1st May 2026 07:00

1 May 2026

Aterian plc("Aterian" or the "Company" or the "Group")

Final Results for the Year Ended 31 December 2025

Aterian Plc (LSE: ATN) is pleased to announce its audited results for the period ended 31 December 2025.

This announcement contains information which, prior to its disclosure, was inside information as stipulated under Regulation 11 of the Market Abuse (Amendment) (EU Exit) Regulations 2019/310 (as amended).

Engage directly with the Aterian PLC management team by asking questions, watching video summaries, and seeing what other shareholders have to say. Please navigate to our interactive investor hub here: https://aterianplc.com/s/fcf8eb

For further information, please visit the Company's website: www.aterianplc.com or contact:

Aterian Plc:

Charles Bray, Executive Chairman - [email protected]

Simon Rollason, CEO & Director - [email protected]

Financial Adviser and Joint Broker:

AlbR Capital Limited

David Coffman / Dan Harris

Tel: +44 (0)207 7469 0930

Joint Broker:

SP Angel Corporate Finance LLP

Ewan Leggat / Devik Mehta

Tel: +44 20 3470 0470

Financial PR:

Bald Voodoo - [email protected]

Ben KilbeyTel: +44 (0)7811 209 344

Subscribe to our news alert service: https://atn-l.investorhub.com/auth/signup

STRATEGIC REPORT

YEAR ENDED 31 DECEMBER 2025

Dear Shareholder,

2025 was a year of continued progress for Aterian as the Company advanced its exploration portfolio across Africa while strengthening its position within the critical minerals sector despite challenging capital market conditions.

During the year, we expanded and refined our project pipeline across Botswana, Rwanda and Morocco, focusing on commodities essential to the global energy transition, including copper, lithium and tantalum.

In parallel, we began establishing the foundations of a mineral trading platform in Rwanda through our subsidiary Eastinco Limited, creating an additional pathway to generate revenue and support the development of a scalable trading business.

In Botswana, we expanded our exploration portfolio through our 90%-owned subsidiary Atlantis Metals, which now holds eleven licences across the highly prospective Kalahari Copperbelt, together with three lithium brine licences in the Makgadikgadi Pans. Work during the year focused on geological interpretation and target generation, positioning the portfolio for future exploration programmes.

In Rwanda, exploration at the HCK lithium-tantalum project progressed through our joint venture with Rio Tinto, which funded a comprehensive exploration programme including diamond drilling, geochemical sampling and geophysical surveys. Rio Tinto concluded its earn-in programme in October 2025, having invested approximately US$4.7 million in exploration activities. The programme generated a substantial geological dataset and confirmed the presence of spodumene-bearing pegmatites, significantly enhancing the Company's understanding of the project.

Alongside exploration activities, we made important progress in developing our mineral trading business in Rwanda. Following the introduction of the country's mineral traceability system, Eastinco resumed trading operations and began establishing supply relationships with artisanal and small-scale mining producers, laying the groundwork for a scalable trading platform.

Morocco remains a core component of the Company's exploration strategy and represents a significant copper exploration portfolio. During the year, exploration programmes continued across the Company's key projects at Agdz, Tata, Azrar and Jebilet Est. This work confirmed copper and silver mineralisation across several prospects, with encouraging results supporting the potential for further discoveries across our licence portfolio.

In December 2025, the Company entered into a strategic AI-powered exploration joint venture with Lithosquare, designed to accelerate target generation and exploration across Aterian's project portfolio. Lithosquare is a next-generation mineral exploration company that combines artificial intelligence, advanced data science, and geological expertise. The agreement provides a capital-efficient mechanism to accelerate target generation and exploration across Aterian's portfolio.

These developments reflect Aterian's strategy of building a diversified portfolio of critical metal projects in mining-friendly African jurisdictions while developing complementary trading activities to support long-term value creation.

Demand for critical minerals such as copper, lithium and tantalum continues to strengthen as the global energy transition accelerates. Aterian remains focused on responsibly advancing its projects while contributing to secure and sustainable supply chains for these essential metals.

Rwanda Exploration and Mineral Trading

Rwanda is emerging as an attractive mining jurisdiction, offering significant mineral resources, a stable political environment and supportive investment policies. The country hosts notable deposits of tin, tantalum and tungsten (3Ts), as well as lithium, niobium and rare-earth elements, which are important components of global supply chains for technology, energy storage and electronics. Through its focus on responsible mining and transparent supply chains, Rwanda is positioning itself as an important supplier of critical minerals required for the global energy transition and technological development.

Activities during the year focused on exploration at the HCK lithium-tantalum project and the development of the Company's mineral trading platform.

At the HCK Project, exploration was undertaken in partnership with Rio Tinto under the earn-in joint venture as announced in 2023. The programme included diamond drilling and extensive geochemical and geophysical work, confirming the presence of spodumene-bearing pegmatites and demonstrated lithium prospectivity across the licence area. Following the completion of the exploration programme, Rio Tinto elected to exit the joint venture in October 2025, having invested approximately US$4.7 million in the project. Control of the project and the associated technical data have therefore reverted to Aterian.

In parallel, the Company continued to develop its mineral trading activities through Eastinco Limited. Trading operations resumed following the introduction of Rwanda's Inkomane mineral traceability system, and the business began establishing supply relationships with artisanal and small-scale mining producers.

Overall, activities in Rwanda during 2025 strengthened the Company's understanding of the HCK project while laying the foundations for the development of a scalable mineral trading business in the country.

Morocco Exploration

Morocco is emerging as an attractive mining jurisdiction, supported by a stable political environment, well-established infrastructure and a supportive regulatory framework for mineral exploration and investment. The country hosts a diverse range of mineral resources, including copper, silver, cobalt, manganese and other critical metals important to global industrial and energy transition supply chains. With a long history of mining and strong government support for resource development, Morocco is positioning itself as an important supplier of minerals essential to modern technologies and the global energy transition.

During 2025, the Company continued to advance its Moroccan exploration portfolio, which remains a core part of Aterian's critical metals strategy. The Company holds 44 exploration licences covering approximately 663 km² in the prospective Anti-Atlas region, targeting copper and silver mineralisation.

Exploration activities focused on the Company's priority projects at Agdz, Tata, Azrar and Jebilet Est. Work programmes included geological mapping, geophysical interpretation, surface sampling and reconnaissance drilling. At Agdz, drilling and trenching confirmed copper-silver mineralisation associated with structurally controlled systems, while exploration at Agdz Est identified additional mineralised fault zones, highlighting the potential for a broader district-scale system.

Across the wider Moroccan portfolio, exploration continued to define new targets and refine existing prospects through geological studies and the integration of data into the Company's AI-assisted exploration collaboration with Lithosquare. Overall, the results generated during the year strengthened the prospectivity of the Moroccan portfolio and support the Company's strategy of building a pipeline of critical metal exploration projects in mining-friendly jurisdictions.

Botswana Exploration

Botswana is emerging as an attractive destination for battery metals exploration, supported by a stable political environment, investor-friendly policies and significant mineral potential. Historically known for its diamond industry, the country is increasingly diversifying into critical minerals such as lithium, nickel, copper and manganese, which are essential for the global transition to electric vehicles and renewable energy storage.

In 2025, the Company continued to advance its Botswana portfolio following the 2024 acquisition of a 90% interest in Atlantis Metals. The portfolio comprises 14 prospecting licences covering approximately 5,211.51 km², including eleven licences in the highly prospective Kalahari Copperbelt and three lithium brine licences in the Makgadikgadi Pans.

Work during the year focused on geological evaluation and target generation across the Kalahari Copperbelt licences. The Company commissioned the reprocessing of regional airborne geophysical datasets and undertook desktop geological studies to improve the understanding of structural and stratigraphic controls on copper mineralisation. This work enabled the identification and prioritisation of several exploration targets across the licence portfolio.

At the Sua Pan lithium brine licences, a groundwater reconnaissance and sampling programme was completed to establish baseline hydrogeochemical conditions and assess lithium potential. While lithium concentrations were generally low, the programme provided valuable baseline data to inform future exploration.

Overall, activities in Botswana during the year focused on building the geological understanding of the licence portfolio and identifying priority targets for future exploration.

Financial Review

During the period under review, the Group made a loss before taxation of £2,016,000 (2024: loss £1,617,000).

The loss primarily reflects exploration expenditure across the Company's project portfolio together with corporate and administrative costs associated with advancing its operations.

Strategy

Aterian Plc is a critical metals exploration and development company focused on unlocking Africa's mineral potential. The Company's objective is to build an integrated platform spanning exploration, development and mineral trading, supporting the supply of metals essential to the global energy transition. Aterian remains committed to identifying and advancing strategic opportunities that align with this objective while contributing to the secure and responsible development of critical mineral supply chains.

Strategic Plan

Aterian's strategy focuses on building a diversified portfolio of critical mineral assets across mining-friendly African jurisdictions while developing complementary trading activities to support long-term revenue generation and shareholder value.

The key elements of the Company's strategy are:

Exploration and Asset Development

| Advancing a diversified portfolio of critical mineral projects through systematic exploration programmes designed to de-risk assets and identify opportunities for resource development. |

Strategic Partnerships and Joint Ventures

| Partnering with established industry participants to accelerate exploration, share risk and unlock value across the Company's project portfolio. |

Geographic and Commodity Diversification

| Maintaining a diversified portfolio across multiple African jurisdictions and critical metals to manage exploration risk and capture emerging opportunities in the energy transition supply chain. |

Responsible and Sustainable Practices

| Promoting responsible exploration and transparent supply chains while supporting local communities and adhering to international ESG standards. |

Targeted Mergers and Acquisitions | Pursuing selective acquisitions of prospective critical metal assets to expand the Company's exploration pipeline and enhance portfolio value. |

Integrated Business Model

| Developing an integrated business model combining exploration, project development and mineral trading to diversify revenue streams and support long-term growth. |

Through this strategy, Aterian aims to build a scalable critical minerals business that contributes to the supply of metals required for the global energy transition while maintaining responsible and sustainable operations.

Group Overview

Operational Statement, 2025

Introduction

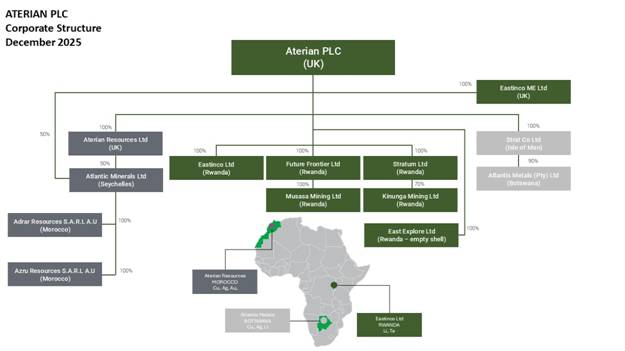

Aterian Plc is a critical metals exploration and development company focused on Africa, with projects in Morocco, Rwanda and Botswana. The Company targets commodities central to the energy transition, including copper, lithium, tantalum, niobium and tin, and is building a portfolio of prospective assets alongside mineral trading activities.

In Rwanda, the Company operates through several subsidiaries. Eastinco Limited holds a mineral trading licence and is actively purchasing concentrate from artisanal and small-scale miners (ASMs) for export in partnership with Wogen Resources, the Company's sales and marketing partner. Two additional subsidiaries, Kinunga Mining Limited and Musasa Mining Limited, hold exploration licences targeting tantalum-niobium (coltan) and lithium. In Morocco, Aterian operates through two subsidiaries holding exploration permits focused on developing copper and silver resources.

In April 2024, the Company acquired a 90% interest in Atlantis Minerals Pty Ltd in Botswana, initially comprising four copper-silver and lithium licences. This portfolio has since expanded to eleven licences in the Kalahari Copper Belt, and three licences adjacent to Sua Pan considered prospective for lithium-bearing brines.

Project Exploration Review - Rwanda

At year-end, the Company had two exploration projects in Rwanda.

1. The HCK Lithium-Tantalum Project, located in southern Rwanda.

2. The Musasa Lithium-Tantalum Project, located in the Western Province on the eastern shores of Lake Kivu.

HCK Lithium-Tantalum Project

The HCK Lithium-Tantalum Project covers approximately 2,750 hectares in southern Rwanda and is held by Kinunga Mining Ltd, a Rwanda-registered joint venture company owned 70% by Stratum Limited (a wholly owned subsidiary of Aterian) and 30% by HCK Mining Company Ltd.

In May 2023, Aterian entered into an Earn-In Investment and Joint Venture Agreement with Rio Tinto Mining and Exploration Ltd and Kinunga Mining Ltd. Rio Tinto exited the agreement in October 2025 after investing US$4.73 million in exploration activities, concluding that the project was unlikely to host a Tier-1 scale lithium deposit.

Exploration activities under the joint venture included diamond drilling, geochemical sampling and geophysical surveys. In early 2025, diamond drilling resumed at the HCK-1 prospect, targeting lithium-bearing pegmatites. Four diamond drill holes, totalling approximately 1,180 m, were completed across two targets (HCK-1 and HCK-2), intersecting multiple pegmatite dykes, with downhole thicknesses locally reaching up to 79 m.

Assay results confirmed the presence of spodumene-bearing pegmatites, including a notable intersection in hole MWOG0002 of 6.90 m at 2.11% Li₂O, including 3.45 m at 3.20% Li₂O within fresh pegmatite below the weathered zone. These results validated the pegmatite exploration model developed from earlier geological mapping, geochemical sampling and geophysical surveys.

The exploration programme also included the collection of 257 rock samples, 2,643 soil samples, and approximately 246 km of ground magnetic surveys, together with radiometric data and mineralogical test work. Following Rio Tinto's exit, control of the project and the full technical dataset reverted to Aterian.

Aterian intends to review the accumulated data and advance exploration at HCK with a renewed focus on lithium, tantalum and niobium mineralisation, which occur within the licence area and have historically supported artisanal mining

Musasa Lithium-Tantalum Project

The Musasa Lithium-Tantalum Project comprises an exploration licence covering approximately 350 hectares in Rwanda's Western Province and is held by Musasa Mining Limited, a wholly owned subsidiary of Aterian.

Since the licence was granted in October 2024, the Company has undertaken initial target generation work, including desktop studies and reconnaissance field surveys. A total of 66 observation points were established across the licence area, with evidence of current or historic artisanal mining identified at eight locations.

Pegmatites were recorded at 23 locations, and beryl was identified at one site. Indicators consistent with potential subsurface pegmatite mineralisation, including coarse muscovite and quartz fragments in soil, were observed at a further 20 locations.

The presence of pegmatites, indicator minerals and historic artisanal workings is considered encouraging and suggests the potential for the discovery of a new pegmatite field within the licence area.

Eastinco Limited - Mineral Trading

Eastinco Limited, a wholly owned subsidiary of Aterian, holds a mineral trading licence in Rwanda and operates the Company's mineral trading platform.

Trading operations resumed in February 2025 following the stabilisation of Rwanda's Inkomane mineral traceability and trading system. Eastinco registered as a compliant participant and conducts trading activities in accordance with Rwanda Mines, Petroleum and Gas Board ("RMB") requirements and international responsible sourcing frameworks, including the Responsible Minerals Initiative (RMI) and OECD Due Diligence Guidance.

Supply agreements have been established with vetted artisanal and small-scale mining suppliers, supported by internal quality control procedures including pXRF verification, laboratory assays and supervised blending and packaging prior to export. To support concentrate procurement, Aterian secured a US$250,000 mezzanine loan facility, alongside a trade finance agreement providing up to US$4.5 million to fund purchases of tantalum, niobium and cassiterite concentrates.

Trading activities generated a gross profit during Q4 2025, demonstrating the viability of the Company's trading model.

In 2026, Aterian further strengthened its trading operations through a profit-share joint venture with Wogen Resources, a leading international metals trader. The agreement provides access to up to US$25 million in working capital to support supplier payments, inventory financing, and full-cycle trade funding.

Additional funding of £450,000 has been raised through equity and convertible bonds to expand trading infrastructure in Rwanda, including larger premises and increased throughput capacity.

Aterian is also developing partnerships with selected artisanal mining producers, providing equipment, capital and technical support to improve production and processing. These initiatives are intended to increase short-term production by processing tailings while supporting longer-term growth.

Overall, the Rwanda trading platform has progressed from operational restart to a scalable trading business capable of generating revenue while maintaining strong ESG and traceability standards.

Project Exploration Review - Morocco

The Company holds 663 km² of exploration licences in Morocco, targeting critical minerals with a primary focus on copper and silver. The licences are held 100% by the Company's Moroccan subsidiaries, with Elemental Altus Royalty Corporation holding a 2.5% NSR royalty over each licence, except for Akka and West Tazalaght, where no royalty applies.

Most licences are located in the Anti-Atlas region, a historically significant copper-producing district hosting numerous copper occurrences associated with Neoproterozoic volcano-sedimentary sequences and sediment-hosted systems, including units of the Adoudou Formation and Cambrian carbonates.

Exploration efforts are focused on the Company's most prospective assets, including Agdz, Tata, Azrar and Jebilet Est, while maintaining flexibility to pursue additional opportunities across the Moroccan portfolio.

A summary of the key projects is provided below.

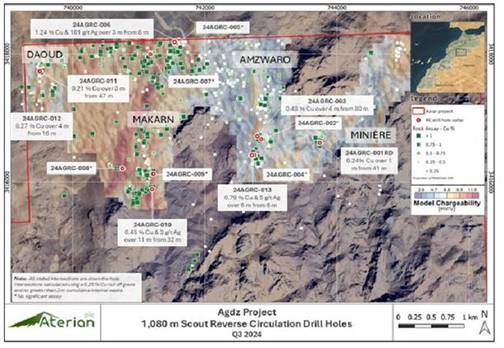

Agdz Copper-Silver Project

The Agdz Copper-Silver Project covers 50.4 km² in central Morocco and comprises the Agdz Est licence (15.9 km²) and the Agdz licence (34.5 km²). The project lies approximately 35 km east of Ouarzazate, within the Anti-Atlas belt, near the Bouskour copper-silver mine and the Imiter silver mine, both operated by Managem.

Mineralisation occurs within volcano-sedimentary rocks of the Ouarzazate Supergroup intruded by granodiorite and cut by fault systems associated with hydrothermal alteration and historical workings. Exploration has defined five main prospects (Makarn, Makarn North, Amzwaro, Minière and Daoud), with rock chip samples returning grades of up to 26.5% Cu, 448 g/t Ag and 3.74 g/t Au.

Work completed to date includes 576 m of trenching across 13 trenches and a reverse circulation drilling programme in 2024 comprising 13 holes for 1,080 m. Significant drill intersections include 3 m at 1.24% Cu and 101 g/t Ag at Makarn North and 6 m at 0.79% Cu and 5 g/t Ag at Amzwaro.

Recent exploration at Agdz Est identified several mineralised fault zones with four sub-parallel structures mapped over strike lengths of up to 0.9 km, returning grades of up to 2.97% Cu and 51 g/t Ag.

Data generated from recent work will be incorporated into the Company's AI-enabled exploration partnership with Lithosquare to assist with project ranking and target generation.

|

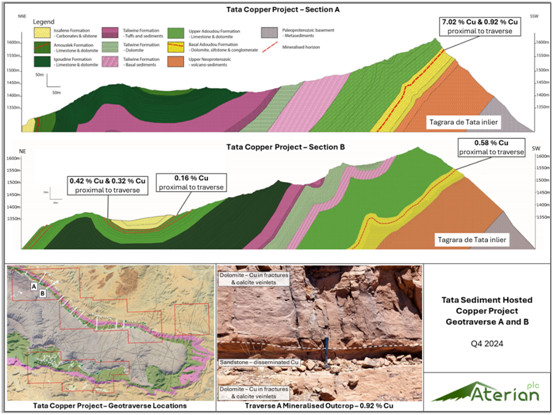

Tata Copper Project

The Tata Copper Project covers 138.6 km² in the western Anti-Atlas Mountains, approximately 165 km southeast of Agadir and 50 km from the Tizert copper mine operated by Managem.

Exploration targets sediment-hosted copper mineralisation within the Adoudou Formation, with mineralisation identified along approximately 32 km of strike, of which around 13 km remains untested. Rock chip sampling has returned values of up to 7.02% Cu from bedding-parallel mineralisation within lower Adoudou siltstones.

Recent work has focused on the reinterpretation of historical airborne geophysical datasets (magnetometry, gamma-spectrometry and electromagnetic surveys) covering over 250 km². Integration of these datasets with geological and geochemical information has identified four priority copper targets with a combined strike length of approximately 14.3 km.

Further geological mapping, sampling and ground geophysical surveys are planned to refine targets for drilling.

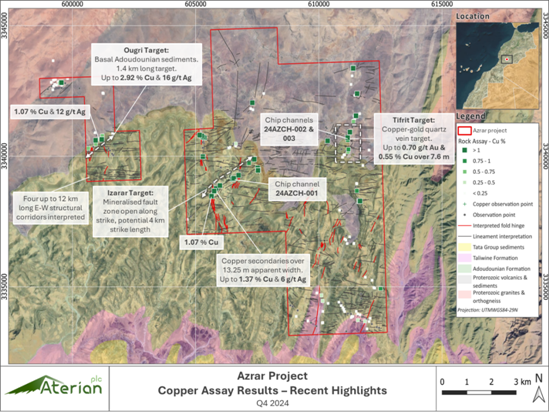

Azrar Copper-Gold Project

The Azrar Copper-Gold Project covers 76.9 km² in the western Anti-Atlas, approximately 155 km southeast of Agadir and 45 km from the Tizert copper mine.

Recent fieldwork included 8 line-km of geological mapping and reconnaissance channel sampling. Results include 0.80% Cu over 4.2 m at the Izarzar fault target and 0.82 g/t Au with 0.63% Cu over 9 m at the Tifrit quartz vein target, including 2.97 g/t Au and 2.00% Cu over 0.7 m.

Three principal targets have been identified:

· Tifrit - a 3.8 km quartz vein system hosting copper-gold mineralisation

· Ougri - a 1.4 km sediment-hosted copper zone returning up to 2.92% Cu and 16 g/t Ag

· Izarzar - a 4 km structurally controlled copper-silver system with sampling up to 2.45% Cu

Reinterpretation of airborne geophysical data has identified five priority exploration targets covering approximately 11.4 km². Further mapping, trenching and geophysics are planned.

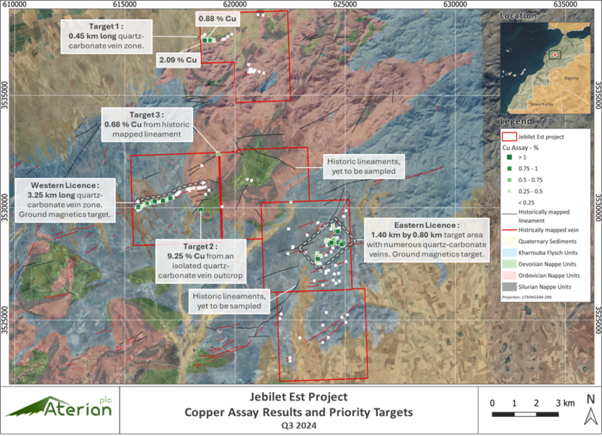

Jebilet Est Copper Project

The Jebilet Est Copper Project covers 73.6 km² and is located approximately 35 km northeast of Marrakech, with good infrastructure including rail access to the port of Casablanca.

Exploration has focused on mapping quartz and quartz-carbonate veins and verifying structural lineaments. A previously mapped vein system has been extended to approximately 3.25 km, with additional sub-parallel veins identified.

Rock chip sampling returned values including 2.09% Cu, 9.25% Cu, and 0.68% Cu from several newly identified targets.

Earlier work defined two principal mineralised zones, with grades of up to 4.43% Cu in the western licence and 3.11% Cu in the eastern licence. These results indicate multiple structurally controlled copper-bearing systems across the project area.

Other Explored Moroccan Projects

Akka Copper Project

The Akka Project comprises three licences covering 47.1 km² in the western Anti-Atlas and was awarded in August 2023. The project is located approximately 15 km west of Akka and targets copper mineralisation hosted within Adoudou Formation sediments.

The project lies within an established copper district approximately 20 km east of the Akka Copper-Gold Mine and 35 km southwest of the Tazalaght Copper Mine.

Initial reconnaissance sampling returned values up to 3.93% Cu from quartz-carbonate veining within a fold hinge structure. Additional samples returned 0.30% Cu and 0.34% Cu, while disseminated copper oxide mineralisation within Adoudou dolomites returned anomalous values of 0.16% Cu.

West Tazalaght Copper Project

The West Tazalaght Project comprises two licences covering 27.4 km² in the western Anti-Atlas and was awarded in August 2023.

The project is located approximately 13 km northeast of Tafraoute and 7 km west of the Tazalaght Copper Mine. Exploration targets sediment-hosted copper mineralisation within folded sediments of the Adoudou and Taliwine Formations.

Initial reconnaissance sampling returned values of up to 0.25% Cu, and evidence of historical copper activity, including smelter slag containing malachite, was observed within the licence area.

Morocco Portfolio Review and Licence Relinquishments

This year, the Company conducted a comprehensive review of its Moroccan asset portfolio to streamline operations and focus on core projects. As a result, several non-core research permits due for renewal were relinquished. The asset review considered factors such as geological prospectivity, initial reconnaissance mapping and sampling, project size, accessibility, and infrastructure.

This strategic decision has reduced the Company's landholding from 897.7 km2 to 663.6 km2, enabling a more targeted allocation of capital and resources. The refined portfolio allows for greater focus on high-priority assets, including Agdz, Azrar, Tata, and Jebilet Est, while also creating flexibility to pursue new opportunities within Morocco.

Project Exploration Review - Botswana

In April 2024, the Company completed the acquisition of a 90% interest in Atlantis Metals (Pty) Ltd, a privately owned company registered in Botswana. Atlantis holds 14 prospecting licences comprising eleven copper-silver licences in the Kalahari Copperbelt (KCB) and three lithium brine licences in the Makgadikgadi Pans, covering a combined area of 5,211.51 km².

Kalahari Copperbelt

The Kalahari Copperbelt (KCB) is considered one of the most prospective regions globally for sediment-hosted copper deposits (USGS, 2020). The belt extends approximately 1,000 km from western Namibia into northern Botswana along the margin of the Kalahari Craton and hosts several significant copper-silver deposits.

Mineralisation in the Kalahari Copperbelt typically occurs near the contact between the D'Kar Formation and the underlying Ngwako Pan Formation, which hosts several known copper-silver deposits.

Atlantis licences are strategically located within this emerging copper district. One licence lies approximately 50 km east of MMG's Khoemacau Copper Mine Zone 5 deposit (92.9 Mt at 2.0% Cu and 21 g/t Ag), while another is located 7 km west of the Banana Zone deposit (157 Mt at 0.86% Cu and 11 g/t Ag). In March 2024, MMG Limited acquired Khoemacau's parent company, Cuprous Capital Ltd, for US$1.73 billion.

The Company engaged independent geophysical consultants to reprocess airborne geophysical datasets from the Botswana Geoscience Institute and other sources. This work improved geological interpretation and assisted in mapping the key D'Kar-Ngwako Pan contact, an important exploration horizon for copper-silver mineralisation.

Desktop studies indicate that the Atlantis licences lie within a highly prospective metallogenic province that hosts deposits such as Motheo, Khoemacau and Boseto, although the level of prospectivity varies depending on structural setting and stratigraphy.

Several licences are considered structurally favourable, particularly PL0154/2024, PL0157/2024, PL2622/2023, PL0199/2025 and PL0265/2025, where basin-margin structures, fold geometries and interpreted D'Kar stratigraphy may provide favourable conditions for copper mineralisation.

Satellite-based remote sensing using Sentinel-2 imagery identified spectral signatures associated with minerals such as bornite, chert, goethite and illite, together with anomalous CO₂ and helium emissions, which may indicate concealed copper-silver mineralisation beneath soil or deep cover.

These interpretations have been reviewed and supported by Lithosquare, the AI exploration partner collaborating with Aterian, and have enabled a portfolio-wide desktop target ranking exercise to prioritise follow-up exploration.

Sua Pan Lithium

The Company holds three prospecting licences covering 2,517 km² along the eastern and southern margins of Sua Pan within the Makgadikgadi Salt Pans.

The Makgadikgadi Pans were designated a government "Lithium Zone" in 2022 to encourage exploration following historical reports of lithium-bearing brines and the emergence of Direct Lithium Extraction (DLE) technologies that may improve the economic viability of such deposits.

Historical sampling during the 1980s reported lithium concentrations of 103, 117 and 223 mg/L, although the precise sampling locations were not recorded.

In December 2025, the Company commissioned Aqualogic (Pty) Ltd to conduct a Groundwater Reconnaissance and Sampling Programme across the licence areas to establish baseline hydrogeochemical conditions and assess lithium potential.

The programme collected 15 water samples from six boreholes and nine shallow auger holes within the salt pan sediments. Field measurements included pH, temperature, electrical conductivity and total dissolved solids, with laboratory analysis conducted by Gaborone Laboratory Services, supported by an ISO/IEC 17025 accredited laboratory in South Africa for trace element analysis.

Results show that the groundwater system is highly saline, with total dissolved solids ranging from 2,233 mg/L to 106,400 mg/L. Hydrochemical classification indicates predominantly Na-Cl type waters within the pan sediments and Na-Ca-Cl type waters in boreholes, consistent with evaporative concentration processes typical of salt pan environments.

However, lithium concentrations were extremely low or below detection limits, with similarly low levels of bromide and boron. While the reconnaissance results indicate limited lithium enrichment in the sampled groundwater, the study provides important baseline hydrogeochemical data for future exploration across the project area.

Lithosquare Partnership

In December 2025, the Company entered into a strategic AI-powered exploration joint venture with Lithosquare, a next-generation mineral exploration company that combines artificial intelligence, advanced data science, and geological expertise. The agreement provides a capital-efficient mechanism to accelerate target generation and exploration across Aterian's portfolio.

The Key Highlights of the JV:

· Up to €1.4 million fully funded AI-led programme directed across eight priority Aterian projects ("JV Projects")

· Potential for Lithosquare to earn a 2.0% net smelter return (NSR) and up to 49.9% equity, strictly tied to exploration success and value creation

· Initial €500,000 investment for AI-driven target generation, geophysics, mapping and scout drilling to identify high-value copper and critical mineral targets rapidly

· €900,000 additional projected drilling to advance successful targets

· Lithosquare has an initial 20% project interest and 0.5% ("NSR") with additional equity and NSR interests tied to value creation catalysts

This capital-efficient structure enables Aterian to accelerate value creation on its portfolio with zero dilution. The JV partners are aligned on rapid execution and value creation, with work in progress.

The Business Model

The Company's strategy is to build a scalable critical metals business through phased exploration in mining-friendly, investment-attractive jurisdictions. Aterian aims to grow its asset portfolio by identifying and acquiring high-potential greenfield opportunities through mergers and acquisitions.

Strategic partnerships form an important part of this approach, enabling the Company to accelerate exploration and advance projects toward potential development. Key milestones achieved to date include the acquisition of the Company's Moroccan exploration portfolio, the earn-in joint venture with Rio Tinto in Rwanda, and the acquisition of Atlantis Metals in Botswana.

The Company remains committed to executing this strategy while maintaining strong corporate governance based on the QCA Code.

Resources and Reserves

Given the early-stage nature of the projects held by the Company, with current exploration efforts focused on planning future drilling programmes, the Company has no stated resources or reserves.

Environment, Social and Governance Policy

Our Communities

Integrating ESG matters into our operations and investment decision-making processes is a key element of being a responsible corporate body. We firmly believe it is part of our corporate responsibility to deliver returns by being a responsible investor.

Minimising our impact on the environment is a strong company focus. This includes reducing our carbon footprint and water usage, reforestation and protecting biodiversity.

Aterian is committed to being a responsible corporate citizen and operating in a manner that is transparent and environmentally responsible, ensuring the longevity of our operations and supporting the socio-economic development of our host communities.

Responsible mining and exploration are about being transparent and open. At Aterian, we are committed to the safety of our people, the protection of the environment, and continuous improvement through technological innovation. This is made possible thanks to the dedication of our employees, as well as the support of our leadership and the communities in which we operate.

At Aterian, we recognise the importance of the UN Sustainable Development Goals (UN SDGs), and we indirectly contribute to many of them in some way.

We have prioritised the SDGs that align most directly with our business, corporate strategy, sustainability efforts, and stakeholder expectations while also representing our greatest opportunities to contribute further to the goals.

Aterian's commitment to being a responsible corporate citizen is guided by our ESG policies.

Our Commitment to the Growing Importance of ESG in the Mining Environment

ESG factors are likely to be the main source of risk in metal and mineral supply over the coming decades, more so than direct reserve depletion. Following OECD and EU guidelines on responsible sourcing of minerals is essential in preventing groups in surrounding regions from profiting from the trade of Conflict Minerals-namely tin, tantalum, tungsten, and gold. These guidelines establish a due diligence framework for companies to identify, assess, and mitigate risks in their supply chains, ensuring transparency and ethical sourcing practices. By adhering to these standards, companies and regulators help break the link between mineral extraction and the financing of violence, human rights abuses, and political instability in conflict-affected areas. This not only promotes peace and security but also supports the development of legitimate and sustainable economic opportunities in the Great Lakes region.

· Conflict Mineral Policy - Following OECD and EU guidelines, preventing armed groups in the DRC and adjacent countries from benefitting from the sourcing of Conflict Minerals.

· Local Community Support - Improving service levels to clients whilst acting fairly in dealings with suppliers and third parties.

· Environment- Minimising impact on the environment is a strong company focus.

· Training and Development - Dedicated to providing training and development opportunities to staff members.

· Clean water initiative - Helping provide clean drinking water to approx. 26,000 school children and teachers in Rwanda.

· Food and healthcare insurance support - Provided in the Musasa area of Rwanda during the Covid-19 pandemic.

· Corporate Governance - The Company conforms to the QCA Corporate Governance Code 2023 and applies this to all its subsidiaries.

As part of our efforts, we actively participate in a clean water programme that provides the local community with access to clean drinking water through the provision of water tanks and supply systems. We also support community aid programmes that assist vulnerable members. We look forward to continuing these efforts.

Employee and Greenhouse Gas (GHG) Emissions

The Company seeks to minimise carbon or greenhouse gas emissions. The Group's utility bills indicate that it consumes less than 40,000 kWh of energy per annum. It does not have responsibility for any emissions producing sources under the Companies Act 2006.

Energy and Carbon Reporting (SECR)

The Company is a "quoted company" within the meaning of the Companies Act 2006 (Strategic Report and Directors' Report) Regulations 2013, as amended by the Companies (Directors' Report) and Limited Liability Partnerships (Energy and Carbon Report) Regulations 2018 (together, "SECR"). Accordingly, the Company is required to disclose its annual energy use and associated greenhouse gas ("GHG") emissions.

The Company's current activities are restricted to exploration related activities with trenching being the most environmentally impactful. We are not mining or engaged in large scale drilling programmes.

Policies and processes are being further enhanced to ensure there is a more rigorous reporting cycle in which requirements are identified and met before giving rise to any issues. The Company functions with the clear mandate of being in full compliance with corporate standards, applicable environmental laws, regulations and permit requirements.

TCFD Governance of Climate-Related Risks and Opportunities

Transitional statement

As at 31 December 2025, the Company is not fully compliant with the requirements of the TCFD framework (on the basis that this is deemed immaterial based on the current stage of operations). The following disclosures set out where the Company is currently in this regard (i.e. whether or not it is fully compliant, partially compliant or not yet compliant), where we would like to be in the future and what steps will be taken to achieve this. The Company is still at a very early stage of developing its activities and is extremely small in terms of its operations, resources and environmental impact. Nonetheless, the Company's strategy to grow means that its impact on the environment is likely to increase, and its resources and procedures will also need to develop alongside this growth in activity.

In contrast to the Streamlined Energy and Carbon Reporting (SECR) disclosures which requires listed companies to disclose their greenhouse gases emissions, CO2 and energy usage, TCFD is primarily designed to protect shareholders from the impacts of climate change by ensuring companies adapt to the risks and opportunities that climate change presents. In the mining industry an example would be a brown thermal coal exploration company faced with reduced market demand over the next 25 years.

TCFD adherence requires disclosure of Greenhouse Gas (GHG) emissions as part of the Metrics and Targets section. This creates a degree of overlap with SECR requirements, however TCFD's main focus on emissions is to understand how GHG emissions may expose a company to future changes in law or legal challenges, regulation or market dynamics which penalise higher polluting industry sectors, sub sectors or companies.

The disclosures set out below describe whether the Company is fully compliant with the TCFD requirements and, where it is not, explain why it is not yet able to comply. It further describes what procedures are currently in place and the steps the Company expects to take to progress to full compliance.

The Company is committed to complying with local environmental regulations and international disclosure frameworks, including the Task Force on Climate-related Financial Disclosures (TCFD). With regard to the TCFD, the Company ensures that its climate-related financial disclosures are consistent with the TCFD Recommendations and Recommended Disclosures, as aligned with the listing rules UKLR 22.2.24 (1), (2), LR 22.2.25 and LR 22.2.26.

We have made the disclosures below against each TCFD Recommendation and Recommended Disclosure, noting where the Company is in full or partial compliance or where further work is planned to be undertaken to report in the 2026 Annual Report and Accounts.

When making assessments and preparing disclosures, we have considered whether particular issues and related information may influence the economic decisions of the stakeholders. Such an approach aligns with the guidance and recommendations provided by the TCFD regarding the materiality of information. Furthermore, the process of assessing risks and their potential financial impact involved the use of judgements and estimates, which we believe are consistent with the TCFD Recommendations and Recommended Disclosures.

The tables below describe the Company's position on each of the TCFD's 11 disclosure recommendations, with the following keys indicating the level of compliance:

- *Compliant

- **Partially compliant

- ***Not yet compliant

Pillar | Requirement | Company position |

Governance around climate-related risks and opportunities | a. Describe the board's oversight of climate-related risks and opportunities**

| The Board recognises that evolving legislation and regulatory frameworks aimed at addressing climate change may have future financial implications for the Group. In response, the Board proactively engages in climate governance and oversight to ensure it is able to plan for resilience and alignment with best practices. Climate change matters are regularly discussed in management and Board meetings but these are not routinely minuted on the basis that their impacts are often immaterial to the Company's current activities. However, with effect from April 2025, all board meetings are being recorded and matters covering climate change, corporate responsibility and ESG are to be formally minuted. It is intended that these procedures will cover: · Regular reviews of material issues and principal risks, including those linked to climate change. · Establishing and reviewing climate-related policies, identifying areas requiring further action, and delegation of responsibility to in-country managers for local implementation. These changes will be implemented proportionately as the Company's activities grow, with the overarching aim of ensuring that Environmental, Social and Governance (ESG) considerations, including climate-related risks and opportunities, are embedded within the Group's risk management and internal control systems. While climate-related risk is not currently deemed a principal risk due to the Group's present scale, it remains an important consideration within the broader ESG framework. Further information on ESG risks and mitigation strategies is outlined in the "Principal risks and uncertainties" section on pages 30-33. The Audit Committee is responsible for reviewing the Company's annual disclosures in relation to the Task Force on Climate-related Financial Disclosures (TCFD) and other emerging climate risks. To date, the Audit Committee's role has been limited because of the relatively immaterial scale of the Company's operations. During 2026, the Audit Committee papers and minutes will explicitly document its assessment of TCFD disclosures and plans for their future development. The Board collectively drives the Group's short, medium, and long-term strategic decisions. While annual KPIs related to emissions and climate targets are not currently set -reflecting the modest scale of Aterian's present operations - the Board recognises the opportunity to integrate such targets as the Group grows. Opportunities for Aterian plc:As global focus intensifies on climate action, Aterian is well-positioned to benefit from the transition to a low-carbon economy. Opportunities include leveraging sustainable mining practices to attract ESG-focused investors, positioning the Company as a responsible supply partner within clean technology supply chains, and exploring funding or partnership avenues tied to environmental innovation. The Board recognises that early adoption of climate disclosure frameworks and emissions reduction strategies could enhance the Company's reputation, compliance readiness, and long-term shareholder value. As the activities of the Group grow, the Board will develop its strategies in a proportionate way.

|

| b. Describe management's role in assessing and managing climate-related risks and opportunities** | The Board has overarching responsibility, and management has the oversight of day-to-day operations.

Management as a whole is responsible for day-to-day operations, including the identification and evaluation of climate-related risks and opportunities.

|

Strategy: Disclose the actual and potential impacts of climate-related risks and opportunities on the Company's businesses, strategy, and financial planning where such information is material. | a. Describe the climate-related risks and opportunities the company has identified over the short, medium, and long term**

b. Describe the impact of climate-related risks and opportunities on the organisation's businesses, strategy, and financial planning**

| The climate-related risks relevant to the business have remained largely unchanged compared to previous reporting periods, and where relevant, opportunities have also been identified, both within the context of the current activities of the business being relatively small scale.

The climate-related opportunities stem from the demand for minerals that support the energy transition (e.g., copper and lithium), which is expected to rise. Aterian is strategically expanding its trading and exploration into African regions with deposits of these metals which management believes supports green technology markets. This opportunity is driven by demand from the renewable energy sector and electric vehicle (EV) battery manufacturing. This presents an opportunity for Aterian to attract investors to its critical metal projects in Africa. Adopting energy-efficient and renewable-powered exploration technologies could also result in cost savings and enhanced environmental credentials.

To date, Board minutes and related papers have not documented its decision-making processes across short-term, medium-term and long-term horizons, but this is to be implemented during the course of 2026 to cover relevant climate-related risks and opportunities as described below.

Short-Term (0-3 Years): (Three-year period to the end of 2027): This is typically the life of the Company's exploration licences, over which the management and the Board monitor the Company's liquidity and viability.

Such period is typically the term of joint venture agreements such as the Company's agreement with Rio Tinto, and the initial tenure of a particular exploration licence or permit. The Company has a detailed financial plan that is actively managed and adapted to changes in external circumstances.

Climate-related risks deemed to affect the Company in the short-term are not as prevalent as those in the medium and longer term.

Policy and legal risks which Aterian is facing are similar to other players in the critical minerals industry:

• New and evolving reporting obligations may result in higher compliance costs but at present these are not material.

• Risks due to certain jurisdictional policy changes where exploration activities are undertaken, such as emissions target requirements or carbon pricing regulation, causing mining operations post-exploration to be commercially unviable.

We believe these risks are relatively low in the short-term but become more material over a longer horizon as the Company's operations become more significant..

Risks include regulatory changes in the UK and in the countries where the Group operates (Morocco, Rwanda, and Botswana) that may increase compliance costs and necessitate additional staffing to facilitate new regulatory requirements, such as baseline surveys and reporting obligations. Regulatory changes could cause delays in permitting exploratory activity due to concern around climate-related impacts of potential mining activity as a result of the outcomes of the exploration work, which may in turn reduce time spent undertaking field programmes, as well as physical risks like extreme weather events (e.g., flash floods, elevated summer temperatures) that could further disrupt exploration activities and/or increase the safety risk for field teams.

Although not yet readily apparent, community concerns about environmental impacts within the context of climate change could lead to reputational risks and delays to the growth in planned activities.

The financial impact of these risks and opportunities has not yet been quantitatively assessed. Given the relatively small-scale activities currently undertaken by the Company, resource allocation has been proportionate in risk assessment, and management deems the short-term impact to be minimal.

Opportunities Product and Market Expansion: The demand for minerals that support the energy transition, such as copper and lithium is expected to increase. Aterian is strategically expanding its trading and exploration into African regions with deposits of these metals, focusing on assets that support green technology markets. This opportunity is driven by demand from the renewable energy sector and electric vehicle (EV) battery manufacturing. This presents an opportunity for Aterian to attract investors to its critical metal projects in Africa.

Adopting energy-efficient and renewable-powered exploration technologies could also result in cost savings and enhanced environmental credentials. The financial impact of this opportunity has not yet been assessed in quantitative terms.

Medium-Term (3-10 Years): (Seven-year period to the end of 2034). This period is likely to feature development of successful licences into assets capable of mineral production.

Climate-related risks will be factored into scenario analysis using various mineral input prices to support the Board in decision-making for field investment proposals in line with the Group's strategy.

Technology risks are considered relevant in the medium and long-term. As global and jurisdictional legislation evolves, we may need to allocate capital to emissions reduction investments, such as carbon capture and storage, which may not provide direct revenue and, therefore, may impact the medium to long-term value of the Company.

Reputational risks include risks of stakeholder concerns and disengagement resulting from other climate-related risks, as well as increasing difficulty in accessing capital markets for future growth opportunities. We believe these risks are less of a concern in the short-term since the Company has longstanding relations with its key shareholders and noteholders. However, these may become more significant in the medium and long term.

Physical risks which may affect the Company and its operations include floods, severe heat and/or desertification.

As climate change continues, we believe that these severe weather events may occur more frequently and during unexpected periods, potentially further impacting business operations and finances. We currently operate throughout the year, but in the middle of summer, temperatures on the ground in Morocco and Botswana can exceed 40oC.

Rwanda has a more temperate climate due to its elevation. However, if temperatures were to change sharply within a short period due to climate change, this could negatively impact operations, for example, by reducing equipment productivity due to overheating or increasing fire risk.

Other risks include water scarcity, which could hinder fieldwork programs, camp construction, and the provision of water for extensive field activities in remote desert locations. Permitting may not be granted for the development of projects if water scarcity in the region is an issue (lack of reservoirs, unsuitable groundwater, etc.). Significantly increased costs of compliance and related reporting may also become more apparent, which reduces the cost and time efficiency of executing field programmes.

Opportunities in this period include the increasing demand for sustainably sourced minerals, which could help Aterian secure environmentally conscious investors. Technological innovations, such as drones, remote sensing and machine learning could improve exploration efficiency and reduce environmental impact. The Group has not yet explored such technologies but is likely to do so in the medium term. Potential direct investment in the energy sector may provide upstream opportunities for the provision of critical metals.

Longer-Term (10+ Years): (Period covering beyond 2034). This period is likely to feature both the construction of facilities and the subsequent production of mineral ore.

This is defined by the opportunities being identified that are mostly affected by climate-relate risks.

Opportunities - Investments in Aterian could present significant opportunities for the provision of notably copper and lithium aiding the transition away from fossil fuels.

Additionally, Aterian could solidify its position in critical minerals, enhancing its market reputation in a low-carbon economy.

Building long-term trust and fostering good cooperation with local and national stakeholders through local community training for sustainable exploration activities is supported by Aterian in its efforts to mitigate the effects of climate change on local populations. This responsible approach, demonstrated during the exploration stages, further enhances Aterian's reputation.

Impact on the Organisation's Businesses, Strategy, and Financial Planning:

We acknowledge that the transition to a lower carbon economy presents both risks and opportunities for Aterian. As described above, the impact on short-term strategy and financial planning remains minimal and proportionate to business operations, but we have in place the necessary flexibility to adapt as and when we see the risks evolve. In respect of medium-term and long-term financial planning, we are acutely aware of the climate-related risks and our ability to execute various projects.

With respect to physical risks, we will factor this into our strategic planning through extended and more frequent periods when exploration may not be possible and thus periods during which operations and revenues either cease or reduce.

We consider transition risks outlined in (a), above, within the context of our strategic and financial planning, noting the following potential impacts which could arise within the context of climate change:

i) reduced demand and lower pricing for minerals - resulting in lower future revenues; ii) higher operating costs in our supply chain; iii) high investment spend relating to climate risk mitigation activities through increased operational spend and increased downtime due to extreme weather events.

For physical risks, while important from a governance perspective, we deem the financial and operational impact to be lower, as we currently operate successfully in extreme weather conditions and believe we will do so going forward.

We take a conservative approach in our forward planning and therefore do not factor in opportunities that may arise in the short, medium or long-term through climate change.

As the scale of our operations increases, we will devote more resources to governance, including reporting, and these will feature in our future strategic and financial planning.

|

| c. Describe the resilience of the organisation's strategy, taking into consideration different climate-related scenarios, including a 2°C or lower scenario***

| Resilience of Strategy in Different Climate Scenarios:

The Company has not yet performed a formal scenario analysis on the potential impacts of different climate scenarios and is therefore not compliant with part (c.) of the Strategy requirements.

The limited scale of the Company's operations has meant that an allocation of resources to such scenario analysis will not be possible until we are fully funded for the medium and long-term. |

Risk Management: Disclose how the organisation identifies, assesses, and manages climate-related risks. | a. Describe the organisation's processes for identifying and assessing climate-related risks** b. Describe the organisation's processes for managing climate related risks** c. Describe how processes for identifying, assessing, and managing climate-related risks are integrated into the organisation's overall risk management** | The Board is the conduit through which climate-related risk management is enacted.

At present, as described above in its transition statement, the Company has not yet developed detailed processes for identifying and assessing climate-related risks. These will be developed as the Company's activities become more extensive.

Country managers support the Chief Executive Officer in his oversight role and will, when activities become material in scale, perform management and reporting on the risks when these are formally identified.

The processes described above under the "governance" pillar are part of our overall Group Risk Management framework and form an integral part of Aterian's risk management and internal controls system. Risk management covers both physical and transitional climate-related risks.

The Company endeavours to constantly improve its systems of risk management and internal controls. However, with the limited scale of operations and resources, the Company does not report any further material updates on these matters in this report.

|

Metrics and Targets: Disclose the metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material. | a. Disclose the metrics used by the organisation to assess climate-related risks and opportunities in line with its strategy and risk*** management process. b. Disclose Scope 1, Scope 2 and, if appropriate, Scope 3 greenhouse gas (GHG) emissions and the related risks*** c. Describe the targets used by the organisation to manage climate-related risks and opportunities and performance against targets*** | Metrics Used to Assess Climate-Related Risks:

As of now, the Company does not track specific greenhouse gas (GHG) emissions metrics, such as Scope 1, Scope 2, and Scope 3 emissions, because the exploration activities it currently undertakes are in the early-stages and not emissions-intensive.

For further context, the Company meets the Streamlined Energy and Carbon Reporting emissions threshold exemption within the UK, meaning that it consumes less than 40MWh per reporting period.

The Company is still in the early stages of its development and does not currently record emissions from its business activities. However, as the activities grow, it will establish a baseline for GHG emissions target measurement.

Future Plans for Emissions Reporting: Aterian has not yet developed its plans to measure and manage emissions in the future. As the scale of operations grow, the Company intends to focus on the following:

· Scope 1 Emissions: Direct emissions from fuel use in exploration vehicles and equipment will be tracked by monitoring fuel consumption. · Scope 2 Emissions: Indirect emissions from electricity used at exploration sites and offices will be tracked through utility bills and fuel used for generators, which are currently leased as necessary (where their use is necessary). · Scope 3 Emissions: Although tracking Scope 3 emissions (e.g. transportation and supply chain emissions) will be phased in, the Company plans to assess indirect emissions in the future.

Targets for Managing Climate-Related Risks and Opportunities: Aterian has not yet established specific climate-related targets. In this regard, the Company is not compliant with the TCFD requirements. However, when these are established, these targets will focus on emissions reduction and broader sustainability goals aligning with industry best practices. These are likely to include:

· Emissions Reduction: the transition of all exploration vehicles to low-emission or renewable energy-powered alternatives, where feasible.

· Water Management: During exploration stages and at any future production stage, Aterian will seek to limit water consumption utilising, where possible, smaller, flexible and adaptable field teams, encouraging minimal water use wherever possible and recycling water where possible and optimising water consumption at any future production site.

· Energy Efficiency: The Company will seek to improve energy efficiency across exploration and development activities by incorporating low-energy technologies and practices.

· Sector-Specific Metrics: Aterian plans to align its reporting and targets with those of its industry peers, focusing on metrics such as carbon intensity per kilometre of exploration drilling or per tonne of the identified resource.

Implementation and Monitoring: Aterian has not yet established baseline metrics and is therefore not compliant with the TCFD requirements. Once the Company's activities are significant, we will engage third-party experts, as required, to develop a robust emissions measurement and reporting framework and report progress annually in alignment with international standards, such as the TCFD and CDP.

|

The Board is responsible for overseeing the Group's environmental, health, and safety, as well as corporate social responsibility programmes, policies, and will implement measures to monitor performance in these areas. The Board constantly strives to reduce the environmental impact of our operations.

Our People

Aterian operates within a favourable framework for labour relations based on a non-discriminatory, equal opportunities employment system that respects diversity and facilitates communication at all levels of the Group. The Group provides a healthy and safe working environment by implementing the best available international practices and procedures.

Equal Opportunity

The Company promotes a policy of creating equal and ethnically diverse employment opportunities, including those related to gender. The Company promotes and encourages employee involvement wherever practical as it recognises employees as a valuable asset and is one of the key contributors to the Group's success.

Communication

Aterian promotes and encourages the establishment of broad communication channels, continually seeking opportunities for conversation with its various stakeholders to ensure that business objectives remain in tune with social needs and expectations.

The Company will continually strive to provide relevant, transparent, and accurate information about its activities, encouraging continuous improvement in this area.

Eastinco Limited currently provides maintenance support for 65 solar water purification units, which were donated free of cost to schools in Rwanda. Each unit is 100% solar-powered and can provide safe, UV-filtered, and bacteria-free drinking water for up to 400 schoolchildren and teachers. This clean water initiative offers safe drinking water to over 26,000 children.

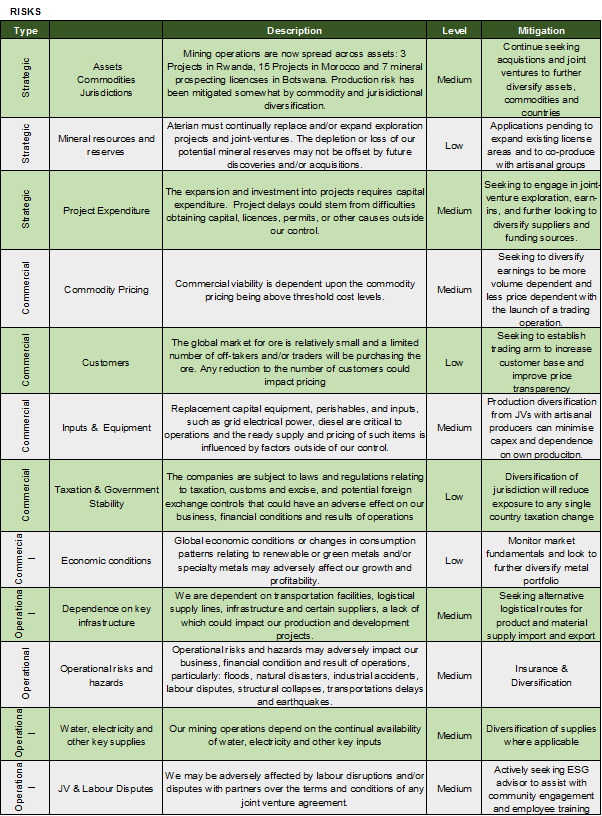

Risks

Risk management is one of the core responsibilities of the Board, and it is central to the decision-making process. The Board's fundamental duties as to management are:

· Assessing (quantitively and qualitatively) the principal risks to the Company. Principal risks are those risks or combination of risks that could seriously affect the performance, future prospects or reputation of the Company;

· Recognising and assessing emerging risks. Emerging risks are those which have not yet occurred but are at an early stage and anticipated to increase in significance over the medium to long-term time horizon;

· Risk management oversight and promotion of a risk mitigation culture.

Principal Risks and Uncertainties

The Group operates in an uncertain environment, subject to several risk factors. The Directors have carried out a robust assessment of the principal risks facing the Group, including those that threaten its business model, future performance, solvency and liquidity.

They consider the following to be the principal risk factors that could materially and adversely affect the Group's future operating results or financial position.

Deterioration in the Metal Markets in Particular

There is a risk that changes in relevant law and legislation could have an adverse effect on the Group's future performance, expected return and or feasibility of any project. The Group is also exposed to general macroeconomic risk, including changes in the economic outlook in its principal markets and government changes in industrial, fiscal, monetary or regulatory policies. The Board continues monitoring developments in the market so that it can adapt its strategy. The management team has wide-ranging expertise in capital markets, mineral exploration, and trading, which, together with a flexible cost structure, enable the Group to adapt its organisation to changes in circumstances.

Funding Risk

Although the Group has sufficient working capital for at least 12 months from the date of this report, the Group may not be able to obtain additional financing as and when needed, which could result in a delay or indefinite postponement of exploration and development activities. In common with many exploration entities, and prior to trading revenue generation, the Group will need to raise further funds to progress the Group from the exploration phase into feasibility and eventually into the production of revenues.

Dependence on Key Personnel

The Company has a small management team, and the loss of a key individual could have a detrimental impact on the future of the Group's business. The Group's future success will also depend mainly on its ability to attract and retain highly skilled personnel.

There can be no assurance that the Group will be successful in attracting and retaining such personnel. The Group seek to create a workplace that attracts, retains, and engages its workforce. Efforts are also made to attract new talent and skilled people.

Environmental Risk

There may also be unforeseen environmental liabilities resulting from both the future and/or historic exploration or mining activities, which may be costly to remedy.

In addition, potential environmental liabilities as a result of unfulfilled environmental obligations by the previous owners may impact the Group. If the Group is unable to fully remedy an environmental problem, it may be required to stop or suspend operations or enter interim compliance measures pending completion of the required remedy. Environmental management systems are in place to mitigate environmental hazard risks.

Political Risk

All countries present a certain level of political risk which may ultimately disrupt business operations for some period of time. However, the Company's subsidiary management teams possess extensive experience operating in Rwanda, Morocco and Botswana.

Our local joint venture partners and subsidiary management teams maintain excellent communication with local stakeholders, ensuring that they have the necessary knowledge and expertise to assist the Company in mitigating any political risk associated with any particular project investment.

Together, we are committed to providing effective management and reducing the likelihood of political risk adversely affecting the Company's operations.

Estimates of Mineral Reserves and Resources

Mineral resources are estimates and no assurance can be given that any particular grade or tonnage will be realised or that they will be converted into ore reserves or will ever qualify as a commercially mineable (or viable) deposit that can be legally and economically exploited.

As a result of these uncertainties, there can be no assurance that any potential mineral resources defined by the Group's exploration programmes will result in profitable commercial mining operations. The Directors are confident that they have put in place a strong management team capable of dealing with the above issues as they arise.

Corporate Responsibility

We have defined the scope of our Group's responsible business practices as falling within the following key focus areas:

• Health and Safety - ensuring the safety and well-being of our staff

• Environment - managing our environmental impact areas of waste, energy and water

• Employees - supporting our people to develop and flourish within the business

• Community - positive interaction with the communities in which we operate

• Ethical Standards - operating to the highest ethical standards

We remain committed to ensuring these activities become embedded in how we operate and contribute to the success of our business. These include not only identifying and managing business risk but exploring opportunities to add value to the business.

Gender and Diversity Analysis

The following tables provide an analysis of the diversity of the individuals on the Company's board and in its executive management as of 31 December 2025:

Gender analysis | Number of board members | Percentage of the board | Number in executive management (Non-Board) | Percentage of executive management (Non-Board) |

Men | 5 | 100% | 1 | 50% |

Women | 0 | 0% | 1 | 50% |

Ethnicity analysis | Number of board members | Percentage of the board | Number in executive management (Non-Board) | Percentage of executive management (Non-Board) |

White British or other White (including minority-white groups) | 3 | 60% | 1 | 50% |

Mixed/Multiple Ethnic Groups | 0 | 0% | 0 | 0% |

Asian/Asian British | 0 | 0% | 0 | 0% |

Black/African/Caribbean/Black British | 1 | 20% | 0 | 0% |

Other ethnic group, including Arab | 1 | 20% | 1 | 50% |

The Company has not met the following targets on board diversity during the year: (i) at least 40% of the individuals on its board of directors are women; (ii) at least one of the following senior positions on its board of directors is held by a woman: (A) the chair; (B) the chief executive; (C) the senior independent director; or (D) the chief financial officer. Whilst the board aims to comply with these targets, the availability of suitable candidates with experience and expertise for these positions in the jurisdictions where the Group operates limits the opportunity to meet such targets. The Company is, however, mindful of these targets when making appointments.

The Company's approach to collecting data for the purposes of making the disclosures above is to promote diversity, inclusion and equal opportunity without referencing specific groups. Such data is collected when employees are recruited. The board considers diversity in all its forms, including gender, social and ethnic backgrounds and personal strengths. The Group's senior managers and other staff (excluding directors) are summarised as follows:

Gender analysis | Number of senior managers | Percentage of senior managers | Number of other employees | Percentage of other employees |

Men | 5 | 83.33% | 6 | 60.00% |

Women | 1 | 16.67% | 4 | 40.00% |

The Board recognises that the Group's long-term success depends on the engagement and commitment of its employees and therefore considers their interests in its decision-making processes. The Group aims to ensure that the workplace is safe and inclusive, welcoming diversity and offering everyone the opportunity to develop to their full potential. The Board has sought to enhance communication and better understand the interests of employees throughout the year. We have provided regular team updates and opportunities for Q&A. This has ensured staff receive answers to a wide variety of questions and allowed the Group to provide staff with pertinent information and key business performance updates.

The Board recognises the need to operate a gender diverse business and will ensure this is reviewed as the business develops. The Board also ensures that any employment decisions consider the necessary diversity requirements and comply with all relevant employment laws. The Board is satisfied that it possesses the experience, training, and qualifications required to operate this business at this stage of its development.

Health and Safety

The Group has maintained strict compliance with its Health and Safety Policy and is pleased to report that there were no lost-time accidents during the year.

Environment

No Group Company has had, nor has it been notified of, any instance of non-compliance with environmental legislation.

Key Performance Indicators

The Group utilises several strategic key performance indicators ("KPIs") to measure financial and non-financial performance. These KPIs are linked to our strategic objectives, helping to measure business performance and are focused on both the new trading business and exploration activities.

The most important KPI in 2025 has been the level of cash within the business, ensuring sufficient liquidity to fund operations and strategic investments. In addition to cash position, the Group monitors the following KPIs to track progress and align efforts with our growth and value-creation strategies:

1. Financial KPIs:

1. Exploration Spend vs Budget - Tracks the actual capital deployed on exploration programs compared to planned expenditures to ensure cost discipline.

2. Cash Burn Rate - Monitors monthly operational spending to evaluate sustainability and the timing of future capital requirements.

3. Return on Exploration Investment (ROEI) - Measures value generated relative to capital spent on exploration, particularly in identifying viable mineral resources.

4. Trading Revenue Growth - Evaluates performance of the Group's new trading business line and its contribution to overall revenue.

These KPIs are monitored internally but not published with specific figures in the annual report.

2. Operational KPIs:

1. Number of Active Exploration Projects - Monitors the scale and intensity of ongoing exploration work across jurisdictions.

2. Drilling Metres Completed - A key metric to assess the scope of subsurface exploration and geological data acquisition.

3. Number of New Licences or Permit Approvals - Reflects the Group's ability to secure new exploration rights and regulatory compliance.

3. Technical and Resource KPIs:

1. Discovery Rate - Measures success in identifying promising mineralisation zones per project or per metre drilled.

2. JORC/NI 43-101 Resource Estimates - Progress in upgrading exploration targets to compliant mineral resource categories.

3. Grade and Tonnage Metrics - Quality and size of identified deposits, indicating potential economic viability.

4. ESG and Non-Financial KPIs:

1. Health and Safety Incidents - Tracks the frequency and severity of workplace incidents to ensure safe operations.

2. Community Engagement Score - Qualitative and quantitative indicators of stakeholder relations and community support.

3. Environmental Compliance Rate - Measures adherence to environmental regulations, including reporting, waste management, and rehabilitation.

These KPIs provide a comprehensive framework for performance evaluation, risk management, and strategic decision-making. The dynamic nature of exploration activities requires frequent review and adaptation of these indicators to reflect evolving project milestones, market conditions, and corporate priorities.

Other Non-Financial Information

The Board acknowledges that a strong business relationship with current and future service providers and future customers is a vital part of the growth.

Aterian's core values and principles, as well as the standards of behaviour to which personnel across the Group are expected to adhere, are outlined in the Group's Code of Conduct.

These values and principles are applied to our suppliers and our stakeholders. The Group has detailed policies and procedures in place on a range of relevant areas such as business ethics, diversity and inclusion, insider dealing and share dealing and human rights and modern slavery