

________________________________________________________________________

As an AIM-traded company, Bezant Resources PLC ("Bezant" or the "Company") and its subsidiaries are required to apply a recognised corporate governance code and demonstrate how the Group complies with such corporate governance code and where it departs from it.

The Directors of the Company have formally taken the decision to adopt the QCA Corporate Governance Code (2023) (the "QCA Code"). The Board recognises the principles of the QCA Code, which focus on the creation of medium to long-term value for shareholders without stifling the entrepreneurial spirit in which small to medium sized companies, such as Bezant, have been created. The Company is committed to providing annual updates on its compliance with the QCA Code further details of which are set out below.

QCA Corporate Governance Statement

The Company is committed to good corporate governance and has adopted the corporate governance guidelines of the Quoted Companies Alliance (QCA).

Principle 1: Establish a purpose, strategy and business model which promotes long-term value for shareholders

The Group's strategy is to build a diversified portfolio of high-potential mineral assets across southern Africa by advancing exploration and development projects with a focus on copper and gold assets, with the aim of creating long-term value through resource discovery, licensing optimisation, and project advancement toward commercial production.

We plan to achieve this through:

• Expertise and Experience