10th Feb 2026 07:00

10 February 2026

www.asia-strategic.comAsia Strategic Holdings Ltd.

("Asia Strategic", the "Group" or the "Company")

Results for the financial year ended 30 September 2025

Asia Strategic Holdings Ltd. (LSE: ASIA), the independent developer and operator of consumer businesses in Emerging Asia, is pleased to announce the publication of its full year results for the financial year ended 30 September 2025.

The Group's audited financial statements for the year ended 30 September 2025 received an unqualified audit opinion ("FY25 Accounts"). The FY25 Accounts will be available on the Company's website at www.asia-strategic.com. A copy of the FY25 Accounts will be submitted to the National Storage Mechanism ("NSM") where it will be available for public inspection at: https://data.fca.org.uk/#/nsm/nationalstoragemechanism

Following publication of the FY25 Accounts and the uploading of them to the NSM, the Company will be requesting a restoration of the listing of the Ordinary Shares. In the meantime, the Company's Ordinary Shares remain suspended from the Official List Equity Shares (transition) category of the Financial Conduct Authority ("FCA") pending further notice.

The Directors of the Group confirms that the financial information for the years ended 30 September 2025 and 2024 are derived from the Group's audited financial statements and that these are not statutory accounts and, as such, do not contain all information required to be disclosed in the full financial statements prepared in accordance with International Financial Reporting Standards (IFRS) as adopted by the European Union. The financial information contained within this full year results statement was approved and authorised for issue by the Board on 9 February 2026.

All data for the reporting period refer to the financial year ended 30 September 2025 ("FY25") and the comparative period refer to the financial year ended 30 September 2024 ("FY24"), unless otherwise stated.

The year-on-year ("YOY") growth or decline refers to any change that occurred between FY25 and FY24, or equivalent periods of one year, as applicable.

All figures are reported in United States Dollars ("$"), unless otherwise specified.

All data pertaining to the student numbers across the report, including tables and charts, are rounded to the nearest ten for clarity and presentation purposes.

HIGHLIGHTS

Financial highlights

· Group revenue increased 8% YOY to $32.1 million in FY25 (FY24: $29.7 million).The Education division accounted for 78% of revenue (FY24: 76%), while Services contributed 22% (FY24: 24%). Key drivers of this growth included:

· A 19% increase in Myanmar's Education division (FY24: 42% increase) driven by contributions from new businesses and continued scaling of existing operations;

· A 2% growth in Services (FY24: 31% increase), as the Myanmar Services division continued to contribute through improved commercial positioning and expansion of high-value service offerings; and

· A 6% decline (FY24: 4% decline) in Vietnam's Education division due to the continued restructuring of Wall Street English Vietnam.

· Group gross profit increased 11% YOY to $18.9 million in FY25 (FY24: $17.0 million), with the Education division contributing 94% (FY24: 91%) and the Services division 6% (FY24: 9%). Revenue growth outpaced the cost of services, with the Group's gross margin improving to 59% (FY24: 57%). The improvement in the Education division gross margin to 71% (FY24: 68%) was offset by a decline in the Services division gross margin to 16% (FY24: 23%). The improvement within the Education division reflects the Group's growing operational efficiency as knowledge is consolidated across brands, leading to better cost control in mature businesses, while newer ventures continue to scale and meet expectations. The Services division's gross margin declined in FY25 due to a shift toward a lower-margin contract mix driven by local business demand coupled with continued cost inflation.

· The Group's net loss narrowed to $6.3 million in FY25 (FY24: $11.0 million loss), primarily reflecting the absence of a one-time $4.6 million goodwill impairment at Wall Street English Vietnam recorded in FY24. The main cause of the losses in FY25 was a foreign exchange loss of $2.8 million, due to heightened currency volatility in key markets, and a plant and equipment write-off of $0.5 million, due to earthquake damage. Despite this, operating expenses were effectively controlled, increasing by only 1% YOY, underscoring management's disciplined cost management as new businesses scale and mature operations become more efficient.

· Group adjusted EBITDA loss (excluding impairment losses and interest on lease liabilities) also narrowed to $0.3 million in FY25 (FY24: $0.7 million loss). The improvement was driven by reduced losses at Wall Street English Vietnam and growth in the Group's start-up businesses, partially offset by higher foreign exchange losses. Marketing expenses decreased $0.4 million YOY to $3.1 million in FY25, reflecting improved spending efficiency amid stronger sales activity. Overall, underlying operational performance strengthened as cost control measures and improved performance at the Group's start-up businesses took effect.

· At 30 September 2025, deferred revenue, representing cash received in advance of service delivery, was $18.9 million, of which $14.5 million (30 September 2024: $12.4 million) was current, and $4.4 million (30 September 2024: $2.0 million) was non-current.

· The Group reported a positive operating cash flow of $3.9 million (FY24: $3.9 million) because of increased advance payments in the Education division. If repayment of lease liabilities (including principal and interest) were considered, the Group would have recorded a positive cash flow of $0.7 million (FY24: positive $0.6 million). This improvement reflects a more efficient cash conversion cycle and disciplined working capital management. In parallel, the Group adopted a more strategic approach at Wall Street English Vietnam, implementing targeted cost reductions and commercial adjustments to support its pathway to profitability.

· The Group invested $0.7 million in FY25 (FY24: $2.5 million), primarily to establish four new schools across the Group's newer brands, Kids&Us and Logiscool. A significant portion of the investment was directed towards the repair and renovation of Auston's and Wall Street English's Mandalay schools following the devastating earthquake in March 2025. Capital expenditures across other businesses were limited to routine maintenance.

· The Group maintained a $4.5 million loan facility with MACAN, the Group's largest shareholder. During FY25, $45k was drawn down. As of the report date, $0.8 million remains available to the Group.

· Diversification of the Group's operations across multiple countries continues to play an important role in mitigating single-country risk. Management has determined that there are sufficient mitigating actions within the Group's control to ensure liquidity for at least the next twelve months from the date of this report. These include controlled business expansion, disciplined financial management, access to the unused loan facility with MACAN, diversification of the capital structure through potential bank loans, and vendor financing.

Operational Highlights

Education

· Revenue from Education businesses increased 10% YOY to $25.0 million in FY25 (FY24: $22.7 million).

· At 30 September 2025, deferred revenue from Education businesses, representing cash received in advance of service delivery, comprised:

- Current: $14.2 million (30 September 2024: $12.1 million)

- Non-Current: $4.4 million (30 September 2024: $2.0 million).

· The Education division operates across Vietnam and Myanmar with the following businesses:

Vietnam

(i) Wall Street English - English language education for adults.

(ii) Kids&Us - English language education for children and teens.

(iii) Logiscool - Coding education for children and teens.

Myanmar

(i) Wall Street English - English language education for adults.

(ii) Kids&Us - English language education for children and teens.

(iii) Logiscool - Coding education for children and teens.

(iv) Yangon American International School ("Yangon American") - K-12 international school.

(v) Auston - Tertiary education.

· The number of schools and students at the end of each financial year were:

Number of Schools | Number of Students | |||||

2025 | 2024 | 2023 | 2025 | 2024 | 2023 | |

Vietnam | 16 | 17 | 11 | 4,610 | 4,300 | 4,040 |

Wall Street English | 7 | 9 | 7 | 3,320 | 3,450 | 3,680 |

Kids&Us | 6 | 6 | 4 | 1,130 | 770 | 360 |

Logiscool | 3 | 2 | - | 160 | 80 | - |

Myanmar | 19 | 16 | 9 | 5,800 | 5,030 | 4,650 |

Wall Street English | 5 | 6 | 5 | 3,290 | 3,260 | 3,700 |

Kids&Us | 4 | 3 | 1 | 610 | 480 | 100 |

Logiscool | 6 | 3 | - | 850 | 320 | - |

Yangon American | 2 | 2 | 1 | 190 | 150 | 100 |

Auston | 2 | 2 | 2 | 860 | 820 | 750 |

Group | 35 | 33 | 20 | 10,410 | 9,330 | 8,690 |

Vietnam

The number of students increased 7% compared to 30 September 2024 driven by growth at Kids&Us Vietnam and Logiscool Vietnam.

· Wall Street English Vietnam: The number of students decreased during the year but only slightly, as the closure of two schools was offset by the increased demand for the online product. A new leadership team was appointed to lead the transition to profitability by improving operational efficiency, optimising digital channels, and strengthening collaboration with the franchisor. In response to a continued shift towards online preferences, the Group adjusted staffing, restructured service teams, downsized space, and recalibrated its commercial strategy.

· Kids&Us Vietnam: Growth continued with financial and operational performance broadly in line with expectations, supported by maturing schools (five out of six schools have over 150 students) that are delivering higher enrolment and operating leverage, driving improved unit economics. Retention rates have strengthened, though they remain below the levels required to reach optimal capacity utilisation. The Group advanced its growth agenda by refining site selection toward smaller spaces and improving service team efficiency to maximise class sizes, optimise space utilisation, and enhance margins.

· Logiscool Vietnam: Growth remained subdued with weak commercial performance and limited school expansion. With new leadership and a fresh approach to commercialisation, Logiscool Vietnam is positioned to achieve better commercial performance going forward.

Myanmar

The number of students increased 15% compared to 30 September 2024 driven by growth across all brands. Despite significant challenges, notably the earthquake in Mandalay, performance was strong demonstrating the resilience of the businesses.

· Wall Street English Myanmar: Price increases, combined with stable student enrolment, supported growth, although they also raised affordability concerns among certain customer segments. The team continued to respond effectively to market pressures by reducing dollar-denominated costs and enhancing pricing competitiveness, positioning the brand for stronger performance in FY26.

· Kids&Us Myanmar: The experienced leadership team, shared with Vietnam since early FY25, has stabilised the business and contributed to strong enrolment. However, retention rates were softer than expected which limited growth. Management is actively addressing this through targeted operational initiatives and service-level improvements.

· Logiscool Myanmar: Robust growth was driven by a combination of accumulated market knowledge, an experienced commercial team, and a favourable market position. Enrolment numbers nearly tripled, while revenue increased almost sevenfold.

· Yangon American: Growth remained stable, supported by a stronger commercial focus and a more consistent faculty base. A key milestone during the period was the appointment of an experienced Head of School to lead Yangon American through its next phase. A new site in central Yangon for the Secondary school opened in January 2026. The new site provides the required indoor and outdoor space for older students. At the same time, relocating the existing Junior High and High School students to the new campus frees up space at the existing Elementary campus to expand lower-grade capacity. These developments position Yangon American for a potential breakthrough year ahead.

· Auston: Further announcements on the conscription law have created renewed uncertainty among younger demographics, impacting student enrolments in early 2025. The Mandalay earthquake in March further compounded the acquisition cycle and increased operating costs. Despite these challenges, Auston demonstrated resilience under new leadership, with sales and enrolment stabilising. The academic offering was strengthened through new partnerships with UK academic institutions.

Services

· Revenue from Services businesses increased 2% YOY to $7.1 million in FY25 (FY24: $7.0 million).

· At 30 September 2025, deferred revenue from Services businesses, representing cash received in advance of service delivery, was $0.3 million (30 September 2024: $0.3 million). The marginal decrease is the result of a large one-off integrated security project with revenue recognised in FY24.

The Services division consists of the following products:

Vietnam

(i) EXERA Vietnam - Integrated facility management.

· EXERA Vietnam: In FY24, the Group established EXERA Vietnam as an integrated facility management company to serve both internal and external customers. Modest revenue was generated from its first few customers in FY25. The Group is evaluating strategic partnership opportunities to strengthen and scale the business.

Myanmar

(i) EXERA Myanmar - Integrated risk management services.

(ii) Ostello Bello - Boutique hostels.

· EXERA Myanmar: Employed over 1,900 security officers as of 30 September 2025 (30 September 2024: circa 1,710) across circa 250 sites in Myanmar (30 September 2024: circa 230 sites). This growth was driven by new customer acquisition among local corporations as well as by the expansion of services to United Nations agencies and embassy clients.

· Ostello Bello: Operates one boutique hostel with circa 40 beds and circa 12 rooms in Bagan. The earthquake in Mandalay necessitated the difficult decision to close the Mandalay hostel after ten years in operation. Overall sector activity remains subdued due to the continued low levels of inbound international tourism.

SIGNIFICANT AND SUBSEQUENT EVENTS

1) Impact of the Myanmar earthquake and business continuity

On 28 March 2025, a 7.7-magnitude earthquake struck central Myanmar, followed by several aftershocks. The affected regions included Sagaing, Mandalay, Magway, Bago, and northeastern Shan State. The earthquake caused extensive disruption to electricity, internet connectivity, transportation, and essential public services.

Independent assessments estimate total economic damages at approximately $11 billion, equivalent to about 14% of Myanmar's GDP. Humanitarian agencies estimate that over 3,600 people died, approximately 200,000 people were displaced, and around 2 million people required critical humanitarian assistance.

The Group's corporate offices and operations in Yangon were largely unaffected, although the premises of Wall Street English, Logiscool, Auston, and Ostello Bello in Mandalay were significantly impacted and were closed for an extended period of time. No casualties or serious injuries were reported among our students, staff, or guests.

During the disruption, the Group transitioned immediately to online delivery for its English language and coding programmes. For learners without reliable access to electricity or internet, the Group offered study breaks, course extensions, and flexible scheduling. Structural engineering assessments were undertaken promptly on all facilities, and appropriate repair works were completed. All affected schools and facilities received the official safety approvals from the authorities and have now reopened. However, the damages necessitated substantial refurbishment and refitting. As a result, the Group has written off the carrying amounts of leasehold improvements and furniture & fittings for these sites, totalling $0.5 million, as disclosed in Notes 10 of the financial statements.

2) Safeguarding communities through earthquake response and recovery efforts

The Group responded rapidly to support its employees, students, and local communities. Immediate assistance included shelter, food, water, temporary accommodation, and relocation support for affected staff and stakeholders. The Group contributed approximately $30,000 through the European Chamber of Commerce to support emergency relief efforts.

To strengthen longer-term rehabilitation, the Group established an Earthquake Relief Fund, seeded with approximately $46,000 from key management and open to contributions from employees across the organisation. The fund provided targeted support to affected employees and contributed to broader community recovery initiatives.

EXERA, the Group's integrated risk-management business, played a vital on-the-ground role in Mandalay by providing site security, secure logistics, and emergency response services to ensure safe and effective distribution of humanitarian aid.

The Group has completed all required structural repairs to its school premises and obtained the necessary clearances. It remains fully committed to maintaining the highest safety standards as on-site operations resume. Asia Strategic Holdings remains focused on navigating the aftermath of the earthquake with resilience, prioritising the safety of its people and ensuring business continuity.

3) Global macroeconomic and geopolitical uncertainties

Global trade and geopolitics remain volatile through 2025 and early 2026, with the U.S. rolling out a baseline tariff and country-specific "reciprocal" tariffs in April 2025 and then recalibrating some rates and exemptions over subsequent months as negotiations progressed. The policy direction is still toward using tariffs to rebalance trade, but implementation has become more fluid: featuring temporary pauses, deal-linked adjustments, and sector carve-outs (notably recent agricultural exemptions). This shifting landscape continues to weigh on regional sentiment, supply chains, and inflation expectations, supporting a prudent stance on operating costs and capital allocation.

Vietnam has moved into a more constructive track within this framework. The U.S. and Vietnam agreed on 26 October 2025, a Framework for an Agreement on Reciprocal, Fair, and Balanced Trade: the U.S. keeps a 20% reciprocal tariff as the baseline for now, while working toward a product-specific exemption list that could reduce selected Vietnamese exports to 0% once a final agreement is signed and implemented. Vietnam, in return, will eliminate tariffs on nearly all U.S. exports and address key non-tariff barriers and enforcement areas. Talks remain active, but the scope and timing of U.S. zero-tariff carve-outs are still unresolved, so near-term uncertainty persists.

For Myanmar, reciprocal tariffs remain very high due to the absence of a concluded trade arrangement, implying continued external pressure on export-linked sectors and broader macro fragility.

4) Convertible Note Programme

Details of the updated Convertible Note Programme are disclosed in Note 20 to the financial statements.

COUNTRY ECONOMIC UPDATES

The most recent forecast by the Asian Development Bank (the "ADB") is for developing Asia's GDP growth of 5.1% in 2025 and 4.6% in 2026.

Inflation in developing Asia is expected to be 1.6% in 2025 and 2.1% in 2026, as supply chain disruptions ease further, lowering food and fuel prices.

Vietnam

The years stated below refer to the calendar year, which runs from 1 January to 31 December unless otherwise stated.

· According to the General Statistics Office of Vietnam (the "GSO"), GDP growth for the 9M 2025 was 7.9% YOY, exhibiting strong economic fundamentals and a long-term positive outlook. The full-year 2024 GDP growth was 7.1%, while ADB forecasts 6.0% growth in 2026. Average CPI for 9M 2025 increased by 3.3% YOY, while core CPI rose by 3.1%. Key inflation drivers included rising costs in education, transportation, F&B, electricity, housing, and construction materials.

· Vietnam's exports in the 9M 2025 are estimated to have grown 16% YOY to $348.7 billion, while imports were estimated to have increased 19% YOY to $332.0 billion. This led to a trade surplus of $16.8 billion, according to the GSO. For 9M 2025, Vietnam's trade surplus with the United States exceeded $99.0 billion, despite the 20% U.S. tariff on Vietnamese imports implemented in July 2025.

· Vietnam's industrial sector continued to strengthen in 9M 2025, with the Index of Industrial Production rising 9% YOY, according to the GSO. Meanwhile, Vietnam's S&P Global Manufacturing PMI remained at 50.4 in September 2025, unchanged from the previous month, indicating modest expansion supported by recovering new orders and sustained output growth.

· Vietnam's public investment disbursement reached $16.6 billion through 9M 2025, equivalent to 50% of the Prime Minister's annual target. With only four months remaining, half of the capital plan is still undisbursed, heightening pressure to achieve the Government's 100% target. Over the same period, Vietnam maintained strong foreign direct investment ("FDI") momentum, with realised FDI reaching a five-year high of $18.8 billion, up 9% YOY, and registered FDI rising 15.2% to $28.5 billion, underscoring investors' sustained confidence.

· Since early 2025, the Vietnamese Dong has depreciated more than 3% against the USD. Although Vietnam posted a $16.8 billion trade surplus in 9M 2025 and continued to receive solid FDI and remittance inflows, USD liquidity in the banking system remains tight as the Fed keeps rates at 4.00-4.25%. In response to the intense exchange rate pressure, the State Bank of Vietnam intervened by selling USD in August and then again in October 2025 worth a cumulative $2.9 billion.

· Over the past two decades, Vietnam has evolved from a low-income to an upper-middle-income band (from $4,466 to $13,845) according to the World Bank, with 2024 GDP per capita estimated at $4,700. With a population of 102.2 million in 2025 and a median age of 33.4 years old, Vietnam is the third most populous country in Southeast Asia, after Indonesia (284.4 million) and the Philippines (114.4 million) according to the International Monetary Fund. The population is projected to grow steadily, reaching 105.4 million by 2030.

· The country's Human Development Index rose from 0.493 in 1990 to 0.766 in 2023, placing Vietnam in the High Human Development category and ranking 93rd out of 193 countries and territories. According to the EF English Proficiency Index in 2024, Vietnam was still classified as "Low proficiency".

· The GSO estimates that Vietnam's workforce grew to 53.3 million during Q3 2025. The large and low-cost labour force, coupled with a stable and favourable macro environment, has made Vietnam an attractive hub for foreign investment. It is particularly appealing to global manufacturers looking to diversify and de-risk their value chain.

Myanmar

The years stated below refer to the calendar year, which runs from 1 January to 31 December, and the financial year below refers to the Myanmar financial period, which runs from 1 April to 31 March.

· Myanmar's economy remains stagnant, with the ADB forecasting GDP to contract by 3.0% in 2025, followed by a modest recovery of 2.0% in 2026. Activity across all sectors has declined sharply after the March 2025 earthquake, including manufacturing and services.

· Inflationary pressures persist due to supply disruptions caused by halted border trade and earthquake-related damage, which has reduced agricultural output in several regions. Lower import volumes are expected to drive further increases in food prices. The ADB projects inflation to reach around 30% by the end of 2025, easing to approximately 23% in 2026 as a result of a stabilising currency and weakening domestic demand.

· According to the World Bank, Myanmar recorded a trade surplus of about $1.0 billion (circa 1.3% of GDP) in FY25, driven mainly by import compression amid tighter licensing, and border disruptions. In the first half of FY26 (April-September 2025), the trade surplus narrowed to roughly $0.7 billion, about 50% lower than a year earlier, as reconstruction-related needs lifted imports by 23% against an 11% rise in exports. Structural shifts were evident, with land-route imports from Thailand down 81% in 2024 and sea imports up 37%, contributing to higher logistics costs and inflationary pressures. Looking ahead, significant risks remain as the economy is constrained by tight external financing, border-trade disruptions, and strong dollar/kyat dynamics. The trade surplus is more a symptom of import weakness than of export strength, creating inflationary pressures even as formal trade balances improve.

· According to the World Bank, Myanmar's fiscal deficit widened to 4.1% of GDP in FY25 and is expected to increase further to 4.9% in FY26, reflecting rising reconstruction and humanitarian spending. The current account shifted to a surplus of 3.2% of GDP in FY25, supported by import compression and remittances, but is expected to narrow to 0.4% of GDP in FY26. FDI remained low with commitments remaining steady at $1.0 billion in FY25 and $0.3 billion in the first half of FY26.

· CBM foreign-exchange interventions declined in 2025. Between April and October 2025, the CBM sold around $249 million in FX, compared with $780 million in the previous seven months and $1.2 billion a year earlier, amid constrained FX availability and a shifting focus to import controls. Demand for essential imports, including fuel, edible oil, and fertilisers, remained elevated due to reconstruction and supply-chain pressures.

· Myanmar faces persistent infrastructure and energy challenges, worsened by reduced FDI, limited external support, and widespread power shortages. Seasonal hydropower dependence and earthquake-related grid damage continue to drive frequent outages. Moreover, approximately 80% of natural gas production is committed through long-term contracts to neighbouring nations.

· Political uncertainty, including the introduction of conscription, and rising internal displacement continue to destabilise the labour market, hinder economic recovery, and shift consumer behaviour. Coupled with inflationary pressures, these factors have led to a significant rise in price sensitivity across the population.

· The ADB estimates per capita GDP will grow by 0.4% in 2025, after contracting by roughly 1.5% in 2024, implying a very shallow recovery in living standards. In line with this, the World Bank projects that aggregate output will remain around 13% below pre-pandemic levels in FY25, underscoring the depth of the shock. Meanwhile, the World Bank's State of Education in Myanmar report noted a significant rise in household spending on private tutoring in 2023, as families sought to support their children's education amid uncertain times, a trend that is expected to remain stable.

· Labour market conditions remain fragile, characterised by under-employment and a shift to low-productivity work. According to the World Bank, Myanmar's employment to working-age population ratio is 61%. Prolonged conflict remains a key factor for unemployment, and the World Bank reported that 3.6 million people (6% of the population) were internally displaced, and 22 million people (37% of the population) require humanitarian assistance as of November 2025.

CHAIRMAN'S STATEMENT

Dear Shareholders,

The past financial year was characterised by steady progress, disciplined execution, and continued resilience, notwithstanding the devastation brought by the 7.7 magnitude earthquake in Central Myanmar in March 2025. While the macroeconomic and geopolitical environment remained complex, the Group delivered meaningful revenue growth, strengthened its gross margins, and accelerated operational efficiency initiatives. These achievements underscore both the quality of our diversified platform and our commitment to empowering communities through education and essential services.

Achievements and Growth Potential

Group revenue increased 8% YOY to $32.1 million (FY24: $29.7 million), with the Education division contributing 78% and Services 22% of total revenue. Growth was underpinned by a strong contribution from Myanmar, whereas Vietnam remained subdued yet maintained a stable operational footing.

Key contributors included:

· Education Myanmar: Revenue grew 19%, supported by continued scaling of existing operations.

· Education Vietnam: Revenue declined 6%, driven by the ongoing restructuring of Wall Street English Vietnam, partially balanced by growth at other businesses.

· Services: Delivered 2% growth, underpinned by improved commercial positioning and enhanced delivery of high-value services.

Group gross profit rose 11% to $18.9 million, with gross margin growing to 59%, from improved operational efficiency and the contribution from maturing schools. Education gross margin improved to 71% from 68% the prior year, partially offset by a lower Services gross margin at 16% down from 23% the prior year.

These results reinforce the scalability and resilience of businesses as we continue to build a platform for long-term, sustainable growth.

Portfolio Optimisation and Operational Efficiency

FY25 was a year of focused execution as the Group strengthened operational resilience, optimising the portfolio, and maintaining firm financial discipline across all businesses. Management advanced several initiatives to enhance profitability and operational effectiveness:

· Restructuring at Wall Street English Vietnam: The closure of two underperforming schools, streamlining of administrative and operating costs, and tighter commercial execution created a leaner foundation for the future.

· Scalable, capital-efficient school formats: Expansion continued through smaller, modular formats across Kids&Us and Logiscool, supporting disciplined growth with lower upfront investment and quicker breakeven timelines.

· Enhanced cost control: Operating expenses rose only 5% despite inflationary pressures and currency volatility, reflecting strengthened processes and improved efficiency across the Group.

Financial Discipline and Cash Flow Strengthening

The Group's financial performance reflected the benefits of disciplined capital allocation and improving operational maturity:

· Net loss narrowed to $6.3 million (FY24: $11.0 million), with stable adjusted EBITDA at a $0.3 million loss (FY24: 0.7 million loss).

· Positive operating cash flow of $3.9 million (FY24: $3.9 million) and positive adjusted operating cash flow of $0.7 million after lease payments (FY24: $0.6 million).

· Deferred revenue increased to $18.9 million (FY24: $14.4 million), demonstrating a stable commercial pipeline.

· Capex contained at $0.7 million (FY24: $2.5 million), reflecting a disciplined investment approach.

Economic, Environmental, Social and Governance

Our commitment to responsible, inclusive and transparent business practices remains central to how we operate across Emerging Asia. In FY25, we continued to strengthen our social impact, deepen local capability development, and uphold international governance standards that guide our long-term sustainability.

Key indicators include:

· Over 2,700 employees across Myanmar and Vietnam, with 97% local workforce participation.

· 67% female representation, excluding security personnel.

· Continued adherence to ICoCA standards, reinforcing our commitment to ethical conduct and governance excellence.

Earthquake Response in Myanmar

In March 2025, a significant earthquake hit Mandalay affecting the surrounding communities and our schools. Our teams responded swiftly to ensure both the safety of our communities and the continuity of our services to customers.

Beyond operational resilience, we supported the wider community's recovery efforts through two channels: (i) a donation made via EuroCham Myanmar and (ii) targeted assistance for affected employees and their families through internal fundraising led by the Group's top management. These contributions amounted to a total of $76,000. This response reflects our long-standing commitment to the well-being of our people and the communities we serve.

Words of Appreciation

I would like to express my sincere appreciation to our employees, customers, partners, and shareholders for their unwavering support throughout the year. Their resilience and dedication continue to drive our progress and reinforce our long-term potential across Emerging Asia.

Sincerely, Richard Greer Independent Non-Executive Chairman9 February 2026

Enrico Cesenni, Chief Executive Officer of Asia Strategic, commented:

"FY25 was a year of resilience and unity for the Group. The tragic earthquake in central Myanmar last March affected over two million lives.

"While the impact on the Group's operations was contained, we recognise the broader national impact and our responsibility to support affected communities. In response, we mobilised financial and human resources to assist employees and partnered with organisations delivering on-the-ground relief.

"Despite these challenges, the Group delivered strong results. Revenue surpassed $32 million, up 8% YOY (FY24: $29.7 million), reflecting sustained demand and brand loyalty in Vietnam and Myanmar. Gross profit rose to $18.9 million (FY24: $17.0 million) with margins improving to 59% (FY24: 57%), driven by continued operational efficiencies in education businesses such as larger class sizes from improved scheduling and the introduction of local teachers.

"In line with our commitment to financial discipline, we made the difficult but necessary decision to close two underperforming schools, as well as one school and one hostel affected by the earthquake. This allows us to preserve capital and sharpen our strategic focus.

"We remain committed to long-term value creation and believe strongly in the potential of Emerging Asia. On behalf of the Board, I thank our shareholders for their trust and extend heartfelt appreciation to the Asia Strategic team for their resilience and dedication-especially in the wake of the Mandalay earthquake.

"Together, we are navigating challenges and building enduring value for the communities we serve"

For more information, please visit www.asia-strategic.com or contact:

Asia Strategic Holdings Ltd. Richard Greer, Independent Non-Executive Chairman Enrico Cesenni (OSI), Founder and CEO

| |

Allenby Capital Limited (Broker) Nick Athanas Nick Naylor Lauren Wright

|

+44 (0)20 3328 5656

|

Yellow Jersey PR (Financial PR) Shivantha Thambirajah

| +44 (0) 20 3004 9512

|

Notes to editors

Asia Strategic Holdings Ltd. (LSE: ASIA) is an independent developer and operator of consumer businesses focused on Education and Services in Emerging Asia, specifically Vietnam and Myanmar.

Education Division: The Group operates a diverse portfolio of education brands, encompassing English language learning, coding, K-12 international education, and tertiary education. As of 30 September 2025, the Education division consisted of 35 schools, serving 10,410 students.

Service Division: The Group operates two brands: (i) EXERA, an integrated risk and facilities management services provider in Myanmar and Vietnam, with over 1,900 security officers across 250 sites; and (ii) Ostello Bello, a boutique hostel located in Bagan.

Asia Strategic Holdings utilises an asset-light strategy to scale its operations and capitalises on emerging opportunities in Vietnam and Myanmar.

To receive news alerts on Asia Strategic Holdings please sign up here under the 'RNS' header: https://asia-strategic.com/investor-relations/

OPERATIONAL REVIEW

EDUCATION

The Group's objective for its Education division is to become a leading operator and retailer of tech-enabled education services in Emerging Asia.

Revenue from Education businesses increased 10% YOY to $25.0 million in FY25 (FY24: $22.7 million).

At 30 September 2025, deferred revenue from Education businesses, representing cash received in advance of service delivery, was:

- Current: $14.2 million (30 September 2024: $12.1 million)

- Non-Current: $4.4 million (30 September 2024: $2.0 million)

Within its Education division, the Group provides educational products for children, teens, and adults through five brands across Vietnam and Myanmar.

Franchised Brands

Wall Street English is a leading English language education provider for adults with over 180,000 students enrolled in 29 countries. Its flexible and integrated blended learning solution is offered online or through a hybrid online/in-centre approach.

Kids&Us is a leading English language education provider for children starting at age one and operates in ten countries with over 180,000 students enrolled across 600 schools. Its unique teaching method focuses on natural language acquisition, personalised for each student's age and experiences.

Logiscool is an enrichment programme that teaches children coding and digital literacy. Logiscool operates in 30 countries across more than 360 locations with over 320,000 students enrolled and graduated. Logiscool's unique educational platform is developed so users can easily transition from visual coding to text-based programming languages.

Own Brands

Yangon American offers an international K-12 education, is an authorised International Baccalaureate Primary Years Programme school and an IB Middle Years Programme school, and is a candidate to be accredited as a Western Association of Schools and Colleges ("WASC") school.

Auston is a private higher education provider in Myanmar offering internationally recognised engineering and IT diplomas and degrees through partnerships with the University of Wolverhampton

(since December 2025), the University College Birmingham (since February 2026), Liverpool John Moores University (since February 2020, now in teach-out), and through Pearson Edexcel and BTEC (UK-recognised) certifications obtained in April 2022 and May 2025,, respectively.

While each brand has its own unique characteristics and customer base, economies of scope, experience and scale are achieved through common management. One example is the creation of learning centres where multiple brands occupy the same building or are closely located reducing construction and operating costs, while creating one-stop educational experiences for families.

Vietnam

Revenue from Education businesses in Vietnam decreased 6% YOY to $7.7 million in FY25 (FY24: $8.2 million).

At 30 September 2025, deferred revenue from Education businesses in Vietnam, representing cash received in advance of service delivery, was:

- Current: $3.5 million (30 September 2024: $4.1 million)

- Non-Current: $0.7 million (30 September 2024: $0.7 million)

Wall Street English Vietnam is the largest revenue contributor for Vietnam and the third for the Group and is focused on achieving profitability.

Revenue from Kids&Us Vietnam is expected to continue growing as existing schools mature and new schools open. Students generally sign for longer periods, and a substantial portion of the non-current deferred revenue is attributed to Kids&Us Vietnam.

After facing challenges in the past two years, Logiscool Vietnam is set to rebound in FY26 with a renewed focus on brand repositioning and strategic expansion.

Wall Street English Vietnam

· Revenue from Wall Street English Vietnam decreased 12% YOY to $6.7 million in FY25 (FY24: $7.6 million). The decline is attributable to a reduced number of schools and a lower average revenue per user, driven by a shift in product mix with the lower-priced online delivery.

· Student enrolment declined 4% from 30 September 2024 to circa 3,320 students at 30 September 2025 with the closing of two schools partially offset by an increase in online students.

· A refreshed management team with strengthened commercial, operational, and digital capabilities has been appointed to enhance performance discipline and accelerate the business turnaround.

· Cost reduction measures, including school rightsizing to reduce rental expenses and staff restructuring, have been implemented aggressively to restore profitability.

· Two underperforming legacy schools were closed during FY25, reducing the number of operating schools to seven. At 30 September 2025, Wall Street English Vietnam operated six schools in Ho Chi Minh City and one school in Binh Duong.

Kids&Us Vietnam

Revenue from Kids&Us Vietnam increased 60% YOY to $0.9 million in FY25 (FY24: $0.6 million), reflecting accelerating commercial traction as the brand continues to establish itself in the market.

· Student enrolment grew 47% from 30 September 2024 to circa 1,130 students at 30 September 2025, supported by stronger brand recognition and an improved retention rate.

· As the portfolio matures and with a stable leadership team, the Group refined its site and operating model, prioritising smaller, more efficient spaces and driving improvements in procurement, classroom utilisation, and service-team productivity. These initiatives are enhancing unit economics and strengthening margins across the network.

· At 30 September 2025, Kids&Us Vietnam operated six schools in Ho Chi Minh City, all of which have continued to scale and deepen their market positioning.

Logiscool Vietnam

· Revenue from Logiscool Vietnam was $0.1 million in FY25 (FY24: $23k).

· Student enrolment doubled from 30 September 2024 to circa 160 students as of 30 September 2025. Despite the slow growth, the business holds strong potential for recovery in FY26.

· Logiscool Vietnam opened its third school in Ho Chi Minh City in July 2025 as part of its effort to strengthen brand presence and expand accessibility.

· As of 30 September 2025, Logiscool Vietnam operated three schools, two in Ho Chi Minh City and one in Binh Duong.

Myanmar

Revenue from Education businesses in Myanmar increased 19% YOY to $17.3 million in FY25 (FY24: $14.4 million).

At 30 September 2025, deferred revenue from Education businesses in Myanmar, representing cash received in advance of service delivery, was:

- Current: $10.7 million (30 September 2024: $8.0 million)

- Non-Current: $3.7 million (30 September 2024: $1.3 million)

Wall Street English Myanmar is the largest English language education provider and revenue contributor to the Group.

Kids&Us Myanmar launched in June 2023 and quickly established itself as the market leader.

Logiscool Myanmar launched in November 2023 and mirrored Kids&Us Myanmar's success showcasing the Group's ability to set up market-leading businesses quickly and efficiently in Myanmar.

Auston experienced strong revenue growth among the Group's education businesses in Myanmar over the years. The growth is expected to continue as it is responsible for most of the deferred revenues and sees robust demand for international tertiary education, with a scarcity of quality local options.

Yangon American International School experienced a marginal revenue increase, with student numbers growing organically amid difficult macro and socio-economic conditions. Yangon American has reached circa 190 students.

Wall Street English Myanmar

· Revenue from Wall Street English Myanmar increased 6% YOY to $8.2 million in FY25 (FY24: $7.7 million).

· Student enrolment marginally grew by 1% from 30 September 2024 to circa 3,290 at 30 September 2025, despite the temporary closure of physical schools in Mandalay following the earthquake.

· The price increases helped offset the stagnant student numbers but raised affordability concerns. With an increased mobility of the population, there was a growing demand for convenient online products.

· The team continued to fine-tune its offering to reduce dollar-based costs and offer more competitive pricing:

- Local teachers were incorporated into the service delivery, reducing the reliance on expat teachers.

- Online class scheduling was streamlined, and a local online classroom was established to reduce dependency on international teachers.

· At 30 September 2025, Wall Street English Myanmar operated five schools with four in Yangon and one in Mandalay. One of the schools in Mandalay was closed in the aftermath of the devastating earthquake in March 2025.

Kids&Us Myanmar

· Revenue from Kids&Us Myanmar doubled YOY to $0.9 million in FY25 (FY24: $0.4 million).

· Student enrolment grew 27% from 30 September 2024 to circa 610 at 30 September 2025. The business is yet to reach its full potential, slowed by lower than expected retention rates.

· Kids&Us Myanmar remains the premium operator in the market with strong brand positioning. Supported by a shared and experienced leadership team with Kids&Us Vietnam. Financial and operational performance remain on track. The business is well-positioned for continued growth, with ample opportunities in Yangon and Mandalay.

· Kids&Us Myanmar opened its fourth school in central Yangon in July 2025, sharing facilities with both Logiscool and Yangon American.

· As of 30 September 2025, Kids&Us Myanmar operated four schools in Yangon.

Logiscool Myanmar

· Revenue from Logiscool Myanmar increased almost sevenfold to $1.0 million in FY25 (FY24: $0.1 million) .

· Student enrolment grew 166% from 30 September 2024 to circa 850 at 30 September 2025 and exceeded expectations in both Yangon and Mandalay.

· Similar to Kids&Us Myanmar, Logiscool Myanmar leveraged an experienced commercial team and introduced a new product into a market with limited competition. Its cloud-based, low-cost model supports healthy margins and strong operating leverage, offering promising economics as it expands in Myanmar.

· Logiscool Myanmar opened its first school in Mandalay (fourth overall) in December 2024, fifth and sixth schools (countrywide) in Yangon in May 2025 and July 2025, respectively. The sixth school shares facilities with Kids&Us and Yangon American.

· At 30 September 2025, Logiscool Myanmar operated five schools in Yangon and one in Mandalay.

Yangon American International School

· Revenue from Yangon American International School increased 46% YOY to $1.8 million in FY25 (FY24: $1.2 million). Growth was primarily supported by net new student additions throughout the year, with about 30 additional students in the academic year ("AY") 2024-25 and a further 20 in AY 2025-26, along with an increase in the average tuition fee paid.

· Student enrolment grew 27% from 30 September 2024 to circa 190 at 30 September 2025. In August 2025, the school opened ninth grade, and it plans to add a new grade annually until it reaches the twelfth grade.

· Yangon American has established itself as the leading International Baccalaureate school in the market, with Primary Years Programme and Middle Years Programme authorisations. It is also a candidate for the Western Association of Schools and Colleges accreditation.

· A key highlight during FY25 was the confirmation of a new site in central Yangon, featuring pre-existing facilities available for Yangon American's planned Secondary Campus, set to open in early 2026 pending final regulatory approvals. The central location near embassies, UN agencies, and city landmarks enhances accessibility and safety, reinforces Yangon American's premium positioning, and supports community trust. The move will also ease pressure on the current Elementary Campus, enabling the launch of additional classes in some grades as well as the creation of dedicated learning hubs and specialised support rooms to enrich the learning environment.

· At 30 September 2025, Yangon American operated an Early Years Village and a separate Elementary Campus in Yangon. The Secondary Campus is scheduled to open in January 2026.

Auston

· Revenue from Auston increased 10% YOY to $5.4 million in FY25 (FY24: $4.9 million). The progression of students to bachelor's degree programs drove revenue growth, while the acquisition of new students was subdued as a result of various external factors.

· Student enrolment grew 5% from 30 September 2024 to circa 860 at 30 September 2025. The slow growth is attributable to slow sales from the extended closure of the Mandalay campus after the earthquake in March 2025. Increased migration driven by conflict, the earthquake, and conscription fears, added significant complexity and impacted the overall commercial performance.

· The Group responded by strengthening its management team with experienced leadership and Auston managed to navigate the disruptive and challenging period with limited impact.

· Auston has signed an academic partnership agreements with the University of Wolverhampton in December 2025 and University College Birmingham in February 2026 and obtained Pearson BTEC certification in May 2025, ensuring continuity and a path for Auston's students. Auston is exploring further collaboration opportunities with reputable institutions across the world to expand its product offering horizontally (across disciplines) and vertically (post-graduate programs).

· At 30 September 2025, Auston operated campuses in Mandalay and Yangon, with plans to expand usable space and enhance facilities in Yangon over the next two years.

SERVICES

The Group's objective is to leverage our security expertise and facility management services to become the trusted regional partner for corporates.

Revenue from Services businesses increased 2%YOY to $7.1 million in FY25 (FY24: $7.0 million).

At 30 September 2025, deferred revenue from Services businesses, representing cash received in advance of service delivery, was:

- Current: $0.3 million (30 September 2024: $0.3 million)

- Non-Current: nil (30 September 2024: nil)

Within its Services division, the Group operates two brands across Myanmar and Vietnam:

EXERA is the leading provider of risk management, consulting, integrated security, manned guarding, secure logistics, facility management, and cash-in-transit services in Myanmar. It serves a wide range of international and local clients across Myanmar and holds ISO 18788, ISO 9001, ANSI/ASIS PSC.1 certifications, and ICoCA membership. In Vietnam, it is a start-up focused on integrated facility management services.

Ostello Bello is a boutique hostel brand known for its vibrant social atmosphere and exceptional hospitality. Ostello Bello operates in some of the most popular tourist destinations across Italy and Myanmar.

Vietnam

EXERA Vietnam

· EXERA Vietnam was launched in FY24 to provide integrated facility management services and generated $61k revenue in FY25 from its first few customers. However, the business has been slow to scale, and the Group is exploring strategic partnerships to increase market penetration.

Myanmar

EXERA Myanmar

Revenue from EXERA Myanmar increased 1% YOY to $7.1 million in FY25 (FY24: $7.0 million).

· Market dynamics have shifted as EXERA secures more local corporate clients. With customers increasingly seeking cost savings, repricing has proven more challenging than expected. Nevertheless, EXERA Myanmar has retained key large clients and achieved growth through increased sales of risk reporting packages.

· EXERA employed over 1,900 security officers as of 30 September 2025 (30 September 2024: circa 1,710) across circa 250 sites (30 September 2024: circa 230 sites) in Myanmar.

Ostello Bello

· Ostello Bello, a managed business in the Services division, operates one boutique hostel in Bagan, Myanmar, with circa 40 beds and circa 12 rooms. No revenue was generated in relation to hostel-related services in FY25 (FY24: $10k).

· The devastating earthquake in Mandalay forced the Group to make the difficult decision to close the Mandalay hostel, which had previously served as both a hub for local tourists and an internal coordination centre for our operations in the region for ten years.

FINANCIAL REVIEW

RESULTS OF OPERATIONS

Revenue grew 8% YOY to $32.1 million in FY25 (FY24: $29.7 million). The revenue growth was a result of robust expansion in Myanmar across the Education businesses (FY25: 19% YOY) and Services businesses (FY25: 1% YOY). Revenues decreased in Vietnam's Education businesses (FY25: -6% YOY) as the drop at Wall Street English Vietnam was not fully covered by the growth at Kids&Us Vietnam, Logiscool Vietnam, and EXERA Vietnam.

$ | FY25 | FY24 | FY23 |

Education - Vietnam | 7,720,079 | 8,229,656 | 8,539,813 |

Wall Street English | 6,686,568 | 7,631,372 | 8,254,131 |

Kids&Us | 923,229 | 575,519 | 285,682 |

Logiscool | 110,282 | 22,765 | − |

Education - Myanmar | 17,250,190 | 14,441,789 | 10,162,576 |

Wall Street English | 8,198,732 | 7,744,204 | 6,860,636 |

Kids&Us | 854,603 | 416,064 | 24,632 |

Logiscool | 1,003,583 | 148,726 | − |

Yangon American | 1,795,032 | 1,230,966 | 887,196 |

Auston | 5,398,240 | 4,901,829 | 2,390,112 |

Education | 24,970,269 | 22,671,445 | 18,702,389 |

Services | |||

EXERA | 60,787 | 3,576 | - |

EXERA | 7,071,011 | 6,988,643 | 5,327,189 |

Ostello Bello | - | 10,351 | - |

Services | 7,131,798 | 7,002,570 | 5,327,189 |

Total | 32,102,067 | 29,674,015 | 24,029,578 |

|

|

All Education businesses, except Wall Street English Vietnam, recorded strong revenue growth. Auston is quickly becoming a key contributor to Group revenue. Investments in Yangon American, as well as Kids&Us and Logiscool, will drive more meaningful growth in the years ahead.

The Services division saw modest growth as the Myanmar business strengthened its commercial position and expanded its high-value service offerings. EXERA Vietnam has begun to generate income in FY25 and is exploring strategic partnerships to scale. The Group is evaluating strategic partnership opportunities to strengthen and scale the business, particularly in Vietnam.

Group gross profit rose 11% YOY to $18.9 million in FY25 (FY24: $17.0 million), with the Education division contributing 94% (FY24: 91%) and the Services division 6% (FY24: 9%). An improvement in the Education division gross margin at 71% (FY24: 68%) was offset by a deterioration in the Services division gross margin at 16% (FY24: 23%).

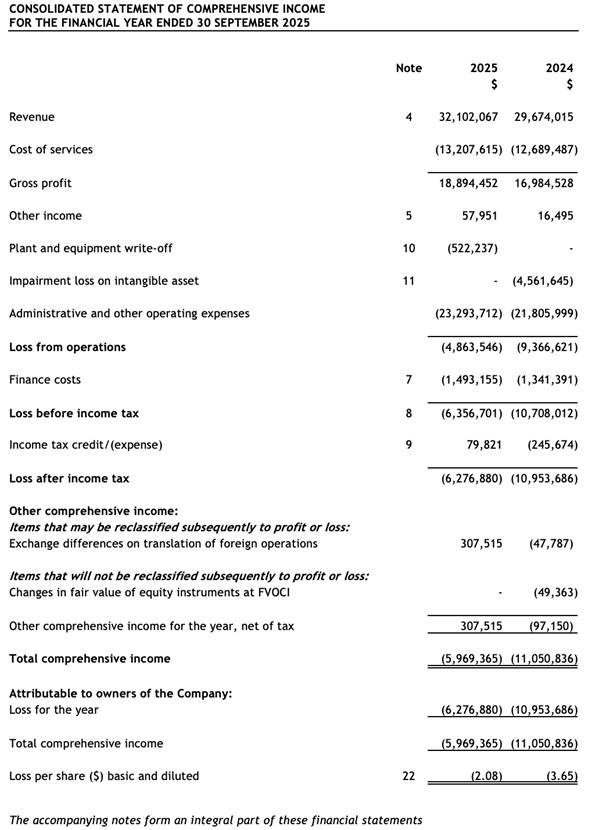

The Group's net loss narrowed to $6.3 million in FY25 (FY24: $11.0 million), reflecting the absence of the one-time $4.6 million goodwill impairment at Wall Street English Vietnam recorded in FY24. The main cause of the losses in FY25 was a foreign exchange loss of $2.8 million, due to heightened currency volatility in key markets, and a plant and equipment write-off of $0.5 million, due to earthquake damage. Despite this, operating expenses were effectively controlled, increasing only 1% YOY, underscoring management's disciplined cost management as new businesses scale and mature operations become more efficient.

$ | FY25 | FY24 | FY23 |

Revenue | 32,102,067 | 29,674,015 | 24,054,547 |

Cost of services | (13,207,615) | (12,689,487) | (10,184,215) |

Gross profit | 18,894,452 | 16,984,528 | 13,870,332 |

Gross profit margin | 59% | 57% | 58% |

| |||

Other income | 57,951 | 16,495 | 90,018 |

Foreign exchange loss | (2,794,062) | (1,455,135) | (1,134,441) |

Impairment loss on intangible assets | − | (4,561,645) | − |

Plant and equipment write-off | (522,237) | − | − |

Administrative and other operating expenses | (20,499,650) | (20,350,864) | (17,098,388) |

Loss from operations | (4,863,546) | (9,366,621) | (4,272,479) |

Finance cost | (1,493,155) | (1,341,391) | (979,791) |

Loss before income tax | (6,356,701) | (10,708,012) | (5,252,270) |

Income tax credit/(expense) | 79,821 | (245,674) | (67,414) |

Loss after income tax | (6,276,880) | (10,953,686) | (5,319,684) |

Selected non-cash items: | |||

Total depreciation of plant and equipment | 1,301,998 | 1,207,028 | 826,953 |

Total amortisation on of right-of-use asset | 2,683,325 | 2,786,093 | 2,858,275 |

Total amortisation on of intangible assets | 102,741 | 100,718 | 80,498 |

Impairment on/(reversal of) trade and other receivables |

3,008 |

− |

(9,514) |

Impairment loss on intangible assets | − | 4,561,645 | − |

Plant and equipment writte-off | 522,237 | − | − |

Finance costs (excluding interest on lease liabilities) |

224,802 |

220,416 |

105,748 |

Total interest on lease liabilities | 1,268,353 | 1,120,975 | 875,405 |

6,106,464 | 9,996,875 | 4,737,365 | |

Adjusted EBITDA1 | (250,237) | (711,137) | (514,905) |

|

|

| |

Adjusted EBITDA after impact of ROUs * | (4,201,915) | (4,618,205) | (4,248,585) |

|

1Key performance indicators for the Group, based on earnings before interest, income tax, depreciation and amortisation ("EBITDA"), are (i) Adjusted EBITDA (as presented above) and (ii) Adjusted EBITDA less amortisation of right-of-use assets and interest on lease liabilities ("Adjusted EBITDA after impact of ROUs").

Group adjusted EBITDA (excluding impairment losses and interest on lease liabilities) loss amounted to $0.3 million in FY25 (FY24: $0.7 million loss). Narrowing losses at Wall Street English Vietnam and the growth of start-up businesses were partly offset by higher foreign exchange losses. Marketing expenses decreased $0.4 million YOY to $3.1 million in FY25, reflecting improved spending efficiency amid stronger sales activity. Overall, underlying operational performance strengthened as cost control measures and improved performance at start-up businesses took effect.

Employees increased to circa 2,780 at 30 September 2025 (30 September 2024: circa 2,600). The increase in headcount is directly linked to the school portfolio expansion in both countries and the acquisition of additional sites under EXERA Myanmar.

CASH FLOW EVOLUTION

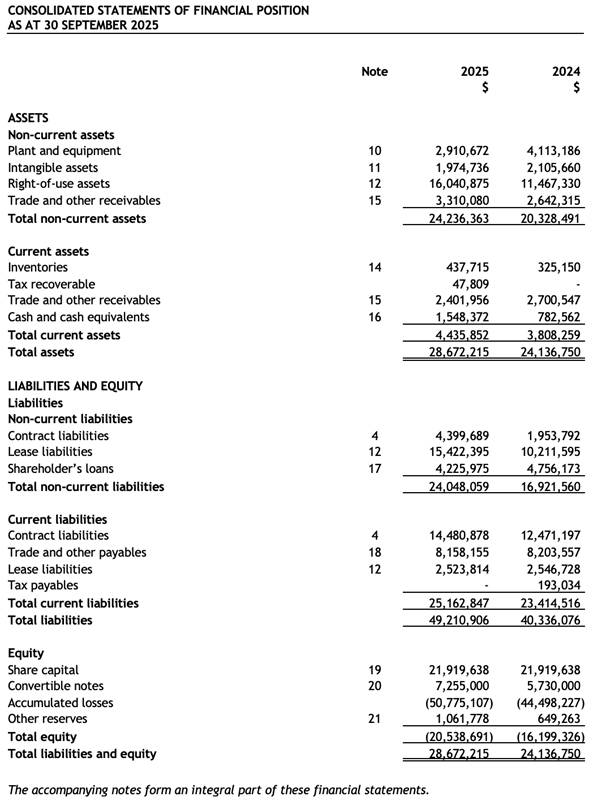

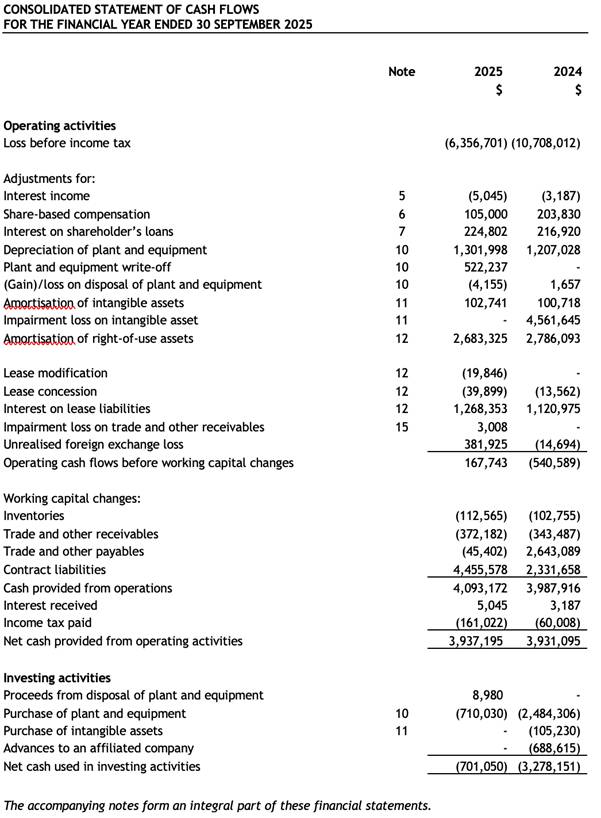

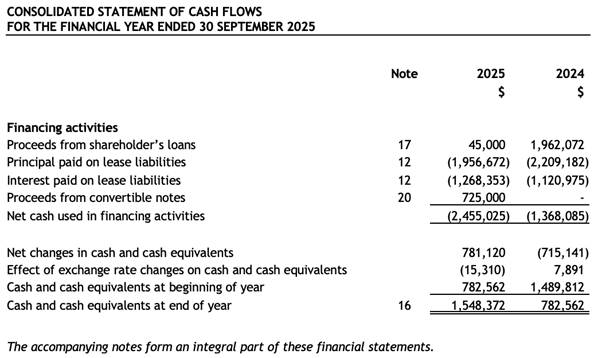

At 30 September 2025, the Group's cash and cash equivalents position was $1.5 million (30 September 2024: $0.8 million). The positive change resulted from the combination of (i) a $3.9 million inflow from operating activities, (ii) a $0.7 million outflow from investing activities, and (iii) a $2.5 million outflow from financing activities.

The Group generated cash inflow from operating activities of $3.9 million in FY25 (FY24: inflow $3.9 million). Operating cash flow before working capital changes in FY25 was $0.2 million (FY24: negative $0.5 million). If repayment of lease liabilities of $3.2 million (FY24: $3.3 million) were considered, adjusted cash inflow from operating activities would have been positive $0.7 million (FY24: positive $0.6 million).

The Group incurred cash outflow from investing activities of $0.7 million in FY25 (FY24: outflow $3.3 million), of which $0.7 million (FY24: $2.5 million) was spent on leasehold improvements for the opening of (i) one school in Vietnam (Logiscool), (ii) four schools in Myanmar (Kids & Us / Logiscool), and (iii) the Auston campus expansion.

Cash outflow from financing amounted to $2.5 million in FY25 (FY24: outflow $1.4 million), of which repayment of lease liabilities totalled $3.2 million (FY24: $3.3 million). Cash inflow from financing, before repayment of lease liabilities, was $0.8 million in FY25 (FY24: inflow $2.0 million), which comprised of proceeds from a shareholder's loan of $45k (FY24: $2.0 million) and convertible notes of $0.7 million (FY24: nil). The finances were utilised primarily to open new schools and support the operating losses for the expansion of selected new ventures (Kids&Us, EXERA VN and Logiscool VN).

DIVIDENDS

The Board of Directors does not recommend paying dividends for FY25 as the Group needs to conserve cash for working capital and future expansion.

LIQUIDITY MANAGEMENT AND GOING CONCERN

The Board of Directors have carried out a detailed review of the Group's cash flow forecast for twenty -four months from 30 September 2025 and specifically considered a going concern review period of 12 months from the date of this report. This forecast considered the time needed for new and non-performing businesses to turn profitable. The Group conducted extensive stress testing on various scenarios calibrating the duration it might take for these businesses to improve as well as other items impacting future performance, such as the general macroeconomic environment and initiatives within the management's control.

The Board of Directors determined management has control over sufficient mitigating actions to manage cash outflow, such as prioritising capital expenditures, reducing operational activities of non−performing business divisions and pausing discretionary spending. Other key considerations included:

a) The Group meticulously plans its business expansion and continuously monitors how changes to the political and economic environment may potentially impact its business operations, particularly in Myanmar. Since FY23, the overall Myanmar businesses have been self-sustaining requiring no financial support;

b) Negative cash conversion cycle for many businesses as tuition fees and certain risk management services are generally collected up to twelve months in advance of service delivery. Refer to Note 4 of the financial statements for further details;

c) Support by franchise partners through flexible payment plans in relation to franchise fees and didactic materials;

d) Flexible discretionary capital spending as any capital expenditures in Myanmar would be funded through excess capital earned locally; and

e) Access to the unutilised Loan Facility as disclosed in Note 17 of the financial statements.

Established businesses within the Education and Services divisions in Myanmar generate sufficient cash flow to support the existing operations and their expansion. Management expects this trend to continue for the foreseeable future.

In Vietnam, the macroeconomic outlook has continued to improve in 2025 and we anticipate further growth from businesses as new schools continue to open and new brands gain traction.

Therefore, at the date of this report, the Directors have concluded that the Group has adequate financial resources to cover its working capital needs for at least the next twelve months.

OUTLOOK

Asia Strategic Holdings is steadfast in leveraging its integrated operating model and in-house shared service functions to deliver sustainable returns to shareholders. Significant financial and human capital investments over the past years have established a competitive portfolio of businesses. This portfolio balances mature, profitable anchors with greenfield projects poised to drive the next phase of growth.

Capital Allocation and Strategic Focus

The Group employs a disciplined capital allocation strategy to support its long-term vision:

· Portfolio and balance sheet strength: balancing time and resources in the organic growth of existing brands to drive sustainable expansion while maintaining a resilient financial position.

· Geographic and sectoral expansion: leveraging shared service functions and a regional management approach to unlock synergies, particularly in new markets.

· Investment prioritisation: minimal and prudent capital expenditures focused on utilising existing locations and adopting a strategic real estate framework to enable brands to achieve their potential.

Continued Development of Existing Brands

Partnerships with international market leaders, such as Kids&Us, Logiscool and Wall Street English, provide a strong foundation for organic revenue growth. Turning around Wall Street English Vietnam remains a top priority, with efforts focused on operational maturity to deliver meaningful cash flow contributions and support future expansion.

The Group is also actively enhancing the programmes at Auston and Yangon American, ensuring students benefit from best-in-class education that equips them for academic and professional success. These improvements aim to strengthen the institutions' competitive edge and reinforce their reputations as leading providers of high-quality education.

Navigating Macroeconomic Conditions and Demographic Shifts

The Group expects a less volatile macroeconomic environment, supported by more stable foreign exchange rates, broader economic growth, and favourable demographic trends such as growing middle classes and young, urbanising populations. Rising foreign direct investment and the region's emergence as a tech hub are driving demand for education, skilled labour, and services. These dynamics align with the Group's strategy to address skills gaps through tech-enabled education and complementary offerings while positioning itself as a key regional partner to corporates, and organisations.

Commitment to Strategic Growth

Asia Strategic Holdings remains committed to expanding its footprint in emerging markets through targeted investments that align with its core strategy. While focusing on current operations, the Group will evaluate new opportunities, particularly those in high-impact sectors such as education, which complement its existing businesses and align with regional development trends.

With an eye on long-term opportunities and a prudent approach to immediate challenges, the Group is well-positioned to navigate the year ahead with resilience, delivering value for shareholders while supporting sustainable economic and social development in the markets it serves.

NOTES TO THE FINANCIAL STATEMENTS

NOTES TO THE FINANCIAL STATEMENTSFOR THE FINANCIAL YEAR ENDED 30 SEPTEMBER 2025

These notes form an integral part of and should be read in conjunction with the accompanying financial statements.

1. General

Asia Strategic Holdings Limited (the "Company" or "Asia Strategic") (Registration Number 201302159D), is a public company limited by shares incorporated and domiciled in Singapore with its principal place of business and registered office at 80 Raffles Place #32-01, UOB Plaza, Singapore 048624. The Company was listed on the Main Market of London Stock Exchange on 22 August 2017.

The principal activities of the Company are management services to its subsidiaries followed by developing, managing, operating and investing in businesses across Emerging Asia. The principal activities of the subsidiaries are set out in Note 13 to the financial statements. Related companies in these financial statements refer to members of the Group.

2. Material accounting policies

2.1 Basis of preparation

The financial statements have been prepared in accordance with International Financial Reporting Standards ("IFRSs") as adopted by the European Union and are prepared under the historical cost convention, except as disclosed in the accounting policies below.

The individual financial statements of each Group entity are measured and presented in the currency of the primary economic environment in which the entity operates (its functional currency). The consolidated financial statements of the Group are presented in United States Dollar ("$") which is the functional currency of the Company and the presentation currency for the consolidated financial statements.

The preparation of financial statements in compliance with IFRS requires management to make judgements, estimates and assumptions that affect the Group's application of accounting policies and reported amounts of assets, liabilities, revenue and expenses. Although these estimates are based on management's best knowledge of current events and actions, actual results may differ from those estimates. The areas where such judgements or estimates have significant effect on the financial statements are disclosed in Note 3 to the financial statements.

Myanmar political and economic situation

The business environment in major cities where the Group operates such as Yangon and Mandalay remain active yet challenging due to (i) the recent earthquake in Mandalay (ii) frequent power and telecommunication outages, (iii) trade restrictions at the border, resulting in inflationary pressure, and (iv) security risks. The political and economic situation evolves daily and is expected to improve after the upcoming elections.

Impact of the Myanmar earthquake and business continuity

On 28 March 2025, a 7.7 magnitude earthquake struck central Myanmar, prompting the National Disaster Management Committee to declare a State of Emergency across the affected regions, including Sagaing, Mandalay, Magway, Bago, and northeastern Shan State. The earthquake caused widespread disruption to electricity, internet connectivity, water supply and sanitization services. In response, several countries, including China, India, the United States and various ASEAN and European nations, have extended financial aid and humanitarian relief.

Myanmar has now transitioned into the recovery phase. However, many families remain displaced in temporary shelters or rental housing due to structural damage and safety concerns. The humanitarian response remains ongoing, with coordinated efforts from national authorities, UN agencies, and international NGOs focused on shelter, health, food security, and infrastructure rehabilitation. Long-term recovery planning is underway, though sustainable housing solutions and economic revitalisation remain key challenges.

While the earthquake had a negligible impact on the Group's corporate offices and operations in Yangon, the premises of Wall Street English, Logiscool, Auston, and Ostello Bello in Mandalay were significantly affected and were closed from April 2025 until November 2025. No casualties or serious injuries were reported as a result of the damage to our schools, hostel, and offices.

Prior to the resumption of physical classes, English language programs, coding courses, and university lectures were fully delivered online, minimising operational disruption. For affected students without internet and/or electricity access, the Group implemented support measures such as study breaks and course extensions. In July, Auston resumed university lectures in a temporary campus.

While the buildings were structurally safe, extensive repairs and refurbishments were required. Significant judgements were made on the impact assessment, resulting in the write-off of the carrying amounts of non-movable items such as leasehold improvements and furniture & fittings for these sites, totaling $522,237 (Note 10).

In November 2025, Wall Street English, Logiscool and Auston's existing sites in Mandalay were refurbished and re-opened. On the other hand, Management decided to discontinue operations at the managed hostel, coinciding with the expiration of the ten-year operation and management agreement.

Despite a challenging macroeconomic environment, demand for quality education remained resilient, underscoring the essential role our education division play in communities with limited alternatives. Our Group's Services division demonstrated its critical importance during the recent earthquake, providing vital support in emergency response operations and safeguarding embassies, client facilities, and key infrastructure. The Group continuously monitors and applies appropriate mitigating actions to ensure the operations in Myanmar remain flexible and adaptable to the market environment.

As part of the Group's risk management protocols, cash balances in Myanmar are limited to the minimum required to maintain operations. While the Group remains focused on expanding its current operations in Vietnam, the contribution from both markets remains an important diversification strategy to mitigate the overall geographical risk exposure of the Group.

Other than as disclosed above, the Group has considered the current market environment in the respective countries in which it operates as at the reporting date and notes that there are no indicators that warrant material adjustments to the key estimates and judgements on the recoverability of any assets. The significant estimates and judgements applied are as disclosed in Note 3 to the financial statements.

Going concern assumption

Including the one-off plant and equipment write-off of $522,237 (Note 2.1), the Group recorded loss for the year of $6,276,880. As at reporting date, the Group's current liabilities and total liabilities exceeded its current assets and total assets by $20,726,995 and $20,538,691 respectively. Net current liabilities, excluding contract liabilities (non-cash item) amounted to $6,246,117.

The Board of Directors have carried out a detailed review of the Group's cash flow forecast for twenty-four months from the financial year ended 30 September 2025 and specifically considered a going concern review period of 12 months from the date of this report.

The cash flow forecast has been prepared and stress-tested taking into consideration the timing of capital expenditures, the general political and macroeconomic environment and other information available at the end of the reporting period. The Directors have evaluated that there are sufficient mitigating actions within their control, such as further optimising the Group's operations, adjustments to operating expenses, and prioritising Group's capital expenditures focusing on multi brand sites driving operational efficiency and synergies.

Other key considerations in the assessment include, among others:

a) The Group develops a detailed business expansion plan and continuously monitors environmental changes that may impact its business operations, particularly in Myanmar. For the past few years, the Myanmar-based businesses have been self-sustainable;

b) The Group has access to $818,000 in unutilised loan facility as disclosed in Note 17 to the financial statements;

c) Tuition fees and certain security services are generally collected up to twelve months in advance of performance with reference to the terms of the contracts. Refer to Note 4 for further details;

d) The Group's net cash generated from operating activities amounted to $712,000 (net of repayments of principal and interest on lease liabilities) during the current financial year;

e) In support of the Group's expansion strategy, the Group entered into a payment plan with a key vendor, subsequent to the financial year end. As at 30 September 2025, the outstanding balances owed to the vendor was $2,334,000. Interest at 4% per annum accrues daily, on any outstanding balances from 1 October 2025. The arrangement matures at 30 September 2027, at which point the Group may settle the obligation or, subject to mutual agreement, further extend the repayment terms; and

f) Control over the timing and size of capital expenditures as all expansionary expenditures are discretionary in nature. Any capital expenditures in Myanmar would be funded by excess capital available locally, if any.

The Directors have assessed the Group's cash flows, forecasts, planned investments, cash resources, and loan facilities, and are satisfied that sufficient resources exist to continue operations for the foreseeable future. No material uncertainties have been identified that may cast significant doubt on the Group's ability to continue as a going concern. Therefore, the financial statements have been prepared on a going concern basis.

Changes in accounting policies

New standards, amendments and interpretations effective from 1 October 2024

On 1 October 2024, the Group adopted the new or amended IFRS and interpretations to IFRS that are mandatory for application for the financial year. The adoption of these standards did not result in significant changes to the Group's accounting policies and had no material impact to the Group's financial statements.

IFRSs issued but not yet effective

At the date of authorisation of these financial statements, the following IFRSs were issued, but not yet effective, and have not been early adopted in these financial statements:

| Standard or interpretation | Description | Effective date (annual periods beginning on or after) |

| IAS 21 (Amendments) | : Lack of Exchangeability | 1 January 2025 |

| IFRS 7, 9 (Amendments) | : Amendments to the Classification and Measurement of Financial Instruments | 1 January 2026 |

| IFRS 7, 9 (Amendments) | : Contracts Referencing Nature-dependent Electricity | 1 January 2026 |

| IFRS 19 (Amendments) | : Subsidiaries without Public Accountability: Disclosures | 1 January 2027 |

| IFRS 18 | : Presentation and Disclosure in Financial Statements | 1 January 2027 |

Consequential amendments were also made to various standards as a result of these new or revised standards.

Except as disclosed below, the Group anticipates that the adoption of the above standards if applicable, will have no material impact on the financial statements of the Group in the period of their adoption.

IFRS 18 Presentation and Disclosure in Financial Statements

IFRS 18 replaces IFRS 1 Presentation of Financial Statements and provides guidance on presentation and disclosure in financial statements, focusing on the statement of profit or loss.

IFRS 18 introduces:

· New structure on statement of profit or loss with defined sub-totals;

· Disclosure related to management-defined performance measures ("MPMs"), which are measures of financial performance based on a total or sub-total required by accounting standards with adjustments made (e.g. 'adjusted profit or loss'). A reconciliation of MPMs to the nearest total or sub-total calculated in accordance with accounting standards; and