13th Apr 2026 07:00

13 April 2026

Golden Prospect Precious Metals Limited

(the "Company")

Annual Report and Audited Financial Statements

The Company is pleased to announce its final results for the year ended 31 December 2025.

For the full report, please click the link below:

http://www.rns-pdf.londonstockexchange.com/rns/0828A_1-2026-4-12.pdf

Year End Highlights:

· Net asset value (NAV) per share total return of 170.5%;

· Share price increase of 164.8% from 35.5p to 94p;

· Named the top performing investment trust of the year by the Association of Investment Companies (AIC);

· Performance recognised by two awards: Citywire Investment Trust Insider Specialist Equities Category Award and Investment Week's Investment Company of the Year Awards within the Specialist category;

· Appointment of Helen Green as Non-Executive Director and Chair of the Audit Committee;

· Appointment of Chris Waldron as Non-Executive Director and member of the Company's Audit, Management Engagement, and Remuneration & Nomination Committees, effective from March 2026.

Chairman's Statement

Post period end significant developments

Before moving on to reporting on the financial year ended 31 December 2025, we must highlight the Company's announcement of 9 March 2026, stating that the Board had been informed that the Company's portfolio managers, Keith Watson and Robert Crayfourd had resigned from Manulife CQS Investment Management ("CQS" or "The Manager"), the Company's investment manager. Keith and Robert are each subject to a three-month notice period and they have continued to manage the Company's portfolio. In order to best protect the Company's interests, the Board has served protective notice to CQS while it considers the options for the future management of the Company. The notice period between the Company and CQS is 12 months. Further announcements shall be made in due course.

Foreword

Notwithstanding the aforementioned developments, I would like to congratulate the investment managers on their spectacular performance in 2025. The Association of Investment Companies (AIC) has confirmed that Golden Prospect Precious Metals was the top performing investment trust of the year. It is a tribute to their talents that they delivered a NAV total return of 170.5% in the context of the gold price rising 52.8% in Sterling, while also outperforming the main gold mining ETFs.

This is both a proud and poignant time for me personally as I will be stepping down as Chairman at the coming AGM. It is, however, reassuring to hand over the reins of a Company in fine fettle after such a successful run, with likely more to follow.

Recent market developments

This time last year we noted the decoupling of the US bond market from gold which has not been witnessed since the 1970's. As the last vestiges of the Gold Exchange Standard were abandoned, it led to further devaluation and inflation. Precious metal mining stocks performed very well in that decade while other sectors of the stock market stagnated.

The breakdown in correlation with US Treasuries has liberated gold and silver, allowing them to undertake an exercise in price discovery. While some may view record highs as a reason to take profits, seasoned investors know that breakouts can go much farther and faster than expected. There is a degree of academic snobbery when referring to speculators but ultimately, they are like pioneers and prospectors who take great risk to achieve great rewards with no guarantee of success. They blaze a trail for others to follow as the price action establishes a more comfortable path for future investors.

While silver has surged, followed by a fast and furious correction, it is in complete contrast to the episode in 1980 where a small group tried to corner the market and drive prices higher for their own gain. Instead, the latest trend is underpinned by fundamentals and industrial demand. As central banks continue to accumulate precious metals the US dollar has fallen to 40% share of their global reserves, while gold is now at 30%, on the back of its higher price.

We previously highlighted that the miners were in a stealth bull market. While the spotlight has certainly returned to the metals, mainstream investor participation remains surprisingly light. The best-known gold mining Exchange Traded Fund, the VanEck Gold Miners ETF (or GDX index) witnessed widespread liquidation of its shares until mid-2025. While the selling has stabilised, there is little in the way of fresh investment. It is a very strong indication that we are far from anything approaching a classic bubble in the sector as the degree of participation, especially in the more risk-on mining shares, remains minimal.

We are witnessing a denouement of the 'Magnificent Seven' technology names as the bull market is at last broadening away from this narrow range of shares. Evidence of this is apparent as value-orientated markets in Europe performed very well, especially the FTSE-100 which was once mockingly described as the 'Jurassic Index' by a US hedge fund manager.

Performance

I am pleased to report on an outstanding year for the Company. Following a 20.4% gain in 2024, over the course of 2025 the NAV rose by 170.5% from 43.1p to 116.60p with a peak value of 117.4p. The share price likewise rose substantially from 35.5p to 94.0p, gaining 164.8%, with highs in early October at 103.3p. Gearing contributed 7.3%, essentially offsetting the 6.7% NAV dilution from the annual subscription right exercise.

Compared with equivalent Exchange Traded Funds, performance continued to outpace the VanEck Gold Miners ETF (GDX) which rose 137.1% and the VanEck Junior Gold Miners ETF (GDXJ) which rose 153.4% in Sterling terms. This once again shows the benefits of active management at a time when so many have been lured into taking a passive approach to investing. Although much has been made of the recent volatility in January 2026, at the time of writing the share price is close to where it was at the end of 2025 while the NAV has risen.

Having been in the doldrums for some time, we are at last witnessing a return to normality where precious metal mining shares outperform the underlying metals. Gold rose by 64.6% in US Dollar terms and 52.8% in Sterling, highlighting an unusual period of strength in the Pound. For UK-based investors the asset gains have more than offset the currency loss. Should we see further Dollar weakness then this would likely be a potent support for further precious metal price appreciation, given the historic inverse relationship.

Gearing

As mentioned above, given the strong portfolio returns over the period, gearing has served its purpose and contributed 7.3% to NAV returns. The Company's investment manager (MCQS) has proved to be prudent over many years in their use of leverage, by reducing borrowings, and therefore risk, when the market outlook is uncertain. At the close of the year, the gearing level stood at 2.4% of NAV, having been as high as 11.1% in July (the maximum permissible is 20%).

Subscription Rights

In November, under the Company's annual subscription rights programme, shareholders had the right to subscribe for 1 new share for every 5 shares held at a price of 48p (being the Net Asset Value of the Company on the 2024 subscription date). The position was well 'in the money' by the time the exercise was undertaken.

Given that there was a cap of €8m on the value of capital that could be raised, allotments had to be scaled down to 78.21%. Applications from Shareholders amounted to 13,895,183 shares which were pared back to 10,867,374. Those who decided not to participate saw their rights snapped up by other investors. The so-called 'rump' of unexercised subscription rights allowed 3,718,555 new Ordinary Shares to be placed by our brokers in the market. This meant that 14,585,929 new Ordinary Shares were issued growing the overall total to 107,834,428, providing the fund managers with fresh assets to grow. The fourth Subscription Rights Price for 2026 has been set at 104.63 pence which was the fully diluted NAV of the Company on 1 December 2025. Hopefully the share price will be well in excess of this target by November 2026, allowing further capital to be raised. At the time of writing the Company's net assets stood at c.£134 million.

Discount, marketing and awards

There was some improvement in the discount over the year. In 2024 it averaged 20.0% while 2025 saw an average of 17.1%. Following the share price surge in August and September we enjoyed a short-lived premium of 0.9%. However, by the end of the year the discount had widened again to 18.0%.

As ever we continue to refresh our marketing initiatives to target an extended audience outside of traditional wealth managers to generate further demand for the Company's shares. Tavistock, a leading London-based press and investor relations firm, was once again retained to support us in these endeavours. We had strong media coverage during the course the year, particularly in November, when the Company was recommended by Jeff Prestridge in his weekly column in the Mail on Sunday. This was a powerful endorsement, given his strong following and more than 30 years' experience, first as personal finance editor of The Mail on Sunday and latterly, group wealth and personal finance editor at the publication. The Company also featured in Joanne Hart's MIDAS column in The Sunday Times.

The Trust's performance was recognised with two awards towards the end of 2025 - first, Golden Prospect Precious Metals won the Citywire Investment Trust Insider Specialist Equities Category Award, and soon after we were crowned the winners of Investment Week's Investment Company of the Year Awards within the Specialist category.

Ongoing Charges Ratio (OCR)

The Company uses the AIC's methodology for calculating the Ongoing Charges Ratio (OCR). In 2024 the OCR stood at 2.21% and by the close of 2025 it was reduced to 1.99% as the Company's fixed costs were spread across a much larger asset base. With the on-going growth in the NAV we hope to see a further reduction in the coming year below the 2% level.

Saba standstill agreement

Shareholders may be aware of Saba Capital, a US activist investor which has targeted the UK closed end fund sector since 2024. Although the Board is not aware of Saba Capital ever being on its share register, as announced on 1 July 2025, the Company had the opportunity to negotiate and enter into a standstill agreement with Saba, which will be in effect until the Company's AGM in 2028. Under the terms of the agreement, Saba has agreed not to call any general meetings or vote against the recommendation of the Board on specified ordinary course resolutions proposed at a general meeting of the Company.

Board changes

At the Annual General Meeting last May, Rob King retired from the Board having been in situ since the Company's launch in 2006. Graeme Ross also stepped down from the Board, having been Chair of the Audit Committee since he joined the Board in 2018. He was ably replaced by Guernsey-based Chartered Accountant Helen Green. Helen has a background in audit from her time working for Saffery in London which culminated with her being an audit partner before her move to Guernsey. Since her move in 2000 and until her retirement on 31 March 2026, she was an executive director of Saffery Trust, a GFSC regulated fiduciary business. She has extensive experience in corporate governance through her roles as non-executive director of listed investment companies (including as audit committee chair and chair) over the last 15 years.

I will be stepping down as Chairman at the forthcoming AGM, having joined the Board in 2014 and been Chairman since 2023. I am leaving the role in the very capable hands of Monica Tepes, subject of course to Shareholder approval.

Since joining the Board in 2024, Monica has made an immediate and meaningful impact. Her deep understanding of the investment trust sector - the trusts, the investors and the service providers - together with her judgement and clarity of thought, have been evident in her many valuable contributions to the Board. I and fellow director Helen Green are confident that the Company will be in excellent hands under her leadership.

Underpinning Monica's contributions is deep specialist experience in the investment trust sector. She began her career as a fund analyst and assistant portfolio manager at a wealth manager before moving to the sell-side, where she held senior roles across research, investor relations, corporate broking, corporate advisory, and marketing and product development.

In December, with the help of an independent recruitment consultant, we initiated a search for a new director as I shall be stepping down from the Board at the end of this year. We have since concluded the search and appointed Mr. Chris Waldron as a director with effect from 26 March 2026, allowing sufficient time for a smooth handover and transition before my departure.

Chris brings a wealth of relevant experience and expertise and we are delighted to welcome him to the Board. He is Chair of Crystal Amber Fund Limited and a director of Bluefield Solar Income Fund as well as a number of unlisted companies. He has over 35 years' experience as an investment manager and until 2013 was Chief Executive of the Edmond de Rothschild Group in the Channel Islands. He previously held investment management positions with James Capel, Bank of Bermuda, the Jardine Matheson Group and Fortis. A graduate of the University of London and Cranfield University, he is a Fellow of the Chartered Institute of Securities and Investment.

Outlook and closing remarks

In the Interim Report I stated that I didn't believe this was the end of the bull market, but likely the end of the beginning. The short space of time since then has shown these words to be prophetic. The surge in precious metals, especially silver, gives an indication that we are entering the middle phase. As is often the case in a booming market (rather than a bubble), the narrative outpaces the price and inevitably there is a high degree of excitability. The 30% sell-off in silver at the end of January 2026 was particularly brutal but proved to be a taste of things to come. A further downturn was experienced in March as conflict escalated with Iran and the Strait of Hormuz was effectively closed to shipping. However, by early April the NAV and share price had recently started to rally so hopefully this is the beginning of a recovery rather than a false dawn.

The upside of such corrections is that it allows institutions to enter the market, especially as many have been caught short with painfully low weightings. Gold miners' valuations are still priced below 2020 levels, relative to the bullion price so some catch-up is warranted. The case is even more extreme for the silver miners which the fund managers have been steadily increasing. History would tend to suggest that the biggest parabolic surge is yet to come, albeit in the years ahead as we enter the final phase of the bull market.

In this, my final report, I hope shareholders will indulge me with a personal reflection. The timing of my exit in late 2026 will coincide with my 60th birthday. In the Chinese Lunar cycle, 2026 is the Year of the Horse as was my birth year 1966. The latter saw the release of the spaghetti Western, The Good, the Bad and the Ugly, where three gunslingers hunt for a cache of Confederate gold. Featuring arduous journeys and episodes of violence it is a metaphor for the history of precious metals down the ages. One of its moving musical compositions was the aptly named Ecstasy of Gold which was a fitting tune for last year. However, longer term investors may find another movie title more pertinent, namely, The Agony and the Ecstasy.

In closing, we thank shareholders for their continued support and invite them to study the Investment Manager's report for their economic assessment and coverage of the portfolio holdings. We will soon be in touch with details of the forthcoming Annual General Meeting.

Toby Birch

Chairman

April 2026

Investment Manager's Report

Performance

The trust's NAV gained 170.5% for 2025, after the 6.7% dilution from subscription share issuance in November/December. The drivers of performance were broad and across almost every name in the fund.

GPM Net Asset Value, Gold Spot Price, GDX Index and GDXJ Index (Jan 2025 - Dec 2025) (in GBP)

The GDX Index represents the VanEck Gold Miners ETF and the GDXJ Index represents the VanEck Junior Gold Miners ETF.

Summary

2025 marked a record-breaking year for precious metals that ultimately lifted metals more broadly. Gold posted gains of 52.8%, whilst Silver gained 130.2% and lesser precious metals like Platinum and Palladium saw gains of 104.9% and 64.8% respectively (all quoted in Sterling).

The key drivers of precious metal gains were;

· Geopolitical uncertainty

· Central Bank demand

· Bar and coin demand

· Debasement fears

· Inflation

Geopolitical uncertainty

Centre to this has been US policy on tariffs and trade protectionism, which has been the primary driver, but it also included the ongoing Russian/Ukrainian war and the rising tensions between the US and Iran. Later in the year, the US president made claims over Danish‑controlled Greenland, directly threatening a NATO state's sovereignty.

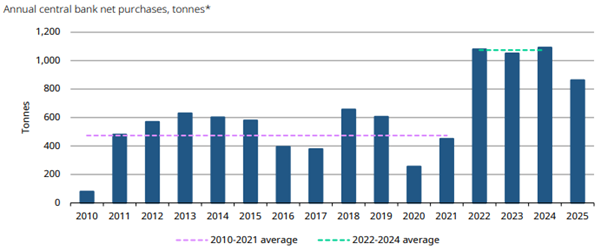

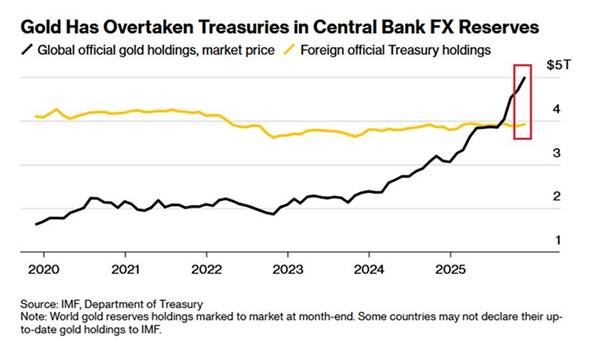

Central Bank Demand

Central Banks are likely to continue to look to diversify away from US treasuries given the US's weaponisation of the US dollar, which has driven strong purchases of gold since the Russian invasion of Ukraine. Whilst the tonnage in 2025 was lower, the value was higher in dollar terms.

Source: Bloomberg

This has now seen gold exceed US treasuries as the largest Central Bank holding, via a mix of purchases and price appreciation.

The US Dollar's role as the global reserve currency is waning at the margin, but would take many years to really see a dramatic shift. Perhaps more important has been the US's openness to encouraging a weaker dollar so to support domestic manufacturing, with the dollar falling 9.4% in 2025 further supporting flows to gold.

The knock-on impacts on this are the dollar being an inferior reserve currency, with inflationary impacts domestically on imports, but perhaps most significantly this reduces the appeal of holding US treasuries.

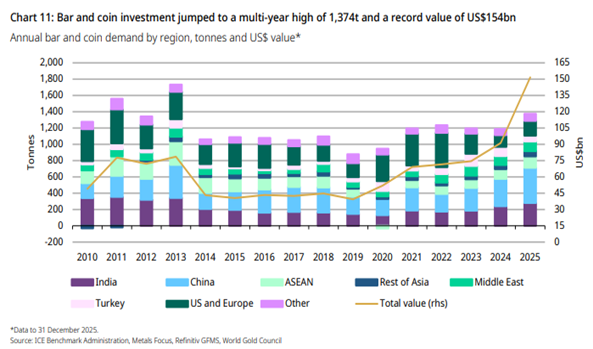

Bar and Coin Demand

Bar and coin demand has been a primary driver of the strength in precious metals through 2025. Much of this has been driven by particularly strong demand from China and to a lesser extent India. The Chinese side of demand is supported by the restricted capital markets in the country that have historically been weighted toward the domestic property sector, but given the collapse in the property sector this has left precious metals as an attractive alternative and continues to support flows into precious metals.

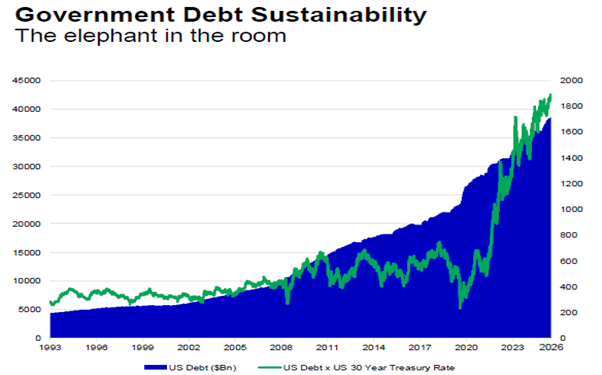

Debasement Fears

Debasement refers to the loss of purchasing power of domestic currencies. The primary driver to this is persistent inflation and continued deterioration of governments' fiscal stability, as higher rates increase the government debt interest to unsustainable levels. They must print more currency to pay back the interest and roll continued deficits into larger debt issuance, thus reducing the purchasing power of their domestic currencies. This is driving flows into real assets, with gold the largest beneficiary, but also supporting associated precious and even base metals.

US Government debt x 30 yr interest rate showing implied interest burden

Source: Bloomberg

Silver

Silver's recent volatility can only be described as unprecedented. It rose 140% from the end of November 2025 through to mid-January 2026, with a 68% rise in January alone, before experiencing a sharp reversal at the time of writing. Whilst these moves are exciting, they are also unsustainable, and a sharp reversal was certainly expected. However, all considered, silver is still showing gains for the year to date despite the pull back, but the path from here is less certain and remains heavily dependent on flows from China.

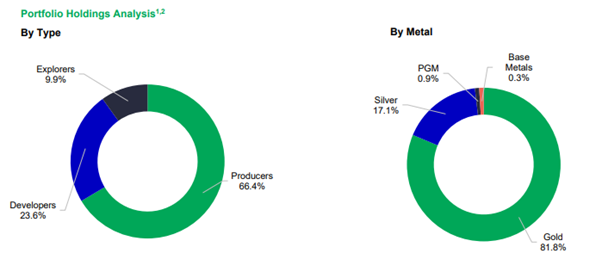

Whilst silver has shown this volatility and outperformance, we have found it interesting that that the silver miners have shown minimal outperformance relative to their gold peers despite silver's 100% outperformance. This has been a primary driver of adding more silver exposure to 17.1% by year end, as we felt it gives upside optionality for a catch up and downside protection on a pullback of silver.

The volatility in silver has been heightened by speculative retail flows, with added impacts from leveraged silver ETF's, the largest of which the 2x levered silver ETF (AGQ) saw the drawdown in silver force further liquidations in the market.

Our preference has been for the silver developers, with three companies standing out as having world class projects, that trade at a meaningful discount to NAV and imply a far lower silver price than current spot. These are namely Abra Silver, Vizsla Silver and Highland Silver, which have shown materially lower volatility than the underlying metal.

Whilst the move in silver is hard to justify, there are fundamental drivers beyond the clear speculative flows. Silver really took off following the Chinese including it in strategic metals that need licences for exports and inversely to initial logic saw the Chinese silver price trade at a steady premium of up to $30/oz in January. China runs ~70% of the global silver smelting so thus controls the majority of the silver produced globally at that bottleneck of the supply chain. Silver has been undersupplied for 4 years, with demand of 1.2bn oz vs 1bn oz of production. Chinese stocks are low in a metal that is critical in industries in which Chinese policy is focused on growth, such as solar power, EV's, chips, wind power and other high-end electronics. The majority of global silver is produced as a byproduct of polymetallic mines, thus higher silver price does little to incentivise production growth.

Outlook

After strong precious metal price action in January before pulling back, the trust has reduced gearing to a neutral level of 3.0%. At the time of writing, gold has pulled back to approximately $4,700/oz from $5,278/oz at the end of February. This followed the start of the US led attacks on Iran and the subsequent closure of the Strait of Hormuz through which 20% of the world's oil transits. This has pushed the oil price up from $73/bbl at the end of February to $110/bbl. This has pushed up central banks interest rate expectations as a result of anticipated inflationary pressures, which is part of the reason for this weakness month to date. Further to this we believe gold has displayed its role as an insurance asset, meaning during times of stress it is often initially sold due to its high liquidity, noting those holding it are likely sat on material gains. This dynamic has been seen in prior times of stress such as the 2008 GFC or Covid in 2020, when gold initially sold off 15-25%, before performing strongly in the following 12 months.

The duration of the closure of the strait is hugely significant for the oil price and thus the global economy and with it precious metals. Many sector specialists and commentators, we included, believe a loss of this magnitude justifies a much higher oil price, with an excess of $200/bbl possible. This could prove hugely inflationary for the global economy whilst weighing on growth, a term known as stagflation. Historically this has been a very supportive environment for the gold price. Even with the recently announced ceasefire, it could take months to ramp back up closed Middle Eastern oil fields, whilst the world has already lost >300M bbls of oil supply that would ultimately need to be restocked tightening future markets.

Most of the drivers in 2025 remain and in many cases are stronger now. Even with this pullback there are still good metal prices for the miners, and they will be making strong cashflows at these levels. We have reduced exposure to those miners we believe most exposed to higher oil prices, but ultimately given the high margin levels the miners currently achieve, higher oil prices are less impactful than if margins were tighter. That said, the market remains highly wary of the miners' costs eroding margins and this cost creep could be penalised in excess of the actual feed through to margin erosion.

We expect Central Banks to remain meaningful buyers of gold given the macro backdrop, although some may become forced sellers to fund energy subsidies or military spend, we believe the trend remains to additions. Higher interest rates could further increase the interest burden on excessive global government debt levels, which should leave gold remaining an important reserve asset against a deteriorating quality of the world's largest 'risk free asset' in US treasuries. We await to see the actions of the recently announced chairman of the Federal Reserve, Kevin Warsh. Currently viewed in the market as a hawk (keeps rates high to battle inflation) much of his commentary appears more dovish (pre lower rates and growth). The interest rate path going forward will be material for the dollar and US treasuries, with lower rates seen as good for precious and higher as negative.

Trust positioning

The trust has increased its weighting to developers over producers in the expectation of more M&A in 2026.

Stocks

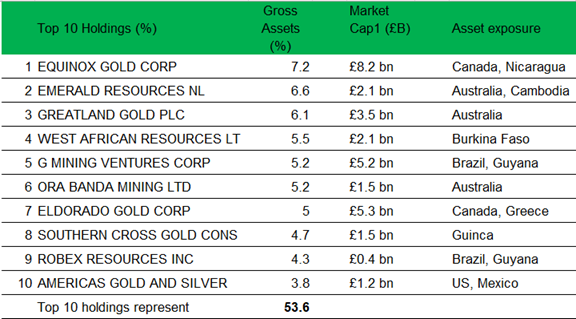

Top 10 at 31 December 2025; market caps at 31 December 2025

The trust remains geographically diverse and weighted to producers with development assets for growth offering catalysts through 2026 as they transition to production. Below these is a weighting tilted to high quality development projects.

The higher gold and silver price are leading to stronger cash generation from the sector, with many mid tiers seeing further strengthening of their balance sheets. Dividends and buybacks should increase through the year, but after years of underinvesting in their organic pipelines we believe that acquiring other single asset producers or late-stage developers will look increasingly accretive. The developers especially trade at a notable discount to producing, enhancing the accretive benefit, but should also provide some valuation protection if we see a pull back in precious metal prices.

Gold developers such as Southern Cross, Osisko Development, Goliath Resources, Liberty Gold, Collective Mining and Goldsky Resources already have 5M oz's of gold or potential to get that level. We have already seen names like Reunion Gold, Robex Resources, New Gold and Calibre Mining taken out in 2025.

In December we added to our weighting in silver developers, as they materially lagged the increase in silver and the silver miners more broadly, thus providing upside if the silver price holds and protection if it pulls back. We believe names such as Abra Silver, Vizsla Silver, Highland Silver and Dolly Varden are all M&A targets from larger peers. With limited silver projects of this scale there is a higher potential for a competitive bid process that could see a materially higher sale price given the large discount they currently trade at compared to producing peers and the limited number of projects of this true tier 1 silver scale.

Keith Watson and Robert Crayfourd

New City Investment Managers

Investment Manager

10 April 2026

Enquiries

| |

Manulife | CQS Investment Management Craig Cleland

| +44 (0) 20 7201 5368 |

Cavendish Capital Markets Limited Robert Peel (Corporate Finance) Daniel Balabanoff / Pauline Tribe (Sales)

| +44 (0) 20 7908 6000 +44 (0) 20 7720 0500 |

Apex Fund and Corporate Services (Guernsey) Limited James Taylor

| +44 (0) 203 5303 600 |

Tavistock Jos Simson / Gareth Tredway / Eliza Logan | +44 (0) 20 7920 3150 |

About Golden Prospect Precious Metals

Golden Prospect Precious Metals Limited is a closed-ended investment company incorporated with limited liability in Guernsey on 16 October 2006. The Company's investment objective is to provide Shareholders with capital growth from a portfolio of companies involved in the precious metals

mining sector.

For the latest factsheet and other information, click here.

Related Shares:

Golden Pros