28th Aug 2025 11:11

Greatland Resources Limited

Greatland Resources Limited

W: https://greatland.com.au

: x.com/greatlandgold

: x.com/greatlandgold

Correction: This announcement replaces the version published on 28/08/2025. The only changes made are formatting corrections. No substantive amendments have been made to the content of the announcement

NEWS RELEASE | 28 August 2025

Unaudited Preliminary FY25 Final Report

Year Ended 30 June 2025

THIS ANNOUNCEMENT CONTAINS INSIDE INFORMATION AS STIPULATED UNDER THE UK MARKET ABUSE REGULATIONS. ON PUBLICATION OF THIS ANNOUNCEMENT VIA A REGULATORY INFORMATION SERVICE, THIS INFORMATION IS CONSIDERED TO BE IN THE PUBLIC DOMAIN.

Greatland Resources Limited (the Company or Greatland) (ASX: GGP, AIM:GGP) has today lodged its unaudited preliminary full-year final report for year ended 30 June 2025 (FY2025).

Highlights:

Renewed safety focus at Telfer generating improved outcomes

· Total recordable injury frequency rate improved to 6.0 at 30 June 2025 (14.1 at 31 Dec 2024)

· Integration of Telfer operation under Greatland ownership completed efficiently and to plan

Significant cash generation from just seven months of operations in FY2025

· Revenue from customer contracts of $961.3 million at an average achieved gold price of $4,785 per ounce

· Net cash flow from operating activities of $601.1 million

· Segment earnings before interest, tax, depreciation and amortisation of $526.7 million

· Net profit before tax of $441.9 million reflecting high margin production from Telfer

· Net profit after tax of $337.3 million

Strong foundation set for FY2026 plans across Telfer and Havieron

· Cash and cash equivalents of $574.7 million at 30 June 2025

· Nil debt at 30 June with significant liquidity available

· Full exposure to the current spot gold and copper prices

Commenting on the FY2025 unaudited results, Greatland Managing Director Shaun Day said:

"Producing such a strong set of financial results from the first seven months of ownership of Telfer is a great credit to the significant efforts of our team. Our focus continues to be on the delivery of our FY2026 operational plan and progressing the growth opportunities at Haverion and Telfer."

This announcement is approved for release by Shaun Day, Greatland Managing Director.

Contact

For further information, please contact:

Greatland Gold plc

Shaun Day, Managing Director | Rowan Krasnoff, Chief Development Officer

Nominated Advisor

SPARK Advisory Partners

Andrew Emmott / James Keeshan / Neil Baldwin | +44 203 368 3550

Corporate Brokers

Canaccord Genuity | James Asensio / George Grainger | +44 207 523 8000

SI Capital Limited | Nick Emerson / Sam Lomanto | +44 148 341 3500

Media Relations

UK - Gracechurch Group | Harry Chathli / Alexis Gore / Henry Gamble | +44 204 582 3500

Australia - Fivemark Partners | Michael Vaughan | +61 422 602 720

About Greatland

Greatland is a gold and copper mining company listed on the Australian Securities Exchange and London Stock Exchange's AIM Market (ASX:GGP and AIM:GGP) and operates its business from Western Australia.

The Greatland portfolio includes the 100% owned Telfer mine, the adjacent 100% owned brownfield world-class Havieron gold-copper development project, and a significant exploration portfolio within the surrounding region. The combination of Telfer and Havieron provides for a substantial and long life gold-copper operation in the Paterson Province in the East Pilbara region of Western Australia.

Unaudited Preliminary Final Report - Year Ended 30 June 2025

Greatland Resources Limited (ASX/AIM: GGP) (the Company or Greatland) reports its 30 June 2025 full year financial information in accordance with ASX Listing Rule 4.3A. These unaudited results are prepared in accordance with Australian Accounting Standards. Amounts presented are in Australian dollars (AUD), except as otherwise noted.

KEY INFORMATION | 30 June 2025 $'000 | 30 June 2024 $'000 | Change $'000 | Change % |

Revenue from contracts with customers | 961,300 | - | 961,300 | 100% |

Profit / (loss) from ordinary activities after tax attributable to members | 337,260 | (28,561) | 365,821 | 1,281% |

Net profit / (loss) for the period attributable to members | 337,260 | (28,561) | 365,821 | 1,281% |

Net tangible assets per securities | 3.09 | 0.03 | 3.06 | 10,200% |

EXPLANATION OF RESULTS

Reorganisation and admission of the Company to ASX and AIM

Greatland Resources Limited (the Company or Greatland) became the 100% holding company of Greatland Gold plc and its subsidiaries on 20 June 2025, following the implementation of a shareholder approved and court sanctioned members' scheme of arrangement under the Companies Act 2006 (UK), through which shareholders of Greatland Gold plc were issued shares in the Company in exchange for their shares in Greatland Gold plc (the Reorganisation). As a result of the Reorganisation, on 20 June 2025 the Company gained control over each of the entities listed in the 'Details of entities over which control has been gained or lost' section below (the Group).

Prior to the Reorganisation, Greatland Gold plc was the parent company of the Group. Prior period financial information contained in this report represents the consolidated historical financial information for Greatland Gold plc.

On 23 June 2025, following completion of the Reorganisation, the Company's shares were admitted to the Official List of the Australian Securities Exchange (ASX) and to trading on the London Stock Exchange's AIM Market (AIM).

Acquisition

On 4 December 2024, the Greatland group of companies (held by Greatland Gold plc as the then ultimate holding company) completed the acquisition of 100% ownership of the producing Telfer gold-copper mine (Telfer), a 70% ownership interest in the Havieron gold-copper project (Havieron) (consolidating Greatland's ownership of Havieron to 100%), and other related interests in assets in the Paterson region of Western Australia (the Acquisition) from certain Newmont Corporation subsidiaries (Newmont). The Acquisition transformed the Greatland group from an exploration and development group whose principal asset was its 30% non-managing joint venture interest in Havieron, into a substantial Australian gold-copper producer.

Operating and financial results

The Group's key focuses for the year ended 30 June 2025 were:

· negotiation, execution and completion of the Acquisition, and associated equity and debt financing;

· integration and operation of the assets acquired through the Acquisition; and

· the Reorganisation and admission of the Company to ASX and AIM.

Revenue from customer contracts of $961.3 million consisted of the sale of gold and copper produced from the Telfer mine during the Group's ownership from 4 December 2024 to 30 June 2025, approximately a seven-month period. The increase in revenue from the prior year (nil) is due to the acquisition and operation of the Telfer mine which transformed the Group from a non-revenue generating exploration and development group into a substantial producer of gold and copper. Consequently, the Group generated a significant maiden profit before tax of $441.9 million.

As at 30 June 2025, the Group had cash and cash equivalents of $574.7 million (30 June 2024: $9.2 million) and nil borrowings (30 June 2024: $79.1 million). During the period, the Group generated $601.1 million net cash flows from operating activities.

DIVIDEND INFORMATION

No dividends have been paid or declared since the start of the financial year and it is not proposed to pay any dividends in respect of the full year.

ADDITIONAL INFORMATION

Requirement | Title |

|

A statement of comprehensive income | Consolidated Statement of Comprehensive Income |

|

A statement of financial position | Consolidated Statement of Financial Position |

|

A statement of retained earnings | Consolidated Statement of Changes in Equity |

|

A statement of cash flows | Consolidated Statement of Cash Flows |

|

Earnings per share | Consolidated Statement of Comprehensive Income |

|

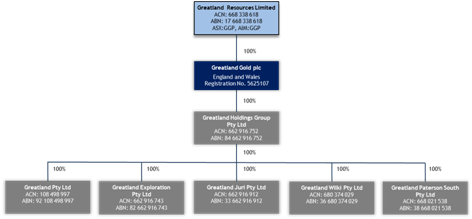

DETAILS OF ENTITIES OVER WHICH CONTROL HAS BEEN GAINED OR LOST

As a result of the Reorganisation, Greatland, through its wholly-owned subsidiary, owns 100% interest in the Group's assets, and the Group structure is set out below:

DETAILS OF ASSOCIATED AND JOINT VENTURE ENTITIES

The Group has no associated or joint venture entities.

STATUS OF AUDIT

The Company's financial statements are in the process of being audited. The Company expects to release its audited financial statements and FY25 Annual Report during September 2025. The Company does not anticipate any material variance from the unaudited results provided in this Preliminary Final Report.

FINANCIAL AND OPERATIONAL PERFOMANCE SUMMARY

Greatland adopts a combination of International Financial Reporting Standards (IFRS) and non-IFRS financial measures to assess performance. This includes EBITDA and net debt which are used to assist internal and external stakeholders to better understand the financial performance of the Group and its operations.

Review of results (unaudited)

Financial Overview | 30 June 2025 $'000 | 30 June 2024 $'000 | Change $'000 |

Revenue from contracts with customers | 961,300 | - | 961,300 |

Segment EBITDA | 526,6671 | (8,086) | 534,753 |

Net profit / (loss) after tax | 337,260 | (28,561) | 365,821 |

Cash flows from operating activities | 601,114 | (21,680) | 622,794 |

Cash and cash equivalents | 574,663 | 9,168 | 565,495 |

Debt | - | (79,124) | 79,124 |

Basic earnings per share (cents) | 63.57 | (11.23) | 74.80 |

1 Segment EBITDA (as described in Note 3 Segment information) is calculated as revenue less cost of sales excluding depreciation and amortisation. Cost of sales of $461.4 million includes change in inventories of $39.4 million, mainly related to stockpiles acquired as part of the Telfer acquisition, and depreciation and amortisation of $40.5 million both of which are excluded from in all-in sustaining cost (AISC).

HEALTH, SAFETY AND WELLBEING

Greatland promotes an environment where safety is one of our key priorities. Greatland is focused on delivering safety leadership at all levels of the business to strengthen the culture of awareness and zero harm. Greatland maintains an effective approach to the health and safety of its employees, and the communities in which we operate: the identification and control of hazards and ongoing management of the risk associated with them.

Since Greatland completed the Acquisition, the continued focus on visible field leadership (providing leaders with the right tools and information to lead by example and timely feedback and support) has seen significant improvements in Telfer's recordable injuries, with the total recordable injury frequency rate (TRIFR) improving from 14.1 at 31 December 2024 to 6.0 at 30 June 2025. There were no fatalities at the Group's projects during the year.

CORPORATE

Acquisition

Greatland Gold plc announced on 10 September 2024 that it had entered into a binding agreement with Newmont in respect of the Acquisition to acquire 100% ownership of the Telfer mine, 70% ownership of the Havieron project (consolidating the Group's ownership of Havieron to 100%), and other related interests in assets in the Paterson region. The Group completed the Acquisition on 4 December 2024.

In connection with the Acquisition, a fully underwritten institutional placing to raise US$325 million ($481.0 million) and a retail offer to raise US$8.8 million ($12.2 million) (together, the Acquisition Fundraising) were successfully completed by Greatland Gold plc (both gross before associated fees). On 30 September 2024, a general meeting of the shareholders of Greatland Gold plc approved the Acquisition and the associated equity fundraising.

At Acquisition completion, the Group paid the upfront cash consideration of US$165.1 million ($256.7 million) (comprising of US$155.1 million cash consideration and estimated purchase price adjustments) and US$167.5 million consideration in the form of 2,669,182,291 Greatland Gold plc ordinary shares issued to Newmont, representing approximately 20.4% of Greatland Gold plc shares then on issue. The fair value of the shares issued at Acquisition completion was $394.3 million based on the Greatland Gold plc share price on 4 December 2024.

At Acquisition completion, the Group also repaid debt of US$52.4 million ($81.5 million), the entire outstanding balance of the Havieron joint venture loan to Newmont, which was subsequently terminated.

During the year Greatland paid a further US$15.4 million ($23.9 million) in Acquisition purchase price adjustments to Newmont. Greatland expects to pay to Newmont on a deferred basis up to a maximum of US$100 million in deferred cash consideration, which may be payable to Newmont on the first five years of Havieron gold production, through a 50% price upside participation by Newmont above a US$1,850/oz hurdle gold price, subject to an annual cap of US$50 million and aggregate cap of US$100 million. The fair value of the deferred consideration has been estimated at $115.6 million at 30 June 2025.

Debt facilities

During the year the Group executed:

· a facility agreement with ANZ, HSBC and ING (together, the Banking Syndicate) in respect of a $75 million working capital facility (Working Capital Facility) and a $25 million contingent instrument facility (Contingent Instrument Facility); and

· a non-binding letter of support with the Banking Syndicate, in respect of $775 million in proposed banking facilities, including $750 million in facilities that would be available to fund capital to complete the planned development of Havieron.

At 30 June 2025, the Working Capital Facility remained undrawn and $8.5 million remained available under the Contingent Instrument Facility.

Greatland intends to finalise debt financing arrangements for the development of Havieron following completion of the Havieron Feasibility Study which is targeted in the December 2025 quarter.

During the year Greatland retained full upside exposure to the gold price, while implementing some downside protection through the purchase of gold put options. The Group purchased AUD denominated gold put options from the Banking Syndicate in respect of 300,000oz of gold, with a series of expiry dates through calendar year 2025 (CY25) and calendar year 2026 (CY26). At 30 June 2025, the following put options remain in place:

Quarter End Date (Expiry) | Gold Volumes Under Options (oz) | Average blended strike price (A$ per oz) |

30-Sep-2025 | 38,910 | 3,905 |

31-Dec-2025 | 30,792 | 3,905 |

31-Mar-2026 | 37,502 | 4,200 |

30-Jun-2026 | 37,502 | 4,200 |

30-Sep-2026 | 37,502 | 4,200 |

31-Dec-2026 | 37,498 | 4,200 |

Total | 219,706 | 4,106 |

The put options establish a price level at which the Group has the right, but not the obligation, to sell gold, therefore providing a minimum downside price protection for the protected ounces while retaining full upside exposure to the gold price across 100% of Telfer production volumes.

In September 2023 Greatland entered into a $50 million working capital facility with cornerstone shareholder, Wyloo Consolidated Investments Pty Ltd. During the year $7 million was drawn down under the facility, and then subsequently repaid from the proceeds of the equity raising described above and the facility terminated.

Reorganisation and ASX initial public offer and listing

In connection with the Acquisition, in September 2024 Greatland Gold plc announced its intention to undertake a listing of the post-Acquisition Group on the ASX within approximately six months from Acquisition completion.

Consistent with this, the Group successfully completed two major corporate initiatives during June 2025, being the Reorganisation through which Greatland became the sole shareholder of Greatland Gold plc and parent of the Group, and Greatland's ASX initial public offer (IPO) and listing.

The ASX IPO was strongly supported, with an oversubscribed $490 million offer at an offer price of $6.60 per share. The offer comprised a $50 million primary issuance by Greatland and a $440 million secondary sell down by Bright SaleCo Limited, a special purpose vehicle incorporated to facilitate the sale under the IPO of 50% of Newmont's shares in Greatland that were originally received in the form of shares in Greatland Gold plc as part of the consideration under the Acquisition. A separate offer to UK resident retail investors was also oversubscribed and successfully completed, raising a further ~$14.0 million in gross proceeds. On 23 June 2025, Greatland was admitted to the ASX and AIM, with trading on ASX commencing on 24 June 2025.

OPERATIONS

Assets

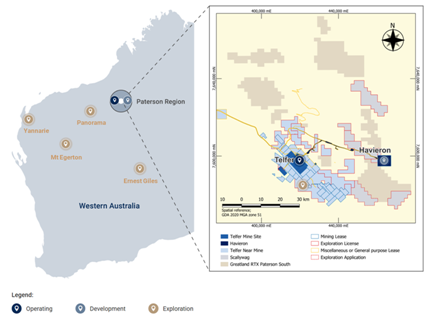

The Greatland portfolio includes the 100% owned Telfer gold-copper mine, the adjacent 100% owned world class Havieron gold-copper project (under development), and a significant exploration portfolio within the surrounding Paterson Province and broader Western Australia.

Figure 1: Map of Greatland's assets

Vision and Strategy

Greatland aspires to become a profitable multi-mine resources company by focusing on the responsible and sustainable discovery, development, extraction, processing and sale of precious and base metals.

Greatland's strategy is to renew and develop an integrated Telfer-Havieron mining and processing operation, with the intention of creating a generational gold-copper mining complex. To help achieve this, Greatland is focused on the following:

1. Continuing to operate Telfer profitably;

2. Extending Telfer's mine life;

3. Developing and optimising Havieron through to production; and

4. Leveraging the Telfer infrastructure to enable a 'hub and spoke' strategy in the Paterson region.

Greatland has assembled a highly experienced team that is committed to delivering on its strategy. The senior team is supported by a Board with significant expertise and experience in the global resources sector. Greatland's leadership team has a strong track record and is strongly aligned with the Company's shareholders.

Telfer, Western Australia

Telfer is an operating gold-copper mine located in the Paterson Province of Western Australia. Telfer first produced gold in 1977 and has produced more than 15Moz of gold to date. Telfer is a fly-in fly-out mine with both open pit and underground mining operations, an established workforce and significant infrastructure. Gold and copper are produced by a large processing facility comprising dual 10Mtpa capacity trains, totalling 20Mtpa in nominal capacity, that produces gold a copper-gold concentrate, gold doré and gold middlings high-grade concentrate. Ore from Telfer is currently being mined from the West Dome open pit and the Telfer underground. Telfer's strategic positioning in the Paterson region, with existing infrastructure and processing capacity, de-risks, expedites and reduces the cost of completing Havieron's development. As the only operating processing infrastructure in the Paterson region with surplus capacity, Telfer enables a 'hub and spoke' strategy to incorporate accretive regional opportunities. |

Operations

The Group acquired 100% ownership of Telfer from Newmont on 4 December 2024, on completion of Acquisition.

In FY25 during the period of Greatland's ownership from 4 December 2024 to 30 June 2025 (approximately seven months), Greatland:1

· produced 198,319oz of gold and 8,429t of copper, at an All-In-Sustaining-Cost (net of by-product credits and excluding inventory movements which mainly relate to stockpiles acquired through the Acquisition) (AISC) of $1,849 per ounce of gold;

· sold 180,570oz of gold and 7,445t of copper at average realised prices of $4,785/oz gold and $12,923/t copper (both after adjustments for treatment and refining charges and payability deductions), for total revenue from contracts with customers of $961.3 million;

· processed 10.97Mt of material, utilising both processing trains, with an average grade of 0.65g/t gold and 0.10% copper, and recoveries of 84.2% for gold and 79.2% for copper;

· mined 4.82Mt of ore at the Telfer West Dome open pit (total material mined of 10.46Mt) and 0.67Mt of ore at the Telfer underground.

A key driver of the strong FY25 operational performance was significant improvement in recoveries. FY25 gold recovery of 84.2% was the highest annual gold recovery achieved at Telfer since 2010, an exceptional result given the lower than historical grade processed in FY25. The improved recoveries were achieved through a focus on stable grinding and flotation plant operation, and consistent feed rates to and utilisation of the pyrite flotation and concentrate carbon-in-leach (CIL) circuits.

Through the Acquisition, Greatland acquired significant stockpiles that were mined under previous ownership of Telfer. Processing of stockpiles during FY25, together with productivity and cost improvements under Greatland's ownership, contributed to achievement of the low AISC of $1,849/oz. At 30 June 2025, estimated stockpiles at Telfer were:

· 7.0Mt run-of-mine stockpiles at 0.57g/t gold and 0.06% copper, containing 129koz gold and 4.5kt copper; and

· 20.7Mt low grade stockpiles at 0.33g/t gold and 0.04% copper, containing 220koz gold and 9.0kt copper.

Note 1 - See ASX announcement entitled "June 2025 Quarterly Activities Report" released by Greatland on ASX on 29 July 2025

Resource and Reserve

During FY25, the Group announced its inaugural Mineral Resource Estimate and Ore Reserve Estimate for Telfer2.

Greatland made significant progress in resource development during the year, completing more than 78,000 metres of resource growth and conversion drilling from 4 December 2024 to 30 June 2025. Drilling for the full FY25 focused on the following key areas:

· West Dome Underground project, where a maiden underground drilling campaign confirmed the near-mine underground opportunity;

· West Dome Open Pit Stage 2 Extension, Stage 7 Cutback and Stage 7 Extension; and

· Main Dome Underground Eastern Stockwork Corridor (ESC) and A-Reefs areas.

Greatland's CY25 drilling results are expected to inform a Telfer Mineral Resource Estimate update during the March 2026 quarter and an Ore Reserve Estimate update in the June 2026 quarter.

Note 2 - For further information, see ASX announcement entitled "Replacement Prospectus" released by Greatland on ASX on 23 June 2025

Extension

Significant progress and investments were made during the year to Telfer mine life extension opportunities.

These investments included tailings storage facility lift construction to expand tailings capacity, commencement of waste pre-stripping of the West Dome Open Pit Stage 7 extension, significantly increased underground development including at the exciting new West Dome Underground opportunity, and significantly increased resource development drilling.

In April 2025, the Group announced an extension of Telfer's mine life to the end of FY27, a significant extension from the Group's pre-Acquisition 15-month mine life to late CY25. Looking ahead, the Group is making further growth capital investments at Telfer, targeting further multi-year mine life extensions.

Continued extension of Telfer's mine life was enabled during the year with key Telfer mining leases achieved their second renewal until December 2045. Tenements M45/6, M45/7, M45/8, M45/9, M45/10, M45/11, G45/1, G45/2, G45/3, G45/4 and L45/3 were all renewed until 17 December 2045.

Havieron, Western Australia

Havieron is a world-class high grade underground gold-copper development project located approximately 45km to the east of Telfer in the Paterson province of Western Australia. The Havieron deposit was discovered by the Greatland group in 2018. It is one of the largest high-grade gold discoveries in Australia of the last 20 years and is currently the second largest undeveloped gold project by Mineral Resource in Australia. Following discovery, Havieron was advanced under an unincorporated joint venture between Greatland and Newcrest Mining Limited (2019 - 2023), and then Newmont (2023 - 2024). The Group consolidated 100% ownership of Havieron in December 2024. Havieron has a Mineral Resource Estimate (inclusive of Ore Reserve) of 131Mt at 1.67g/t gold and 0.21% copper for a total of 7.0Moz gold and 275kt copper and an Ore Reserve Estimate of 24.9Mt @ 2.98g/t gold and 0.44% copper for a total of 2.4Moz gold and 109kt copper3. The Havieron Mineral Resource Estimate is contained within a compact 650 metre strike length and is currently defined over 1,400 vertical metres. The Havieron ore body has an exceptional ounce per vertical metre profile, with the Mineral Resource estimate averaging more than 9,150 gold equivalent ounces per vertical metre through the top 300 metres of the ore body, and more than 7,900 gold equivalent ounces through the top 1,000 metres. Early works commenced in January 2021 and are advanced, including 2,110 metres of development of the underground main access decline, through 80% of the total depth to the top of the Havieron ore body. Underground development is currently paused prior to completion of the Feasibility Study. Note 3 - See ASX announcement entitled "Replacement Prospectus" released by Greatland on ASX on 23 June 2025 |

Greatland's Feasibility Study (FS) for the completion of Havieron's development is underway and targeted to be completed in the December 2025 quarter. The FS is building upon previous study work undertaken by Newcrest Mining Limited as the Havieron joint venture manager in the period from 2019 to 2023.

During the year Greatland finalised the design criteria for the FS, with the study assessing an initial mining rate of 2.8Mtpa post ramp-up, increasing to between 4.0Mtpa - 4.5Mtpa by development of a second decline, material handling system and underground crusher. This represents a significant expansion of Havieron, from the approximately 2.8Mtpa single decline truck haulage operation that was contemplated by previous study work.

The expansion case remains subject to ongoing assessment in the FS, however Greatland considers that the expanded mining rate has the potential to be highly value accretive for the following reasons:

· Telfer infrastructure has sufficient capacity to process increased Havieron ore feed;

· Planned haul road and infrastructure corridor between Telfer and Havieron does not need to be expanded to accommodate increased Havieron throughput;

· Havieron above ground site infrastructure only requires moderate expansion to accommodate increased throughput; and

· Development of the underground crusher and material handling system is expected to be largely self-funded from Havieron cash flows.

The FS will define an executable project schedule and capital expense estimate for the completion of Havieron's development, and an operating cost estimate.

While Greatland awaits the executable project schedule to be delivered as part of the FS, de-risking of the project schedule through critical path analysis is being undertaken. During the year, key early works activities included:

· Award of the early works package for two blind bore ventilation shafts, completion of design of the shafts, and completion of the design and commencement of fabrication of specialist blind bore cutter heads.

· Completed the design and tendered for supply and installation of a reinforced concrete tunnel connecting the existing decline portal to surface level, and backfill of the existing box cut, to mitigate flow of surface water to the Havieron decline during periods of rainfall.

· Progress of the environmental permitting and approvals processes with the WA Environmental Protection Authority (EPA) and the Commonwealth Department of Climate Change, Energy, the Environment and Water (DCCEEW).

Exploration

Greatland holds a significant portfolio of precious and base metals exploration projects in Western Australia, with a focus on the Paterson Province of Western Australia.

Greatland's key exploration projects are:

Paterson region

· Telfer Near Mine: 100% ownership of tenements covering over 750km2 within 30km of the Telfer processing plant. During the year, key activities included over 7,500m of reverse circulation (RC) and diamond drilling focused on near term extensions to known resources along the Telfer trend. Assay results were pending at the end of the year, with encouraging geological logging.

· Paterson South: Seven exploration tenements covering a combined area of 1,022km2, for which the Group is earning into up to a 75% interest under a farm-in and joint venture arrangement with Rio Tinto Exploration Pty Limited, a subsidiary of Rio Tinto Limited. During the year, key activities included drill testing of several targets in close proximity (within approximately 15km) from Havieron and at the Telfer lookalike Paterson dome for approximately 5,800m of RC and diamond drilling. Follow up drilling is planned in both areas targeting combined copper / gold and copper anomalies respectively.

· Scallywag: 100% ownership of six exploration tenements covering an area of approximately 334km2 located adjacent to and around Havieron. During the year, key activities included a magnetotelluric (MT) survey over the Kraken target and follow up drilling for approximately 1,080m of diamond and RC drilling in close proximity to Havieron.

Three of the Scallywag tenements and the Panorama project (a further three tenements outside the Paterson) are subject to a conditional sale agreement with Aventine Resources Pty Ltd (ACN 686 650 297) (Aventine Resources). The sale to Aventine Resources demonstrates Greatland's approach to exploration portfolio optimisation and its support of the Aventine Resources team to establish a new greenfields gold explorer in the Paterson Region.

Broader Western Australia

· Ernest Giles: 100% ownership of five exploration tenements covering an area of approximately 1,323km2 located approximately 250km north-east of Laverton in the Yilgarn region. Ernest Giles is an underexplored Archean greenstone belt which lies within the highly mineralised Yilgarn Craton, to the north of the world-class Tropicana and Gruyere gold mines. During the year, key activities included the completion of a 3D induced polarisation (IP) electrical survey over the Meadows prospect which identified multiple anomalies associated with both banded iron units (BIF) and structures within dolerites, and the planning of over 8,500m of reverse circulation (RC) and diamond drilling that commenced at the end of June 2025 and will be completed in FY26.

· Mt Egerton: 100% ownership of six exploration tenements covering an area of approximately 576km2 located approximately 230km north of Meekatharra in the Gascoyne region. During the year, key activities were negotiation of a land access agreement and preparation for on-ground reconnaissance work to commence in FY26.

Forward Looking Statements

This report includes forward looking statements and forward looking information within the meaning of securities laws of applicable jurisdictions. Forward looking statements can generally be identified by the use of words such as "may", "will", "expect", "intend", "plan", "estimate", "anticipate", "believe", "continue", "objectives", "targets", "outlook" and "guidance", or other similar words and may include, without limitation, statements regarding estimated reserves and resources, certain plans, strategies, aspirations and objectives of management, anticipated production, study or construction dates, expected costs, cash flow or production outputs and anticipated productive lives of projects and mines.

These forward looking statements involve known and unknown risks, uncertainties and other factors that may cause actual results, performance and achievements or industry results to differ materially from any future results, performance or achievements, or industry results, expressed or implied by these forward-looking statements. Relevant factors may include, but are not limited to, changes in commodity prices, foreign exchange fluctuations and general economic conditions, increased costs and demand for production inputs, the speculative nature of exploration and project development, including the risks of obtaining necessary licences and permits and diminishing quantities or grades of reserves, political and social risks, changes to the regulatory framework within which Greatland operates or may in the future operate, environmental conditions including extreme weather conditions, recruitment and retention of personnel, industrial relations issues and litigation.

Forward looking statements are based on assumptions as to the financial, market, regulatory and other relevant environments that will exist and affect Greatland's business and operations in the future. Greatland does not give any assurance that the assumptions will prove to be correct. There may be other factors that could cause actual results or events not to be as anticipated, and many events are beyond the reasonable control of Greatland. Forward looking statements in this report speak only at the date of issue. Greatland does not undertake any obligation to update or revise any of the forward looking statements or to advise of any change in assumptions on which any such statement is based.

Non-GAAP measures

Some of the financial performance measures used in this report are non-IFRS financial measures, including "all-in sustaining cost", "total cash cost", "net cash", "free cash flow", "operating cash flow", "sustaining capital" and "growth capital". These measures are presented as they are considered to provide useful information to assist investors with their evaluation of the business's underlying performance. Since the non-IFRS performance measures listed herein do not have any standardised definition prescribed by IFRS, they may not be comparable to similar measures presented by other companies. Accordingly, they are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

Competent Persons and JORC Compliance

The information in this report that relates to Ore Reserve Estimates and Mineral Resource Estimates has been extracted from the ASX announcement entitled "Replacement Prospectus" released by Greatland on ASX on 23 June 2025 (Relevant Announcement), available at https://www.greatland.com.au/investors/announcements/. The Competent Person responsible for the Ore Reserve Estimates in the Relevant Announcement is Mr Otto Richter and the Competent Person responsible for the Mineral Resource Estimates in the Relevant Announcement is Mr Michael Thomson.

Greatland confirms that it is not aware of any new information or data that materially affects the information included in the Relevant Announcement. Greatland confirms that all material assumptions and technical parameters underpinning the estimates in the Relevant Announcement continue to apply and have not materially changed. Greatland confirms that the form and context in which each Competent Person's findings are presented have not been materially modified from the Relevant Announcement.

FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2025

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME (UNAUDITED)

For the year ended 30 June 2025

| Notes | 2025 $'000 | 2024 (Restated)1 $'000 |

Revenue | 4 | 957,367 | - |

Cost of sales | 5 | (461,380) | - |

Gross profit | 495,987 | - | |

Other income / (expenses) | 7 | 30,259 | 129 |

Exploration and evaluation expenses | (9,846) | (8,086) | |

Corporate and other expenses | 6 | (41,390) | (11,317) |

Share based payment expense | 24 | (28,610) | (6,299) |

Transaction costs related to a business combination | 25 | (14,748) | (2,914) |

Transaction costs expensed in relation to ASX listing | (6,779) | - | |

Profit / (loss) before finance items and tax | 424,873 | (28,487) | |

|

|

| |

Finance income | 19 | 23,623 | 1,576 |

Finance costs | 19 | (6,593) | (1,650) |

Profit / (loss) before tax | 441,903 | (28,561) | |

Income tax expense | 8 | (104,643) | - |

Profit / (loss) for the year | 337,260 | (28,561) | |

Other comprehensive income / (loss): Items to be reclassified to profit / (loss) in subsequent periods: | |||

Net foreign exchange differences on translation of foreign operations, net of tax | 4,880 | 26 | |

Net change in fair value of cash flow hedges taken to equity, net of tax | (9,635) | - | |

Total comprehensive income / (loss) for the year attributable to equity holders of Greatland Resources Limited | 332,505 | (28,535) | |

Profit / (loss) for the year attributable to the ordinary equity holders of Greatland Resources Limited: | |||

Basic earnings / (losses) per share (cents) | 9 | 63.57 | (11.23) |

Diluted earnings / (losses) per share (cents) | 9 | 63.14 | (11.23) |

1 The reporting currency of the Group was changed from sterling to Australian dollars during the financial year. Refer to Note 2(a) for further details.

The above Statement should be read in conjunction with the accompanying notes.

CONSOLIDATED STATEMENT OF FINANCIAL POSITION (UNAUDITED)

As at 30 June 2025

| Notes | 30 June 2025 $'000 | 30 June 2024 (Restated)1 $'000 | 1 July 2023 (Restated)1 $'000 |

ASSETS |

| |||

Cash and cash equivalents | 16 | 574,663 | 9,168 | 59,332 |

Trade and other receivables | 10 | 34,162 | 262 | 222 |

Inventories | 11 | 200,306 | - | - |

Derivative financial instruments | 20 | 605 | - | - |

Other current assets | 8,396 | 4,082 | 24,741 | |

Total current assets | 818,132 | 13,512 | 84,295 | |

Inventories | 11 | 39,956 | - | - |

Exploration and evaluation assets | 12 | 127,256 | 452 | 503 |

Property, plant and equipment | 13 | 1,098,340 | 157,519 | 115,109 |

Financial assets held at fair value through profit and loss | 21 | 28,441 | 75 | 168 |

Derivative financial instruments | 20 | 1,695 | - | - |

Deferred tax assets | 8 | - | - | - |

Other non-current assets | 1,556 | - | - | |

Total non-current assets |

| 1,297,244 | 158,046 | 115,780 |

TOTAL ASSETS |

| 2,115,376 | 171,558 | 200,075 |

| ||||

LIABILITIES | ||||

Trade and other payables | 14 | 212,706 | 9,903 | 16,212 |

Lease liabilities | 18 | 14,301 | 253 | 244 |

Current tax liabilities | 8 | 76,112 | - | - |

Provisions | 15 | 11,837 | 8 | 354 |

Total current liabilities |

| 314,956 | 10,164 | 16,810 |

Deferred contingent consideration | 25 | 115,579 | - | - |

Borrowings | 17 | - | 79,124 | 79,052 |

Deferred tax liabilities | 8 | 41,451 | - | - |

Lease liabilities | 18 | 17,268 | 335 | 542 |

Provisions | 15 | 286,011 | 3,834 | 3,714 |

Total non-current liabilities |

| 460,309 | 83,293 | 83,308 |

TOTAL LIABILITIES |

| 775,265 | 93,457 | 100,118 |

NET ASSETS |

| 1,340,111 | 78,101 | 99,957 |

| ||||

EQUITY | ||||

Share capital | 23 | 1,170,140 | 183,712 | 183,332 |

Other reserves | (24,646) | 37,032 | 30,772 | |

Retained earnings / (accumulated losses) | 194,617 | (142,643) | (114,147) | |

TOTAL EQUITY | 1,340,111 | 78,101 | 99,957 |

1The reporting currency of the Group was changed from sterling to Australian dollars during the financial year. Refer to Note 2(a) for further details.

The above Statement should be read in conjunction with the accompanying notes.

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY (UNAUDITED)

For the year ended 30 June 2025

|

Notes | Share capital $'000 | Reorg- anisation Reserve $'000 | Cash flow hedge reserve $'000 | Foreign currency translation reserve $'000 | Share based payment reserve $'000 | Capital return reserve2 $'000 | Retained earnings/ (accumulated losses) $'000 | Total equity $'000 |

As at 1 July 2023 (Restated)1 |

| 183,332 | - | - | 11,414 | 19,358 | - | (114,147) | 99,957 |

Profit / (loss) for the year | - | - | - | - | - | - | (28,561) | (28,561) | |

Other comprehensive income / (loss) | - | - | - | (39) | - | - | 65 | 26 | |

Total comprehensive income / (loss) |

| - | - | - | (39) | - | - | (28,496) | (28,535) |

Transactions with owners: |

|

|

|

|

|

|

|

|

|

Share based payments | 24 | - | - | - | - | 6,299 | - | - | 6,299 |

Contributions of equity, net of transaction costs | 23 | 380 | - | - | - | - | - | - | 380 |

As at 30 June 2024 (Restated)1 |

| 183,712 | - | - | 11,375 | 25,657 | - | (142,643) | 78,101 |

Profit / (loss) for the year | - | - | - | - | - | - | 337,260 | 337,260 | |

Other comprehensive income / (loss) | - | - | (9,635) | 4,880 | - | - | - | (4,755) | |

Total comprehensive income / (loss) |

| - | - | (9,635) | 4,880 | - | - | 337,260 | 332,505 |

Transactions with owners: |

|

|

|

|

|

|

|

|

|

Share based payments | 24 | - | - | - | - | 11,331 | - | - | 11,331 |

Surrender of options | 23 | 34,210 | - | - | - | (24,168) | (26,006) | - | (15,964) |

Capital reorganisation | 23 | 18,080 | (18,080) | - | - | - | - | - | - |

Contributions of equity, net of transaction costs | 23 | 934,138 | - | - | - | - | - | - | 934,138 |

As at 30 June 2025 |

| 1,170,140 | (18,080) | (9,635) | 16,255 | 12,820 | (26,006) | 194,617 | 1,340,111 |

1The reporting currency of the Group was changed from sterling to Australian dollars during the financial year. Refer to Note 2(a) for further details.

2.As a result of the surrender options, capital returned in excess of the originally recognised share based payment expense has been disclosed in a capital return reserve. Refer to Note 23 Share capital for further information.

The above Statement should be read in conjunction with the accompanying notes.

CONSOLIDATED STATEMENT OF CASH FLOWS (UNAUDITED)

For the year ended 30 June 2025

| Notes | 2025 $'000 | 2024 (Restated)1 $'000 |

Cash flows from operating activities | |||

Profit/ (loss) before tax | 441,903 | (28,561) | |

Adjustments for: | |||

Share based payment expense | 24 | 28,610 | 6,299 |

Depreciation and amortisation | 13 | 50,746 | 310 |

Other non-cash items | (26,326) | 70 | |

Finance costs | 19 | 6,593 | 1,650 |

Finance income | 19 | (23,623) | (1,576) |

Movements in assets and liabilities: | |||

Other current and non-current assets | (5,867) | (80) | |

Inventories | 40,655 | - | |

Trade and other receivables | (29,207) | 22 | |

Trade and other payables | 142,816 | (1,648) | |

Provisions and other liabilities | (16,309) | 80 | |

Interest received | 9,162 | 1,754 | |

Interest paid | (4,949) | - | |

Purchase of gold put premiums | (13,090) | - | |

Net cash flows from operating activities | 601,114 | (21,680) | |

Cash flows from investing activities | |||

Payments for mine development and fixed assets | 13 | (160,265) | (26,688) |

Exploration expenditure capitalised | 12 | (8,986) | - |

Cash consideration for Telfer-Havieron acquisition | 25 | (280,659) | - |

Transaction costs related to asset acquisition | 25 | (12,561) | |

Net cash flows from investing activities | (462,471) | (26,688) | |

Cash flows from financing activities | |||

Proceeds from issue of shares | 23 | 557,199 | 380 |

Transaction costs from issue of shares | 23 | (17,366) | - |

Proceeds from borrowings | 17 | 7,000 | - |

Repayment of borrowings | 17 | (87,683) | - |

Repayment of lease principal | 18 | (10,323) | (248) |

Payments to directors and employees for surrender of options | 23 | (34,210) | - |

Payments for prepaid borrowing costs for debt | - | (1,895) | |

Net cash flows from financing activities | 414,617 | (1,763) | |

Net increase/ (decrease) in cash and cash equivalents | 553,260 | (50,131) | |

Cash and cash equivalents at the beginning of the period | 9,168 | 59,332 | |

Effect of exchange rate differences on cash and cash equivalents | 12,235 | (33) | |

Cash and cash equivalents at the end of the year | 16 | 574,663 | 9,168 |

1The reporting currency of the Group was changed from sterling to Australian dollars during the financial year. Refer to Note 2(a) for further details.

The above Statement should be read in conjunction with the accompanying notes.

NOTES TO THE FINANCIAL STATEMENTS (UNAUDITED) | ||||

Principal accounting policies | ||||

1. | Corporate information | |||

2. | Basis of preparation | |||

Financial performance | ||||

3. | Segment information | |||

4. | Revenue | |||

5. | Cost of sales | |||

6. | Corporate and other expenses | |||

7. | Other income and expenses | |||

8. | Income tax | |||

9. | Earnings per share | |||

Operating assets and liabilities | ||||

10. | Trade and other receivables | |||

11. | Inventories | |||

12. | Exploration and evaluation assets | |||

13. | Property, plant and equipment | |||

14. | Trade and other payables | |||

15. | Provisions | |||

Capital structure and financing | ||||

16. | Cash and cash equivalents | |||

17. | Borrowings | |||

18. | Lease liability | |||

19. | Finance income and finance costs | |||

20. | Derivative financial instruments | |||

21. | Financial assets fair valued through profit and loss | |||

22. | Financial risk management | |||

23. | Share capital | |||

Other notes | ||||

24. | Share based payments | |||

25. | Acquisition of Havieron project and Telfer gold-copper mine | |||

26. | Subsequent events | |||

| ||||

NOTES TO THE FINANCIAL STATEMENTS (UNAUDITED)

FOR THE YEAR ENDED 30 JUNE 2025

PRINCIPAL ACCOUNTING POLICIES

1 CORPORATE INFORMATION

Greatland Resources Limited (Greatland or the Company) is a for profit company limited by shares, domiciled and incorporated in Australia, whose shares are traded on the Australian Securities Exchange (ASX) (ASX:GGP) and the LSE AIM (AIM:GGP). Greatland's shares commenced trading on the ASX from 24 June 2025, and commenced trading on the LSE AIM on 23 June 2025.

The registered office of the Company is Level 2, 502 Hay Street, Subiaco, WA, 6008.

The nature of operations and principal activities of the Group are exploration, mine development, mine operations and the sale of gold and gold-copper concentrate.

2 BASIS OF PREPARATION

The financial report is a general purpose financial report which:

· has been prepared in accordance with Australian Accounting Standards (AAS) and other authoritative pronouncements of the Australian Accounting Standards Board (AASB) and the Corporations Act 2001 (Cth);

· complies with International Financial Reporting Standards (IFRS) and interpretations adopted by the International Accounting Standards Board (IASB);

· has been prepared on a historical cost basis except for certain financial instruments which have been measured at fair value through the Consolidated Statement of Comprehensive Income;

· is presented in Australian dollars with all values rounded to the nearest thousand dollars ($'000) unless otherwise stated, in accordance with ASIC Corporations (Rounding in Financial / Directors' Reports) Instrument 2016/191; and

· does not early adopt AAS and Interpretations that have been issued or amended but are not yet effective.

a) Change in reporting currency

Effective 24 June 2025, post ASX listing, the reporting currency of the Group was changed from sterling (£) to Australian dollars ($). The change in presentation currency provides investor and other stakeholders with greater transparency in relation to the Group's performance as it better reflects the primary economic environment in which the Group operates.

The amounts for prior periods have been translated into Australian dollars using the methods outlined below:

· Consolidated Statement of Comprehensive Income and Consolidated Statement of Cash Flows have been translated into Australian dollars using average foreign currency rates prevailing from the relevant year;

· assets and liabilities in the Consolidated Statement of Financial Position have been translated into Australian dollars at the closing foreign currency rate on the relevant balance sheet date;

· equity section of the Consolidated Statement of Financial Position, including retained earnings, share capital and other reserves, has been translated into Australian dollars on the basis that Greatland had always reported in Australian dollars; and

· earnings / (losses) per share has been restated to Australian dollars to reflect the change in presentation currency.

b) Significant changes in the state of affairs

Greatland was incorporated on 30 May 2023 and became the parent company of Greatland Gold plc in a restructure where existing shareholders exchanged their shares in Greatland Gold plc for shares in the Company on 20 June 2025.

Prior to the restructure, Greatland Gold plc was the parent company of the Group. The restructure has been accounted for as a capital reorganisation and did not result in a business combination for accounting purposes. Financial information of the Group has been presented as a continuation of the pre-existing Greatland Gold plc consolidated entity. Accordingly, the assets and liabilities continued to be recorded at their existing values in the Consolidated Statement of Financial Position.

Prior period financial information contained in this report therefore represents the consolidated historical financial information for Greatland Gold plc.

On 24 June 2025, the Company successfully commenced trading on the ASX following an Initial Public Offering (IPO) of $490.0 million (before costs), which included ~$50.0 million by way of a subscription of new shares in the Company and approximately $440.4 million by way of a secondary sell-down by Bright SaleCo Limited, a special purpose vehicle incorporated to facilitate the sale under the IPO of 50% of Newmont's shares in Greatland. A separate offer to UK resident retail investors was also oversubscribed and successfully completed, raising a further ~$14.0 million in gross proceeds.

c) Basis of consolidation

The consolidated financial statements comprise of the financial statements of Greatland and its subsidiaries.

Subsidiaries are those entities controlled directly or indirectly by the Company. The results of the subsidiaries are included in the Consolidated Statement of Comprehensive Income for the same reporting period or the date of acquisition (where applicable) using the same accounting policies as those of the Group.

The consideration transferred in a business combination is the fair value at the acquisition date of the assets transferred and the liabilities incurred by the Group and includes the fair value of any contingent consideration arrangement. Acquisition-related costs are recognised in the income statement as incurred. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair value at the acquisition date. All intra-group balances and transactions, including any unrealised income and expenses arising from intragroup transactions, are eliminated in full in preparing the consolidated financial statements.

d) Foreign currency translation

Both the functional and presentational currency of Greatland is Australian dollars. Each entity in the Group determines its own functional currency, the primary economic environment in which the entity operates, and items included in the financial statements of each entity are measured using that functional currency.

Transactions in foreign currencies are recorded at the spot rate at the date of the transaction. Monetary assets and liabilities denominated in foreign currencies are translated at the rate of exchange ruling at the balance sheet date. All differences are taken to the Consolidated Statement of Comprehensive Income.

On consolidation of a foreign operation, assets and liabilities are translated at the balance sheet rate, income and expenses are translated at average foreign currency rates prevailing for the relevant period. Gains/losses arising on translation of foreign controlled entities into Australian dollars are taken to the foreign currency translation reserve.

e) Significant accounting judgements, estimates and assumptions

Determination of mineral resources and ore reserves

The Group reports its Mineral Resources and Ore Reserves in accordance with the Joint Ore Reserves Committee (JORC) Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves - the JORC Code. The information on Mineral Resources and Ore Reserves is prepared by Competent Persons as defined by the JORC Code. Estimates of mineral resources and ore reserves are utilised in several estimates and judgments impacting the financial statements, in particular allocating value to acquired assets, assessing for indicators of impairment of non-current assets and in determining the depreciation/amortisation of assets using the units of production method

There are numerous uncertainties inherent in estimating Mineral Resources and Ore Reserves. Assumptions that are valid at the time of estimation may change significantly when new information becomes available.

Changes in the forecast prices of commodities, exchange rates, production costs or recovery rates may change the economic status of reserves and may, ultimately, result in the reserves being restated. Such changes may impact asset carrying values, depreciation and amortisation rates, deferred development costs and provisions for restoration.

Other critical accounting judgements

Other critical accounting judgements, estimates and assumptions are discussed in the following notes:

Description | Notes |

Income tax | 8 |

Unit of production method of depreciation / amortisation | 13 |

Impairment of assets | 11, 12, 13 |

Exploration and evaluation assets | 12 |

Life of component ratio for stripping asset | 13 |

Mine rehabilitation provision | 15 |

Share based payments | 24 |

Acquisition of Havieron project and Telfer gold-copper mine | 25 |

The Group has adopted all of the new, revised or amending Accounting Standards and Interpretations issued by the AASB that are relevant to its operations and effective for an accounting period that begins on or after 1 July 2024.

Set out below are the new and revised Standards and amendments thereof effective for the current year that are relevant for the Group:

f) New standards and interpretations effective from 1 July 2024:

· AASB 2020-1 Amendments to Australian Accounting Standards: Classification of Liabilities as Current or Non-Current (AASB 101)

· AASB 2022-6 Amendments to Australian Accounting Standards: Non-Current Liabilities with Covenants (AASB 101)

· AASB 2022-5 Amendments to Australian Accounting Standards: Lease Liability in a Sale and Leaseback (AASB 16)

· AASB 2023-1 Amendments to Australian Accounting Standards: Disclosures and Statement of Cash Flows: Supplier Finance Arrangements (AASB 7 & AASB 107)

The amendments listed above did not have any material impact on the Group.

g) New accounting standards and interpretations issued but not effective

At the date of approval of these financial statements, the following standards and interpretations which have not been applied in these financial statements were in issue but not yet effective:

· AASB 2023-5 Amendments to Amendments to Australian Accounting Standards: Lack of Exchangeability - effective 1 January 2025 (AASB 1, AASB 121 & AASB 1060)

· AASB 2024-2 Amendments to Australian Accounting Standards: Classification and Measurement of Financial Instruments - effective 1 January 2026 (AASB 7 & AASB 9)

· AASB 18 Presentation and Disclosure in Financial Statements - effective 1 January 2027

The new and amended Standards and Interpretations which are in issue but not yet mandatorily effective, with exception to the item listed below, are not expected to have a material impact on the Group.

AASB 18 Presentation and Disclosure in Financial Statements

AASB 18 was issued in June 2024 and will replace AASB 101 Presentation of Financial Statements, effective for annual periods beginning on or after 1 January 2027. The new standard introduces new classification and presentation requirements, primarily impacting the Consolidated Statement of Comprehensive Income and related notes, as well as introducing additional disclosure requirements for management-defined performance measures.

The Group is in the process of assessing the impact of the new standard, however it is not expected to have an impact on the recognition and measurement of assets, liabilities, income and expenses, and is expected to only result in changes in the classification and presentation of these in the consolidated financial statements, as well as some additional disclosures in the notes.

The Group does not intend to early adopt any of the new standards or interpretations. It is expected that where applicable, these standards and interpretations will be adopted on each of the respective effective dates.

FINANCIAL PERFORMANCE

This section focuses on the financial performance of the Group, covering both profitability and resulting return to shareholders via earnings per share.

3 SEGMENTAL INFORMATION

Operating segments are reported in a manner that is consistent with the internal reporting to the Group's executive management team (the Chief Operating Decision Makers) for the purpose of making decisions about resource application and assessing performance.

Greatland operates two segments, the principal activities of each are summarised below:

· Telfer-Havieron - mining and processing of gold and copper, mine development

· Exploration - exploration and evaluation of gold and copper mineralisation

Segment results for the year ended 30 June 2025

| Telfer-Havieron $'000 | Exploration $'000 |

Corporate and other $'000 | Total $'000 |

Revenue | 957,367 | - | - | 957,367 |

Cost of sales, excluding depreciation and amortisation | (420,854) | - | - | (420,854) |

Segment gross profit | 536,513 | - | - | 536,513 |

Exploration and evaluation expenses | (2,377) | (7,469) | - | (9,846) |

Segment EBITDA | 534,136 | (7,469) | - | 526,667 |

Depreciation and amortisation | (40,526) | - | (281) | (40,807) |

Segment EBIT | 493,610 | (7,469) | (281) | 485,860 |

Capital expenditure | 210,855 | 10 | 6,787 | 217,652 |

Segment assets | 2,019,693 | 1,087 | 94,596 | 2,115,376 |

Segment liabilities | (1,581,829) | (18,861) | 825,425 | (775,265) |

Segment results for the year ended 30 June 2024 (Restated)

| Telfer-Havieron $'000 | Exploration $'000 |

Corporate and other $'000 | Total $'000 |

Revenue | - | - | - | - |

Cost of sales, excluding depreciation and amortisation | - | - | - | - |

Segment gross profit | - | - | - | - |

Exploration and evaluation expenses | (301) | (7,785) | - | (8,086) |

Segment EBITDA | (301) | (7,785) | - | (8,086) |

Depreciation and amortisation | - | - | (310) | (310) |

Segment EBIT | (301) | (7,785) | (310) | (8,396) |

Capital expenditure | 31,471 | - | 358 | 31,829 |

Segment assets | 160,597 | 1,500 | 9,461 | 171,558 |

Segment liabilities | (219,636) | (11,631) | 137,810 | (93,457) |

Segment EBITDA is a non-IFRS measure, being earnings before interest, tax, depreciation and amortisation and is calculated as follows profit before income tax, plus depreciation, amortisation, impairment, share based payments, corporate and finance costs less interest income.

Interest income, finance costs and acquisition costs are not allocated to the operating segments as this type of activity is driven by the central finance function which manages the cash position of the Group.

Segment EBIT reconciles to net profit before tax for the year ended 30 June 2025 as follows:

| 2025 $'000 | 2024 (Restated) $'000 |

Segment EBIT | 485,860 | (8,396) |

Corporate and other expenses | (41,109) | (11,007) |

Share based payment expense | (28,610) | (6,299) |

Transaction costs related to Telfer-Havieron acquisition | (14,748) | (2,914) |

Transaction costs related to the IPO | (6,779) | - |

Other income | 30,259 | 129 |

Finance income | 23,623 | 1,576 |

Finance costs | (6,593) | (1,650) |

Profit/ (loss) before tax | 441,903 | (28,561) |

Geographical information

Substantially all of the Group's assets and liabilities are located in Australia.

The geographical information below analyses statutory Group revenue from continuing operations. Revenue is primarily presented by the geographical destination of the product.

| 2025 $'000 | 2024 (Restated) $'000 |

Australia | 137,435 | - |

China | 511,363 | - |

Rest of Asia | 288,716 | - |

Canada | 19,853 | - |

Total revenue | 957,367 | - |

4 REVENUE

|

| 2025 $'000 | 2024 (Restated) $'000 |

Revenue from contracts with customers | |||

Dore | 137,851 | - | |

Concentrate | 713,185 | - | |

Treatment and refining deductions | (941) | - | |

Total gold revenue |

| 850,095 | - |

Concentrate | 94,311 | - | |

Treatment and refining deductions | 2,792 | - | |

Total copper revenue | 97,103 | - | |

Dore | 148 | - | |

Concentrate | 4,552 | - | |

Treatment and refining deductions | (55) | - | |

Total silver revenue |

| 4,645 | - |

Revenue from the provision of freight services | 9,457 | - | |

Total revenue from contracts with customers | 961,300 | - | |

Hedge gains / (losses) | (3,933) | - | |

Total sales revenue |

| 957,367 | - |

Recognition and measurement

The Group primarily generates revenue from the sale of gold, copper and silver in the form of concentrate and dore. The sales of these commodities are considered to be performance obligations as they are the contractual promises by the Group to transfer distinct goods to customers. The transaction price allocated to each performance obligation is recognised as the performance obligation is satisfied. Satisfaction occurs when control of the promised commodity is transferred to the customer.

Dore revenue is recognised at a point in time upon transfer of control to the customer and is measured at the amount to which the Group expects to be entitled which is based on the deal agreement. Concentrate revenue is recognised net of treatment and refining charges upon receipt of the bill of lading when the goods are delivered for shipment under Cost, Insurance, and Freight (CIF) Incoterms.

Revenue from the provision of freight services

The Group sells most of its commodities on CIF Incoterms. In the case of CIF Incoterms, the Group is responsible for shipping services after the date at which control of the commodities passes to the customer at the port of loading. The provision of shipping services in these types of arrangements are a distinct service (and therefore a separate performance obligation) to which a portion of the transaction price should be allocated and recognised over time as the shipping services are provided.

5 COST OF SALES

|

| 2025 $'000 | 2024 (Restated) $'000 |

Site production costs | 281,577 | - | |

Employee benefit expenses | 55,002 | - | |

Royalties | 31,269 | - | |

Selling costs | 13,594 | - | |

Change in inventories | 39,412 | - | |

Depreciation and amortisation | 40,526 | - | |

Total cost of sales | 461,380 | - |

6 CORPORATE AND OTHER EXPENSES

|

| 2025 $'000 | 2024 (Restated) $'000 |

Employee benefit expenses | 15,849 | 7,000 | |

Depreciation and amortisation | 281 | 310 | |

Other administrative costs (including integration) | 25,260 | 4,007 | |

Total corporate and other expenses | 41,390 | 11,317 |

7 OTHER INCOME / (EXPENSES)

|

| 2025 $'000 | 2024 (Restated) $'000 |

Gains / (losses) on financial assets at fair value through profit or loss | 17,231 | (93) | |

Other income | 13,028 | 222 | |

Total other income / (expenses) | 30,259 | 129 |

8 INCOME TAX

Income tax expense comprises current and deferred tax and is recognised in profit or loss, except to the extent it relates to items recognised in equity as disclosed below:

|

| 2025 $'000 | 2024 (Restated) $'000 |

Components of income tax are: | |||

Current income tax | |||

Current year tax expense / (benefit) | 121,208 | - | |

Adjustment for current tax of prior periods | - | - | |

Deferred income tax | |||

Deferred tax expense / (benefit) | 28,743 | - | |

Bring to account tax (benefit) on tax losses and other temporary differences | (45,308) | - | |

Adjustment for deferred tax of prior periods | - | - | |

Total income tax expense | 104,643 | - |

|

| 2025 $'000 | 2024 (Restated) $'000 |

Reconciliation of income tax expense to pre-tax profit: |

|

|

|

Profit / (loss) from continuing operations before income tax | 441,903 | (28,560) | |

Income tax expense at the Australian tax rate of 30% (2024: weighted average rate of 28%) | 132,571 | (8,128) | |

Increase / (decrease) in income tax due to: | |||

Bring to account tax (benefit) on tax losses and other temporary differences | (45,308) | - | |

Share based payments | 8,583 | 1,877 | |

Other permanent differences | 7,694 | - | |

Net deferred tax assets not brought to account | 1,103 | 14,156 | |

Movement in unrecognised temporary differences | - | 19 | |

Deferred tax relating to the origination and reversal of temporary differences | - | (7,924) | |

Total income tax expense / (benefit) | 104,643 | - | |

|

| 2025 $'000 | 2024 (Restated) $'000 |

Deferred income tax related to items recognised directly in other comprehensive income / (loss): |

|

|

|

Derivative financial instruments | 4,129 | - | |

Total | 4,129 | - |

|

| 2025 $'000 | 2024 (Restated) $'000 |

Current tax (liability) / asset: |

|

|

|

Opening balance at 1 July | - | - | |

Tax paid / (refunded) |

| - | - |

Current tax charge | 121,208 | - | |

Utilisation of prior period tax losses | (45,096) | ||

Adjustment for current tax of prior periods | - | - | |

Closing balance | 76,112 | - |

Temporary differences brought to account

Deferred tax assets: |

| 2025 $'000 | 2024 (Restated) $'000 |

The balance comprises temporary differences attributable to: | |||

Mine development | - | 6,331 | |

Provisions & accruals | 9,963 | 795 | |

Other deductible temporary differences | 4,731 | 3,339 | |

Derivative financial instruments recognised in other comprehensive income | 4,129 |

| |

Gross deferred tax assets | 18,823 | 10,465 | |

Amount offset from deferred tax liabilities pursuant to set-off provisions | (18,823) | (10,465) | |

Net deferred tax assets recognised | - | - | |

| |||

Deferred tax liabilities: | 2025 $'000 | 2024 (Restated) $'000 | |

The balance comprises temporary differences attributable to: | |||

Property, plant and equipment | (12,486) | (9,702) | |

Mine properties | (32,040) | ||

Exploration and evaluation assets | (10,439) | ||

Investments held at fair value | (5,169) | - | |

Other taxable temporary differences | (140) | (763) | |

Gross deferred tax liabilities | (60,274) | (10,465) | |

Amount offset from deferred tax assets pursuant to set-off provisions | 18,823 | 10,465 | |

Net deferred tax liabilities recognised | (41,451) | - | |

Unrecognised deferred tax assets: | 2025 $'000 | 2024 (Restated) $'000 |

Items for which no deferred tax assets have been recognised are attributable to the following: |

|

|

Rehabilitation, restoration and dismantling provision | 81,658 | - |

Unused tax losses1 | 10,533 | 45,645 |

Total unrecognised deferred tax assets | 92,191 | 45,645 |

1 Losses for which no deferred tax assets have been recognised relate to unrecognised UK revenue losses, unrecognised Australian revenue losses (prior year only) and unrecognised Australian capital losses.

Movements in deferred tax balances

Deferred tax assets

| Mine development $'000 | Provisions and accruals $'000 | Other $'000 | Total $'000 |

At 1 July 2024 (Restated) | 6,331 | 795 | 3,339 | 10,465 |

Recognition of prior year temporary differences | - | - | 213 | 213 |

Acquired as part of Telfer-Havieron acquisition (Note 25) | (6,331) | 13,798 | (3,339) | 4,128 |

(Charged) / credited to profit or loss | - | (4,630) | 4,518 | (112) |

Recognised directly in other comprehensive income / (loss) | - | - | 4,129 | 4,129 |

At 30 June 2025 | - | 9,963 | 8,860 | 18,823 |

Deferred tax liabilities

| Property, plant and equipment $'000 | Mine development $'000 | Exploration and evaluation $'000 | Other $'000 | Total $'000 | |

At 1 July 2024 (Restated) |

| (9,702) | - | - | (763) | (10,465) |

Acquired as part of Telfer-Havieron acquisition (Note 25) | (2,797) | (8,730) | (10,414) | 763 | (21,178) | |

(Charged) / credited to profit or loss | 13 | (23,310) | (25) | (5,309) | (28,631) | |

Recognised directly in other comprehensive income / (loss) | - | - | - | - | - | |

At 30 June 2025 |

| (12,486) | (32,040) | (10,439) | (5,309) | (60,274) |

Recognition and measurement

Current tax assets and liabilities for the period are measured at the amount expected to be recovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amount are those that are enacted or substantially enacted by the reporting date in the countries where the Group operates.

Income tax is charged or credited to profit or loss, except when it relates to items charged or credited directly to equity, in which case the income tax (current or deferred) is also dealt with in equity.

Deferred income tax is provided on all temporary differences between accounting carrying amounts and the tax bases of assets and liabilities at the balance sheet date.

Deferred income tax liabilities are recognised for all taxable temporary differences other than for the exemptions permitted under accounting standards.

Deferred income tax assets are recognised for all deductible temporary differences and unutilised tax losses only to the extent that it is probable that future taxable amounts will be available to utilise these other than for the exemptions permitted under accounting standards. The recognition of deferred tax assets requires management to assess the likelihood that the Group will comply with the relevant tax legislation in the jurisdictions in which it operates and will generate sufficient taxable earnings in future years to utilise these deferred tax assets. This assessment requires the use of estimates and assumptions such as commodity prices, operating performance and financing costs. The carrying amount of deferred tax assets is reviewed at each reporting date and reduced to the extent that it is no longer probable that sufficient taxable profits will be available to allow all or part of the deferred tax asset to be recovered.

Deferred income tax assets and liabilities are measured at the tax rates that are expected to apply in the period when the liability is settled or the asset realised, based on tax rate and tax laws that have been enacted or substantially enacted at the balance sheet date.

The Group offsets deferred tax assets and deferred tax liabilities if, and only if, it has a legally enforceable right to set off current tax assets and current tax liabilities and the deferred tax assets and deferred tax liabilities relate to income taxes levied by the same taxation authority on either the same taxable entity or different taxable entities which intend either to settle current tax liabilities and assets on a net basis, or to realise the assets and settle the liabilities simultaneously, in each future period in which significant amounts of deferred tax liabilities or assets are expected to be settled or recovered.

Tax consolidation

Greatland Holdings Group Pty Ltd, a 100% owned subsidiary of Greatland Gold plc, and its 100% owned Australian resident subsidiaries formed a tax consolidated group with effect from 14 February 2023. Greatland Holdings Group Pty Ltd is the head entity of the tax consolidated group. Members of the tax consolidated group have entered into a tax funding agreement under which the wholly-owned entities fully compensate Greatland Holdings Group Pty Ltd for any current tax payable assumed and are compensated by Greatland Holdings Group Pty Ltd for any current tax receivable and deferred tax assets related to unused tax losses or unused tax credits that are transferred to Greatland Holdings Group Pty Ltd under the tax consolidation regime.

Greatland Resources Limited is a standalone taxpayer in Australia and given it only recently became the parent company of the Group it has not formed a Tax Consolidated Group.

9 EARNINGS PER SHARE

|

| 2025 Cents | 2024 (Restated) Cents |

Basic earnings / (losses) per share | 63.57 | (11.23) | |

Diluted earnings / (losses) per share | 63.14 | (11.23) |

Weighted average number of shares used as the denominator | 2025 Number | 2024 (Restated) Number | |

Weighted average number of ordinary shares in calculating basic earnings per share | 530,560,004 | 254,230,255 | |

Adjustment for calculation of diluted earnings per share: Rights and options |

3,586,457 |

- | |

Weighted average number of ordinary shares in calculating diluted earnings per share |

| 534,146,461 | 254,230,255 |

Recognition and measurement

Basic earnings per share

Basic earnings per share is calculated by dividing profit / (loss) attributable to equity holders of Greatland and the weighted average number of ordinary shares outstanding during the financial year, adjusted for any bonus elements in the ordinary shares issued during the year and excluding treasury shares.

Diluted earnings per share

Diluted earnings per share adjusts the figures used in the determination of basic earnings per share to consider:

· the after-income tax effect of interest and other financing costs associated with dilutive potential ordinary shares; and

· the weighted average number of additional ordinary shares that would have been outstanding assuming the conversion of all dilutive potential ordinary shares.

The prior year comparative diluted losses per share excludes potential ordinary shares that would result in a decrease in basic losses per share, as they were considered anti-dilutive.

OPERATING ASSETS AND LIABILITIES

This section shows the assets used to generate the Group's trading performance and the liabilities incurred. Assets and liabilities relating to the Group's financing activities are addressed in the capital structure and financing section, Notes 16 to 22.

10 TRADE AND OTHER RECEIVABLES

| 2025 $'000 | 2024 (Restated) $'000 |

Trade receivables | 20,912 | - |

Sundry debtors | 13,250 | 262 |

Total trade and other receivables | 34,162 | 262 |

Recognition and measurement

Receivables are classified at initial recognition and subsequently measured at amortised cost or fair value through profit or loss. The classification of receivables at initial recognition depends on the receivable's contractual cash flow characteristics and the Group's business model for managing them. Trade receivables are initially measured at the transaction price determined in accordance with the accounting policy for revenue. All other receivables are initially measured at fair value.

Trade and other receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method. Trade receivables are less any allowance for the expected future issue of credit notes and for non-recoverability due to credit risk. The Group applies the simplified approach to measuring expected credit losses which uses a lifetime expected loss allowance for all trade receivables and contract assets. To measure expected credit losses, trade receivables and contract assets have been grouped based on shared risk characteristics. No such credit loss has been recorded in these financial statements as any effect would be immaterial.

11 INVENTORIES

Current | 2025 $'000 | 2024 (Restated) $'000 |

Ore stockpiles | 84,805 | - |

Gold in circuit | 9,895 | - |

Finished goods | 41,928 | - |

Consumable stores and spare parts | 63,678 | - |

Total current inventories | 200,306 | - |

Non-current |

| |

Ore stockpiles | 39,956 | - |

The cost of inventories recognised as an expense includes $nil (2024: $nil) in respect of write downs of inventory to net realisable value.

Recognition and measurement