24th Mar 2026 07:00

Embargoed: 24 March 2026

ITACONIX PLC

("Itaconix" or the "Company")

PRELIMINARY RESULTS FOR THE YEAR ENDED 31 DECEMBER 2025

Our most successful year into a new stage of development and growth

Itaconix (AIM: ITX) (OTCQB: ITXXF), a leading innovator in high-performance plant-based specialty polymers, is delighted to announce its Preliminary Results for the year ended 31 December 2025.

Financial and Operational Highlights

| 2025

$'000 | 2024 (Restated) $'000 | 2023

$'000 | 2022

$'000 | 2021

$'000 |

Revenue | 10,499 | 6,503 | 7,866 | 5,600 | 2,596 |

Gross profit | 3,642 | 2,260 | 2,437 | 1,487 | 700 |

Gross profit margin | 34.7% | 34.7% | 31.0% | 26.6% | 27.0% |

Adjusted EBITDA1 | (600) | (1,778) | (925) | (1,395) | (1,640) |

Cash used from operating activities | (1,222) | (2,753) | (1,923) | (219) | (2,023) |

Net cash and investments at year-end | 4,391 | 6,734 | 10,023 | 597 | 683 |

1 Adjusted for interest, tax, depreciation, amortisation, share based payment charge, and exceptional items.

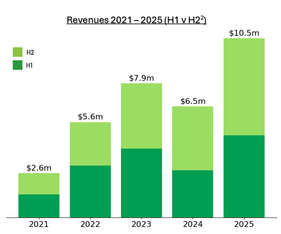

Record annual revenues surpassed $10m for the first time, reflecting 61% year-on-year growth.Annual gross profit surpassed $3m for the first time. Maintained overall gross profit margin of 35%, with gross profit margin in core Itaconix Performance Ingredients business at 41%.Adjusted EBITDA losses improved to $0.6m, from $1.8m in 2024.Net losses declined to $1.4m in 2025 from $2.0m in 2024.Ended the year with strong working capital position for growth.Itaconix® Performance Ingredients and SPARX™ Formulated Solutions businesses on strong paths towards profitable long-term growth.Development of BIO*Asterix® specialty itaconate monomers and resins business into large new revenue opportunity. Launch of BIO*Asterix® ecommerce site (www.bioasterix.com) in July 2025.Leveraged the performance advantages of scale inhibitors through the SPARX™ Formulated Solutions program, to develop new unit dose detergent formulations for 17 North American brands.Several new ingredients in pre-commercial or early commercial stages.The Company has entered 2026 with strong order momentum and a growing pipeline of projects. Management's expectations for the year to 31 December 2026 remain unchanged, with strong forecast revenue growth and positive adjusted EBITDA*.

* The Board believes the current market expectations for the year ended 31 December 2026 are as follows: Revenue - $13.3m, Adjusted EBITDA - $0.3m, Net cash - $3m

1 Adjusted for interest, tax, depreciation, amortisation, share based payment charge, and exceptional items.

2 Unaudited revenues by reporting period.Commenting on the outlook, John R. Shaw, CEO of Itaconix said:

"Achieving $10.5m in revenues is a major milestone towards our goal of developing a large, highly profitable, capital efficient specialty ingredient company.

We sell proprietary ingredients that consumer product brands increasingly want to use for their safety, performance, affordability, and sustainability. Our commercial traction, diverse revenue base, customer project pipeline, and production capacity put us in position for continued growth into a solid foundation of profitability for both generating shareholder value and pursuing additional revenue horizons.

Reaching this position while navigating geopolitical turmoil underscores the strength of our business and the resilience of our supply chain, our operations, and our organisation to global uncertainties.

We are off to a strong start in 2026 and remain confident that we will meet the management expectations, including a clear path to positive adjusted EBITDA in 2026."

- Ends -

Itaconix plc John R. Shaw / Laura Denner | +1 603 775-4400 |

Rosewood John West / Llewellyn Angus / Lily Pearce | +44 (0)20 7653 8702 |

Canaccord Genuity - Nominated Adviser and Sole Broker Adam James / Harry Pardoe | +44 (0) 20 7523 8000 |

About Itaconix

Itaconix uses its proprietary plant-based polymer technology platform to produce and sell specialty ingredients that improve the safety, performance, and sustainability of consumer products. The Company's current ingredients are enabling and leading new generations of cost-effective, decarbonized consumer products in home and personal care.

www.itaconix.com

Report & Accounts and Notice of AGM

The Company's statutory accounts for the year ended 31 December 2025, together with a Notice of Annual General Meeting, are available on the Company's website (www.itaconix.com) and posted to shareholders on 24 March 2026. Copies will also be available at the Company's registered office, Fieldfisher LLP, 9th Floor, Riverbank House, 2 Swan Lane, London EC4R 3TT, United Kingdom.

The Annual General Meeting is due to be held at 14:00 BST on 14 May 2026 at Fieldfisher LLP, 9th Floor, Riverbank House, 2 Swan Lane, London EC4R 3TT, United Kingdom.

CHAIR'S STATEMENT

For Nature with Nature

Itaconic acid is a natural biological material generated in the human and plant world. Prior to the founding of Itaconix, it was utilised mainly at low percentages for the beneficial functional properties it added to polymeric binders used in carpet backing and high-quality paper, where it is still used. It is produced at large scale by industrial fermentation using plant-based feedstock and is widely available on the open market.

We have a broad technology platform, protected by 18 patent families. We use the beneficial functionality of itaconic acid to produce proprietary polymeric ingredients that can offer significant safety, performance, cost, and sustainability advantages over alternative ingredients. Our ingredients enable plant-based solutions for new generations of cutting-edge consumer products.

We had a great year. But more importantly we have decades of potential for our current and future proprietary ingredients to enable better solutions across broad ranges of consumer and industrial products. We will supply key ingredients for new generations of end-use products that are better and safer by how they are produced, how they are used, how they perform, how much they cost, how they interact with animals, and how they do not persist in the environment. We will steadily capture this potential without placing costly burdens on consumers and society.

Our Business Plan

Our goal is to build a large, highly profitable company with re-occurring revenues from a diverse base of customers that purchase Itaconix products as key enabling ingredients in new generations of end-products.

Our immediate objective is to organically establish a sound and sustainable financial foundation that will generate cash from operations to fund long-term growth, ongoing innovation, and shareholder returns.

To achieve this foundation, we have narrowed our near-term commercial focus on consumer product applications where Itaconix ingredients offer the most immediate opportunities for brands to succeed with new products. The multi-functional advantages of our itaconate ingredients can offer extraordinary value in the unit dose segments of the consumer laundry and dishwashing detergent markets. This is a multibillion-dollar market where we have established success and are gaining broader recognition within brands of the competitive advantages our ingredients offer in detergent capsules, tablets, and sheets.

We believe that our base of existing customers and current pipeline of new customer projects in unit dose detergents will drive us to the financial foundation we have targeted to expand into broader applications and execute our business plan to build a large, highly profitable company.

2025

I encourage you to read the details provided throughout this Annual Report on the broad and substantial progress we achieved in 2025 toward both establishing a sound financial foundation and generating commercial traction to propel our near-term and long-term growth.

We surpassed $10m in revenues for the first time. We did so with 61% year-on-year growth and consecutive growth in half-year revenues. We maintained overall gross profit margin of 35% in 2025, with gross profit margin in our core Itaconix® Performance Ingredients business at 41%. Adjusted EBITDA losses improved from $1.8m in 2024 to $0.6m 2025. Net losses declined to $1.4m in 2025 from $2.0m in 2024.

We continued to judiciously use our cash resources to invest in our customer pipeline through new marketing capabilities, new products, additional product studies, global regulatory approvals, better production, and organisation development to support our growth.

Summary

2025 marked our most successful year into a new stage of development and growth. Our Itaconix® Performance Ingredients and SPARX™ Formulated Solutions businesses are on strong paths towards profitable long-term growth. We took important steps towards developing our BIO*Asterix® specialty itaconate monomers and resins business into a large new revenue opportunity. We remain focussed on our organic near-term financial foundation for funding our long-term objectives and potential.

Our progress is occurring in a global environment with significant uncertainties. Views and regulations on the relative safety of chemicals are fragmenting between consumer market segments and across geographies. Our purchases of key raw materials and the sales of our ingredients face risks from political acts that disrupt trade flows and consumer purchasing. As we monitor and manage these forces to meet the strong underlying needs for our ingredients, we are confident that Itaconix will create value for our customers, retail consumers, the environment, our employees, and our shareholders.

Peter Nieuwenhuizen

Chair

CHIEF EXECUTIVE OFFICER'S STATEMENT

Introduction

Achieving $10.5m in revenue marks an important milestone in the development towards a large, highly profitable, capital efficient, specialty ingredients business.

We are structuring and building our revenues for long-term success with products that are valued and purchased for their performance, that are used across a broad range of customers and applications, and that enable new generations of safer and more sustainable consumer products. With our new SPARX™ Formulated Solutions programme, we work closely with other innovators to speed the introduction of new consumer products that address valuable unmet needs.

Reaching this milestone, while navigating global economic and geopolitical pressures, underscores the attractiveness of our products as well as the resilience and adaptability of our organisation, our operations, and our supply chain.

In my Chief Executive Officer's statement in our 2024 Annual Report, I outlined four non-financial key performance indicators through 2026 to guide Itaconix toward near-term profitability while expanding our long-term revenue potential. I am pleased to report that we have made substantial progress across all four indicators.

Expand European cleaning revenues with broader adoption for scale inhibition

We grew our Performance Ingredient revenues in Europe, Middle East, and Africa ("EMEA") to $3.9m in 2025, up from $1.9m in 2024, representing 104% year-on-year growth. This increase was driven primarily by increased adoption of our scale inhibitors in unit dose dishwashing detergents, both among existing and new customers. Looking ahead, we remain confident that our strong pipeline of EMEA detergent projects will continue to deliver attractive growth from both current and potential customers.

Re-land North American cleaning revenues for scale inhibition at attractive pricing

We leveraged the performance advantages of our scale inhibitors through our SPARX™ Formulated Solutions programme to develop new unit dose detergent formulations for 17 North American brands. So far, eight formulations went into production in 2025, another seven are expected to go into production in 2026 and two remain in evaluation. The success these formulations are delivering for both brands and contract manufacturers is driving broader adoption of our Itaconix® TSI™ polymers as a key ingredient in next generation unit dose dishwashing detergents.

We anticipate that our current pipeline of North American dishwashing detergent projects will support another strong year of growth in scale inhibitor and SPARX™ Formulated Solutions revenues in 2026.

Land and expand North American odour neutralisation revenues in broader home and industrial applications

Through our SPARX™ Formulated Solutions programme, we successfully expanded the use of our odour neutralising ingredients in unit dose fabric care applications. These ingredients are now incorporated into five new unit dose fabric care detergent formulations in production, or slated for production, at contract manufacturers for five North American brands. While the majority of these formulations target pod and tablet formats, we also achieved initial success in the laundry sheet category.

In 2025 we built a robust pipeline of North American fabric care detergent projects, which we expect to translate into substantial revenues through 2027. Additionally, we renewed our supply agreement with Croda, contributing to increased revenues in 2025, with further growth anticipated in 2026.

Gain initial traction for BIO*Asterix® specialty monomers and binders

We advanced the availability and visibility of our specialty itaconate esters with the launch of our BIO*Asterix® ecommerce site (www.bioasterix.com) in July 2025. These esters hold significant potential for the development of new plant-based resins in paints and coatings, and we are excited to initiate the long-term development of BIO*Asterix® into a substantial business. The ecommerce site has successfully generated awareness and enquiries regarding our itaconate ester offerings and capabilities. We currently offer four itaconate esters in millilitre volumes to industrial and academic research laboratories, with additional itaconate materials planned for future release. As expected, revenues remain modest at this stage.

Our commercial progress and potential are outlined below, with full financial results detailed in the Financial Review.

Financial Foundation from Consumer Unit Dose Detergent Markets

My Chief Executive Officer's statement in our 2024 Annual Report also outlined seven applications areas where our technology platform provides alternatives to acrylic acid polymers, leveraging advantages in chemical functionality.

Within this range of potential applications, our scale inhibitors and odour neutralisers are gaining strong traction in unit dose dishwashing and fabric care detergents, driven by their ability to deliver better performance, affordability, and sustainability.

The consumer unit dose detergent market has favourable dynamics for Itaconix to grow over at least the next five years. The broader consumer detergent market provides re-occurring revenues and growth opportunities across both developed countries and emerging regions, where adoption of laundry and dishwashing machines continues to expand. Unit dose formats, such as capsules, tablets, and sheets, are outpacing overall detergent growth, reflecting evolving consumer preferences and performance advances.

Our polymers offer multi-functional advantages that are especially valuable in formulating compact unit dose detergents with performance and cost advantages.

Unit dose detergents represent a strong pathway to profitability and innovation, supporting our long-term growth strategy. We remain focused on direct selling and technical support to guide brands and contract manufacturers toward optimal formulations. This approach yielded significant success in 2025, and we believe our current customer base and project pipeline will provide a solid foundation to sustain both profitability and innovation.

With ongoing improvements and upgrades to our US operations, we have the capacity to provide the technical support and production capacity to reach at least $30m in revenues, with limited investment required to support additional revenues thereafter.

Decades of Potential

As we establish our first substantial profitable revenue base in consumer detergents with our current ingredients, our technology platform continues to present significant opportunities to enhance the safety, performance, and sustainability of itaconate polymers.

We have several new ingredients in pre-commercial or early commercial stages and are carefully prioritising where and how to develop additional large, profitable revenue streams from these innovations.

BIO*Asterix® specialty monomers and binders

We offer a growing portfolio of itaconate monomers and polymeric binders with performance, safety, and plant-based advantages that are key differentiators in select segments of the paints and coatings market. We are investing in products, applications, and patents to develop BIO*Asterix into proprietary business with significant long-term growth potential.

Looking ahead, we plan to use our BIO*Asterix® monomers as the foundation for a new class of competitive specialty water-based paints, targeted for introduction by the second half of 2027. We anticipate that this initial use will generate substantial revenue over several years and serve as a springboard for broader adoption of plant-based coatings over the next decade.

Absorption and odour control in hygiene

Our odour neutralisers are already demonstrating effective performance in select hygiene applications for both humans and pets. We are actively working with customers to expand their use into areas where fluid absorption using plant-based superabsorbents is also valued. Building on our prior development efforts, we have superabsorbent polymers at the pre-commercial stage that deliver performance approaching that of acrylate superabsorbents, while offering substantial cost advantage over alternative plant-based approaches, such as bio-based acrylates.

We are researching applications and evaluating commercial development routes to integrate our odour neutraliser and superabsorbent into a new generation of hygiene products. We estimate that material revenues from this work may emerge within the next five years.

Long-term revenue development

We have initiated the development of future major revenue streams beyond consumer detergents, scale inhibition, and odour neutralisation. While we anticipate a longer timeline to achieve significant traction, we are confident that our ingredients will achieve substantial adoption in paints, coatings, and hygiene applications, driven by their advantages in safety, performance, and sustainability.

Next Generation Organisation and Operations

With headcount additions and further optimisation of our production line, we now have the capacity to achieve at least $30m in revenues with our US facility. Fluctuations in US trade policy and ongoing global conflicts continue to present some risks to our supply chains.

While we have avoided major raw material cost increases from tariffs, extended shipping times and costs have required additional working capital and careful monitoring of gross profit margins. These factors also highlight the potential limitations of growing beyond $30m solely from our US operation. Early feasibility and design work began in 2025 and will continue in 2026 on scenarios and options for a potential production facility outside of the US by 2031.

At the same time, we are building our organisation with the capabilities and talent needed for the next stage of growth. In continuation of his dedication to advances in science, our co-founder Dr. Yvon Durant elected to transition from CTO to part-time Innovation Director. He will continue to lead Itaconix's new ingredient and process development efforts while pursue his passion for skiing.

John Pelech joined us in late 2024 to advance our fulfilment capabilities and was promoted to Vice President, Operations, expanding his responsibilities and leadership. After many years of collaboration with Itaconix, Dr. John Tsavalas joined as Research & Development Director from the University of New Hampshire's material science programme. Dr. Jim Gordon retired after a successful tenure building our European customer base. We are recruiting and developing a growing pool of young innovation and commercial talent, who I believe will form the core of our next stages of growth.

Outlook

We enter 2026 with strong expectations, while remaining mindful of areas of uncertainty. We are confident that our current customer base and project pipeline provide a solid foundation to meet the Board's expectations and support continued growth.

Global uncertainties continue to present new risks. However, our position to supplying ingredients for everyday consumer products, combined with reliable raw material sourcing, creates a fundamentally resilient business model. We have established strategies and resources to mitigate the risks that we do face, whilst reducing reliance on elevated inventory levels.

We expect to see significant progress in the adoption of our BIO*Asterix® specialty monomers and binders in paints and coatings, supporting both near-term development and longer-term growth potential.

Overall, our continued focus on enabling safer, better performing, and more affordable everyday consumer products has created a fundamentally resilient and high-growth business, with a clear path to positive adjusted EBITDA in 2026.

I wish to thank our employees, customers, partners and shareholders for their continued support. Their commitment and collaboration are central to our progress and position us well for the opportunities ahead. We look forward to building on this momentum in 2026 and beyond.

John R. Shaw

Chief Executive Officer

OUR STRATEGY

Principal Activities

Itaconix is a leading innovator in plant‑based specialty polymers that enhance the performance, safety, and sustainability of everyday consumer and industrial products. Our technology platform is built around itaconic acid, a naturally occurring, plant‑derived metabolite recognised for decades for its multifunctionality, safety, and ability to replace fossil‑based chemistries. Through proprietary polymerisation processes, we convert readily available itaconic acid into high‑value functional ingredients used across homecare, personal care, and industrial applications.

The Group's core activities include the development, production, and global commercialisation of these proprietary plant‑based polymers, delivered both directly to manufacturers and through strategic partners. Our ingredients provide key functional benefits-such as scale inhibition, odour neutralisation, and hair fixative performance-while enabling brands to meet rising consumer and regulatory expectations for safer, more sustainable product formulations.

Most of the Group's efforts are focused on markets where the multifunctional advantages of our polymers offer significant opportunities to replace traditional acrylic and styrene‑based materials. Building on strong commercial traction in dishwashing and laundry detergents, Itaconix continues to broaden its ingredient portfolio, including early‑stage activities in specialty monomers and binders, coatings, and other emerging applications, supported by the expansion of its BIO*Asterix® line of plant‑based building blocks.

Across all activities, our mission is to deliver high‑performance plant‑based solutions that support decarbonisation, reduce environmental impact, and enable the next generation of consumer products without requiring compromises in cost or efficacy.

Key Performance Indicators (KPIs)

The Directors believe there are financial and non-financial key performance indicators for the Group. These KPIs are critical for management's aim to monetise its technology platform through revenues generated by a growing number of commercial products. Non-financial KPIs are detailed above in the Chief Executive Officer's Statement.

Financial:

· Revenue

· Adjusted EBITDA, the earnings before interest, tax, depreciation, amortisation, share based payments, and exceptional items

· Cash

Non-financial:

· Expand European cleaning revenues with broader adoption for scale inhibition

· Re-land North American cleaning revenues for scale inhibition at attractive pricing

· Land and expand North American odour neutralisation revenues in broader home and industrial applications

· Gain initial traction for BIO*Asterix® specialty monomers and binders

Progress in 2025

In 2025, Itaconix delivered its strongest year of commercial and operational advancement, achieving significant growth across its core business segments and strengthening the foundations for near‑term EBITDA profitability. The Group reported record revenues of $10.5m, a 61% increase from 2024, driven by expanding adoption of Itaconix® Performance Ingredients and continued momentum in SPARX™ Formulated Solutions. Revenue growth was broad‑based geographically, with North America up 44%, EMEA up 104%, and progress continuing across Rest of World markets.

Gross profit rose to $3.6m, with margins stable at 35%, reflecting disciplined pricing, stable raw material costs, and improved operational efficiencies. Itaconix® Performance Ingredients delivered a weighted average margin of 41%, while SPARX™ Formulated Solutions averaged 17%, both supporting improved adjusted EBITDA, which narrowed to a loss of $0.6m, a major improvement from 2024.

BIO*Asterix® advanced from concept toward a meaningful future revenue stream as Itaconix continued developing its specialty itaconate monomers and binders. The Company produced prototype binders for specialty paint applications, completed safety studies to support upcoming US regulatory filings, and progressed a new patent covering a specific itaconate ester application. It also began selling research quantities in North America, marking the first step toward broader commercial engagement. While BIO*Asterix® did not generate revenue in 2025, these technical, regulatory, and early‑market milestones positioned the platform to become a major long‑term contributor as it moves toward commercialisation.

The Group advanced its development and commercial activities as detailed in the Chief Executive Officer's Statement. Below is a table showing the Group's key performance metrics and financial highlights:

| 2025

$'000 | 2024 (Restated) $'000 | 2023

$'000 | 2022

$'000 | 2021

$'000 |

Revenue | 10,499 | 6,503 | 7,866 | 5,600 | 2,596 |

Gross profit | 3,642 | 2,260 | 2,437 | 1,487 | 700 |

Gross profit margin | 34.7% | 34.7% | 31.0% | 26.6% | 27.0% |

Adjusted EBITDA1 | (600) | (1,778) | (925) | (1,395) | (1,640) |

Cash used from operating activities | (1,222) | (2,753) | (1,923) | (219) | (2,023) |

Net cash and investments at year-end | 4,391 | 6,734 | 10,023 | 597 | 683 |

Financial Performance

Revenue

Total revenues for the year ended 31 December 2025 were $10.5m, representing a 61% increase from 2024 revenues of $6.5m. Revenues since 2021 have a compound annual growth rate of 42%. Revenues have shown strong and consistent growth over the last 3 halves, with the last two halves having record revenues for the Group.

Revenues for the period comprised 73% from Itaconix® Performance Ingredients and 27% from SPARX™ Formulated Solutions. In efforts to most accurately reflect each of the business segments, certain revenues and costs from the sale of Itaconix® TSI 422 used in blended products sold though SPARX™ Formulated Solutions were reclassified to Itaconix® Performance Ingredients. In 2024, this amount was $0.3m in revenues and $0.2m in cost of sales, having no impact on the gross profits for the year. For additional information see note 26 to the financial statements.

North America represented 62% of the Group's revenue in 2025 (70% in 2024) and increased by 44% year-on-year. EMEA represented 38% of the Group's revenues in 2025 (30% in 2024) and increased by 104% year-on-year.

In addition to the geographic diversity, the Group had revenue concentration in three customers of 48% in 2025 compared to three customers of 40% in 2024. Revenue diversity continues to be an important focus for the Group as we grow a sustainable revenue base for future growth.

1 Adjusted for interest, tax, depreciation, amortisation, share based payment charge, and exceptional items.

2 Unaudited revenues by reporting period.

Gross profit and adjusted EBITDA1

The gross profit margin was 35% in both 2025 and 2024. During an exceptional growth period, the Group maintained attractive gross profit margins due to continued discipline in pricing strategy, stable raw materials costs, favourable foreign currency movement and improved operating efficiencies.

Itaconix® Performance Ingredients have a range of gross profits depending on the product and end market of 35% to 70% with the weighted average gross profit for 2025 of 41%, this is consistent with the weighted average gross profit for 2024 of 43%. SPARX™ Formulated Solutions have a range of 10% to 20% with a weighted average gross profit for 2025 of 17% which is slightly higher than the equivalent gross profit for 2024 which was 11%.

Adjusted EBITDA is a non-IFRS measure but is widely recognised in financial markets and it is used within the Group as a key performance indicator. Adjusted EBITDA was a loss of $0.6m in 2025 (2024: loss of $1.8m) which improved by 66%. The Group actively monitor administrative expenses and makes prudent spending decisions to support the Group's strategic objectives.

Below is a reconciliation of Loss for the Year to Adjusted EBITDA:

| 2025

$'000 | 2024 (Restated)4 $'000 | 2023

$'000 | 2022

$'000 | 2021

$'000 |

Loss after tax | (1,380) | (2,022) | (1,536) | (2,463) | (455) |

Taxation | 11 | - | 27 | 8 | 7 |

Depreciation | 165 | 120 | 194 | 161 | 167 |

Amortisation | 218 | 214 | 202 | 202 | 201 |

Share based payments | 57 | 72 | 229 | 559 | - |

Interest income | (27) | (330) | (141) | - | - |

Interest expense | 159 | 167 | 79 | - | - |

Impairment of intangible assets | 197 | ||||

Exceptional revaluation of lease liability | - | - | 21 | - | - |

Exceptional revaluation of contingent consideration | - | - | - | 138 | (1,560) |

Adjusted EBITDA | (600) | (1,778) | (925) | (1,395) | (1,640) |

Administrative expenses

Administrative expenses consist of sales, marketing, operations, research and development, and public company costs such as legal, finance and the Group Board. These expenses were $4.7m in 2025 up from $4.4m in 2024. The increase in administrative expenses was largely due to increased staffing to support the Group's growth plans.

Costs and investments

As at 31 December 2025, the Group held cash of $2.4m and investments in term deposits of $2.0m, compared to $5.4m and $1.3m, respectively as at 31 December 2024. Net cash outflows from operating activities of $1.2m in 2025 were used to support the Group's growth plan while managing working capital needs, compared to $2.7m in 2024.

Working capital

At the year end, working capital had increased as inventory readiness to support global volumes grew. Inventories increased to $3.7m in 2025 from $2.3m in 2024. The Group increased raw material inventories to support revenue growth and mitigate the risk of US tariff regimes near-term impact on gross profits. Trade and other receivables increased to $1.7m in 2025 from $1.3m in 2024. Trade and other payables increased to $2.7m in 2025 from $1.9m in 2024.

1 Adjusted for interest, tax, depreciation, amortisation, share based payment charge, and exceptional items.

4 See note 26 to the financial statements.Prior Period Adjustment related to IFRS 16: Lease Accounting

During the year, the Group identified a miscalculation of the interest expense associated with one of its lease arrangements accounted for in accordance with IFRS 16 Leases. The error related to the incorrect application of the effective interest rate method in prior periods, which resulted in an understatement of interest expense and depreciation by $157k and a corresponding understatement of the lease liability by $169k and right of use asset by $12k as at 31 December 2024. For additional information see note 26 to the financial statements.

Financial Reporting

The Group and the Company financial statements have been prepared in accordance with UK adopted International Accounting Standards ("IFRS") and the provisions of the Companies Act 2006. There were no new reporting standards adopted for the year ended 31 December 2025 that have a material impact on the financial statements.

Going Concern

The financial statements have been prepared on a going concern basis. The Directors have reviewed the Company's and the Group's going concern position taking account its current business activities, budgeted performance and the factors likely to affect its future development, set out in this Annual Report, and including the Group's objectives, policies and processes for managing its working capital, its financial risk management objectives and its exposure to credit and liquidity risks.

The Directors have also taken into consideration the current inflationary environment and geopolitical uncertainties on the Group's revenues and supply chain. While there has not been a significant negative impact during the period on the Group revenues or supply chain, the Directors have applied sensitivities to the timing, quantum, and growth of new customer projects in revenue models and have assessed alternate supply chains that have been developed by the Group to mitigate any issues in deliveries to our customers.

As further detailed in the Directors' Report on page 27 and note 2 to the financial statements, the Directors have reviewed the Group's cash flow forecasts covering a period of at least 12 months from the date of approval of the financial statements, which foresee that the Group will be able to meet its liabilities as they fall due. However, the success of the business is dependent on customers continuing to purchase our products in order to increase revenues and to reduce losses and the Directors continuing to control the Group's and the Company's cost base.

Shareholdings and Earnings per Share

Itaconix had 13,486,122 shares in issue as at 31 December 2025. The undiluted weighted average number of shares for the period to 31 December 2025 was 13,486,122. The undiluted weighted average number of shares was used to calculate the loss per share presented in note 9 to the financial statements.

PRINCIPAL RISKS AND UNCERTAINTIES

The Group operates in dynamic global markets and is exposed to a range of strategic, operational, financial, and external risks. The Directors have overall responsibility for establishing and maintaining the Group's risk management framework, while the management team is responsible for implementing controls, monitoring emerging risks, and reporting on mitigation effectiveness. Principal risks are enumerated and reviewed periodically by Management and by the Directors. The Group's risk appetite is to take on calculated and manageable risks aligned with its strategic objectives. While maintaining a low tolerance for risks that could damage its reputation or regulatory standing, the Directors are willing to accept higher levels of risk in areas that support innovation, growth and long-term value creation. As the Group continues to expand its commercial footprint in North America and EMEA, these risks evolve, driven by market conditions, supply chain factors, regulatory expectations, and macroeconomic developments.

Commercialisation Activities

The Group achieved record revenue growth this year, driven by strong customer demand across its performance ingredients and formulated solutions segments. However, the Group's ability to meet its long-term profitability goals remains dependent on growing sales volumes, managing customer ordering patterns, and maintaining momentum in new product adoption. Recent trading updates highlight both accelerated revenue growth and the expectation that growth rates may moderate compared to the exceptional increases seen in 2025.

Management of risk: The Group has sought to manage this commercialisation risk by partnering with market leaders, such as Croda, Nouryon and Brenntag, for the worldwide promotion of our leading products, continued development of end-user formulas to provide customers with packaged solutions, and continuous review of the market needs for Itaconix products.

Recruitment and Retention of Key Staff

The Group relies on experienced scientific, technical, and managerial personnel. Competition for specialty polymer chemists and skilled operations staff remains high across the global chemicals industry. Although the Group expanded its management team in 2025, attracting and retaining high-calibre personnel continues to be a risk.

Management of risk: The Group offers competitive market rates and benefits to recruit and retain top talent. Management continues to provide competitive compensation packages including benefits for employees to be an attractive employer to work for. In addition, the Group seeks to retain key personnel in the US using the Company's 2019 Equity Incentive Plan for share option grants, as disclosed in note 22 to the financial statements.

Key Persons Risk

For senior corporate management, the Group relies on three people, the Chief Executive Officer, the Chief Financial Officer and the Vice President of Operations. These people play a pivotal role in shaping the Company's vision, strategy, and operations. The Board recognises the importance of mitigating key person risk to ensure the long-term stability of the Company.

Management of risk: The Group has negotiated and is negotiating executive and senior management employment agreement with certain key employees and uses the 2019 Equity Incentive Plan for share option grants, not only for incentivisation but also to encourage retention. The Board is developing contingency plans to address unforeseen circumstances, as well as succession planning, to ensure that the Company remains resilient and well-positioned for sustainable growth.

Customer Concentration and Retention

The ability to retain key customers at attractive gross profit margins is critical to maintaining revenue streams. The loss of key customers or excessive dependence on a limited number of customers could impact business results adversely.

Management of risk: We engage with the product managers and formulators, either directly or through contract manufacturers, to create consumer products that achieve desired performance claims and overall costs. During the process, we monitor the estimated value of our ingredients in the end-product formulations and price our ingredients relative to competitive alternatives. The revenues for a particular ingredient are often concentrated in a few customers in the early commercial stages. As we introduce more products and these products enter new phases of growth, we are seeking to diversify our customer base and to more consistently achieve pricing that reflects the value of our ingredients in the end-product formulations.

Regulatory, Legislation and Environmental Impact

Sustainability expectations continue to rise across global consumer, industrial, and regulatory environments. Customers, retailers, and regulators increasingly require low‑carbon, non‑persistent, bio‑based ingredients. Itaconix's polymers directly support these demands, but evolving regulatory requirements necessitate robust documentation and ongoing research and development investment.

Management of risk: The value of Itaconix products starts with their safety and environmental profile. The Group closely monitors the evolving requirements for substantiating these profiles and regularly conducts technical studies to reinforce and extend the safety and environmental claims of Itaconix ingredients.

Competition and Technology

The production and use of Itaconix polymers are subject to technological change over time. There can be no assurance that developments by others will not render the Group's product offerings and research activities obsolete or otherwise uncompetitive.

Management of risk: The Group employs experienced and highly-trained polymer chemists to develop and protect the Group's intellectual property. These efforts include continuous work on the performance and cost advantages of Itaconix polymers. In addition, the staff monitors technologies and patents through publications, scientific conferences, and collaborations with other organisations to identify new risks and opportunities.

Manufacturing Risk

Itaconix has one production facility in North America, that supports the Group's revenues. Key raw materials are sourced globally which can result in an extended supply chain.

Management of risk: The Group holds additional finished goods and raw material inventories off site at a warehouse in North America and another in Europe. Suppliers also hold additional raw materials in North America.

Liquidity Risk

Itaconix seeks to manage financial risk by ensuring adequate liquidity is available to meet foreseeable needs and to invest cash assets safely and profitably. In addition, short-term flexibility is achieved by holding significant cash balances in Itaconix's functional currencies, notably UK Sterling and US Dollars.

Management of risk: The Group monitors bank balances held in established financial institutions and maintains adequate cash balances in its functional currencies.

Credit Risk

The principal credit risk for Itaconix arises from its trade receivables. To manage credit risk, new customers are subject to credit review and all customer accounts are regularly reviewed for debt aging and collection history. As at 31 December 2025, there were no significant credit risk balances.

Management of risk: The Group's control environment requires new customers to establish credit terms through providing credit references and a credit review. Trade receivables are actively monitored for collection history.

Inflation and Foreign Currency Risk

Raw material and logistics costs have stabilised compared to prior years; however, inflationary pressures remain across global markets. Selling prices to international customers increased during 2025, and the Group continues to manage exposure arising from multi‑currency transactions.

Management of risk: The Group actively monitors raw material costs and works with vendors to manage these costs. Costs increases are periodically passed onto customers through pricing increases. The Group also has the ability to receive various foreign currencies in bank accounts and convert them as market conditions are favourable.

Foreign Exchange Risk

Itaconix is a holding company publicly traded on the London Stock Exchange. The Group's primary operations are in the US. These US based operations transact trades with customers in North America and internationally. Revenue and costs are exposed to variations in exchange rates and therefore reported losses. In 2019, the Group elected to convert the reporting currency from UK Sterling to US Dollars. The US Dollar transactions represent a significant portion of the functional currency transactions and therefore reduce the Group's overall exposure to translation exchange risk.

Management of risk: The Group manages foreign exchange risk by maintaining bank balances in major functional currencies to control the impact on transaction costs for operational expenses. The Group will continue to monitor the appropriateness of reporting in US Dollars.

Government and Geopolitical Risk

The Group has potential exposure to government activities related to US-Europe and US-China trade relations and geopolitical risk, such as through the procurement and import of itaconic acid from China, and the sale of products to Europe and Canada. Trade tensions have led to fluctuating tariff regimes that impact the costs of raw materials, production, distribution, and sales. The imposition of tariffs on chemicals and specialty ingredients can increase costs for both manufacturers and end customers, potentially affecting demand and competitive positioning. This can have a negative impact but in certain cases can also improve our competitive position relative to other products. Tariffs or sudden policy shifts may also create supply chain disruptions, forcing companies to adjust sourcing strategies or seek alternative suppliers, often at higher costs. Limited availability and extended delivery times may also trigger increases of raw material or product costs and may continue to cause volatility.

Management of risk: The Group actively monitors global trade policies and tariff developments to assess potential cost impacts and mitigate supply chain risks. The Group also actively monitors raw material sourcing, particularly of itaconic acid and the impact it could have on the Group's products. It works with current suppliers on raw materials pricing and mitigating the impact of tariffs on the pricing of the Group's products. Additionally, the Group stays informed on potential trade developments and advocates for policies that support fair and predictable market conditions. By proactively managing these risks, the Group aims to maintain cost efficiency and supply chain stability while continuing to serve its customers competitively.

Cyber and Information Risk

There is a growing risk of fraudulent attacks on the business, such attack could have the potential to significantly disrupt the Group's operations and result in loss to the business.

Management of risk: The Group monitor IT systems in place to ensure they are up to date and regularly updated with the latest security protection.

SECTION 172 STATEMENT

Statement of Compliance with Section 172 of the Companies Act 2006

The Directors are required to include a separate statement in this Annual Report that explains how they have considered broader stakeholder needs when performing their duty under Section 172(1) of the Companies Act 2006. This duty requires that a director of a company must act in the way he or she considers, in good faith, would be most likely to promote the success of the company for the benefit of its members as a whole, and in doing so have regard (amongst other matters) to:

· The likely consequences of any decision in the long term;

· The interests of the company's employees;

· The need to foster the company's business relationships with suppliers, customers, and others;

· The impact of the company's operations on the community and the environment;

· The desirability of the company to maintain a reputation for high standards of business conduct; and

· The need to act fairly between members of the company.

In connection with its statement, the Board describes in general terms how key stakeholders, as well as issues relevant to key decisions are identified, and also the processes for engaging with key stakeholders including customers, employees and suppliers, and understanding those issues. It is the Board's view that these requirements are predominantly addressed in the corporate governance disclosures made in the Directors' Report, which are themselves discussed more extensively on the Group's website.

A more detailed description is limited to matters that are of strategic importance in order to remain meaningful and informative for shareholders. The Board believes that two decisions taken during the year fall into this category, and engaged with appropriate internal and external stakeholders on these decisions, where applicable:

· QCA Code Review and Updates: the Directors evaluated and implemented the Company's ongoing compliance with the Quoted Companies Alliance Corporate Governance Code, including enhancements to governance processes, risk management systems, and transparency. Stakeholder expectations, including those of investors and regulators, were central to these deliberations;

· Shareholder "Say on Pay" Considerations: the Directors reviewed executive remuneration structures with specific attention to shareholder feedback, alignment with performance objectives, and market standards. The Board sought to ensure that remuneration policies continued to support long‑term value creation while maintaining fairness and transparency.

CONSOLIDATED INCOME STATEMENT

For the year ended 31 December 2025

| Notes | 2025

$'000 | 2024 (Restated) $'000 |

Revenue | 2 | 10,499 | 6,503 |

Cost of sales | (6,857) | (4,243) | |

Gross profit | 3,642 | 2,260 | |

Administrative expenses | (4,682) | (4,445) | |

Operating loss before exceptional items | (1,040) | (2,185) | |

Impairment of intangible assets | (197) | - | |

Operating loss before tax from operations | (1,237) | (2,185) | |

Finance income | 27 | 330 | |

Interest expense | (159) | (167) | |

Loss before tax | (1,369) | (2,022) | |

| |||

Taxation charge | (11) | - | |

Loss after tax | (1,380) | (2,022) | |

Basic loss per share ¢ | (0.10)¢ | (0.15)¢ | |

Diluted loss per share ¢ | (0.10)¢ | (0.15)¢ |

CONSOLIDATED STATEMENT OF OTHER COMPREHENSIVE INCOME

For the year ended 31 December 2025

|

|

| 2025

| 2024 (Restated) | |||

| Notes | $'000 | $'000 | ||||

Loss for the year |

| (1,380) | (2,022) | ||||

Items that will be reclassified subsequently to profit or loss |

|

| |||||

Exchange gain in translation of foreign operations |

| 381 | (98) | ||||

Total comprehensive loss for the year |

| (999) | (2,120) | ||||

Attributable to: |

|

| |||||

Equity holders of parent |

| (999) | (2,120) | ||||

CONSOLIDATED BALANCE SHEET

At 31 December 2025

|

| 31 Dec | 31 Dec |

| ||

|

| 2025 | 2024 |

| ||

|

|

| (Restated) |

| ||

| Notes |

| $'000 | $'000 |

| |

Non-current assets |

| |||||

Intangible assets |

| 237 | 244 | |||

Property, plant and equipment |

| 1,067 | 584 |

| ||

Right-of-use assets |

| 1,854 | 2,035 |

| ||

Investment in subsidiary undertakings |

| - | - |

| ||

| 3,158 | 2,863 |

| |||

|

|

|

| |||

Current assets |

|

|

| |||

Inventories |

| 3,717 | 2,312 |

| ||

Trade and other receivables |

| 1,691 | 1,281 |

| ||

Investments |

| 2,020 | 1,252 |

| ||

Cash and cash equivalents |

| 2,371 | 5,482 |

| ||

| 9,799 | 10,327 |

| |||

|

|

|

| |||

Total assets |

| 12,957 | 13,190 |

| ||

|

|

|

| |||

Financed by |

|

|

| |||

Equity shareholders' funds |

|

|

| |||

Equity share capital |

| 8,665 | 8,665 |

| ||

Equity share premium |

| 58,012 | 58,012 |

| ||

Own shares reserve |

| (5) | (5) |

| ||

Merger reserve |

| 31,343 | 31,343 |

| ||

Share based payment reserve |

| 1,001 | 944 |

| ||

Foreign translation reserve |

| 712 | 331 |

| ||

Retained deficit |

| (91,494) | (90,114) |

| ||

Total equity |

| 8,234 | 9,176 |

| ||

|

|

| ||||

Non-current liabilities |

|

|

| |||

Lease liabilities |

| 1,862 | 1,991 |

| ||

|

| 1,862 | 1,991 |

| ||

|

|

|

| |||

Current liabilities |

|

|

| |||

Trade and other payables |

| 2,699 | 1,876 |

| ||

Lease liabilities |

| 162 | 147 |

| ||

| 2,861 | 2,023 |

| |||

|

| |||||

Total liabilities |

| 4,723 | 4,014 |

| ||

|

|

|

| |||

Total equity and liabilities |

| 12,957 | 13,190 |

| ||

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

At 31 December 2025

| Equity share capital | Equity share premium | Own shares reserve | Merger reserve | Share based payment reserve | Foreign translation reserve | Retained deficit (Restated) | Total | |

$'000 | $'000 | $'000 | $'000 | $'000 | $'000 | $'000 | $'000 | ||

At 1 January 2024 | 8,665 | 58,012 | (5) | 31,343 | 872 | 429 | (88,092) | 11,224 | |

Loss for the year | - | - | - | - | - | - | (2,022) | (2,022) | |

Exchange differences on translation of foreign operations | - | - | - | - | - | (98) | - | (98) | |

Share based payments | - | - | - | - | 72 | - | - | 72 | |

At 31 December 2024 (restated) | 8,665 | 58,012 | (5) | 31,343 | 944 | 331 | (90,114) | 9,176 | |

Loss for the year | - | - | - | - | - | - | (1,380) | (1,380) | |

Exchange differences on translation of foreign operations | - | - | - | - | - | 381 | - | 381 | |

Share based payments | - | - | - | - | 57 | - | - | 57 | |

At 31 December 2025 | 8,665 | 58,012 | (5) | 31,343 | 1,001 | 712 | (91,494) | 8,234 | |

CONSOLIDATED STATEMENT OF CASH FLOWS

For the year ended 31 December 2025

| Group |

| Group | ||||||

|

|

| 2025 | 2024 | |||||

|

|

|

| (Restated) | |||||

|

| $'000 | $'000 | ||||||

Net cash outflow from operating activities |

|

| (1,222) ------ | (2,753) - ------ | |||||

Interest received |

|

| 27 | 330 | |||||

Purchase of securities |

|

| (768) | - | |||||

Deposit of securities |

|

| - | 6,204 | |||||

Purchase of property, plant and equipment |

|

| (630) | (363) | |||||

Development of website |

|

| - | (27) | |||||

Capitalisation of development costs |

|

| (208) | (197) | |||||

Cash loaned to subsidiary undertakings |

|

| - | - | |||||

Net cash (outflow) / inflow from investing activities |

|

| (1,579) | 5,947 | |||||

Repayment of lease liability |

|

| (310) | (279) | |||||

Net cash outflow from financing activities |

|

| (310) | (279) | |||||

Net (outflows) / inflow in cash and cash equivalents |

| (3,111) | 2,915 | ||||||

Cash and cash equivalents at beginning of year |

|

| 5,482 | 2,567 | |||||

Cash and cash equivalents at end of year |

|

| 2,371 | 5,482 | |||||

NOTES TO THE FINANCIAL INFORMATION

1. Accounting policies

Basis of presentation

The financial information set out in this document does not constitute the Group's statutory accounts for the years ended 31 December 2024 or 2025. Statutory accounts for the years ended 31 December 2024 and 31 December 2025, which were approved by the directors on 23 March 2026, have been reported on by the Independent Auditors. The Independent Auditor's Reports on the Annual Report and Financial Statements for 2024 or 2025 was unqualified and unmodified and neither year did not contain a statement under 498(2) or 498(3) of the Companies Act 2006.

Statutory accounts for the year ended 31 December 2024 have been filed with the Registrar of Companies. The statutory accounts for the year ended 31 December 2025 will be delivered to the Registrar of Companies in due course and will be posted to shareholders on 24 March 2026, and thereafter will be available from the Group's registered office at Fieldfisher Riverbank House, 2 Swan Lane, London, United Kingdom, EC4R 3TT and from the Group's website https://itaconix.com/investor/reports-documents/

The financial information set out in these results has been prepared using the recognition and measurement principles of International Accounting Standards, International Financial Reporting Standards and Interpretations in accordance of UK adopted International Accounting Standards ('IFRS'). The accounting policies adopted in these results have been consistently applied to all the years presented and are consistent with the policies used in the preparation of the financial statements for the year ended 31 December 2024, except for those that relate to new standards and interpretations effective for the first time for periods beginning on (or after) 1 January 2025. There are deemed to be no new standards, amendments and interpretations to existing standards, which have been adopted by the Group, that have had a material impact on the financial statements.

The Group's financial information has been presented in US Dollars (USD).

Going concern

The financial statements have been prepared on a going concern basis. The Directors have reviewed the Parent Company's and the Group's going concern position taking account its current business activities, budgeted performance and the factors likely to affect its future development, set out in the Annual Report, and including the Group's objectives, policies and processes for managing its working capital, its financial risk management objectives and its exposure to credit and liquidity risks.

The Group made a loss for the year of $1.4m, had Net Operating Assets at the period end of $8.0m and a Net Cash Outflow from Operating Activities of $1.2m. Primarily, the Group meets its day to day working capital requirements through existing cash resources and had on hand cash, cash equivalents and investments at the balance sheet date of $4.4m.

The Directors have reviewed the Group's cash flow forecasts covering a period of at least 12 months from the date of approval of the financial statements, which foresee that the Group will be able to meet its liabilities as they fall due. However, the success of the business is dependent on customers continuing to purchase the Group's products in order to increase revenue and profit growth and continuing to control the Group and Parent Company's cost base.

The Directors believe that, taken as a whole, the factors described above enable the Parent Company and Group to be and continue as a going concern for the foreseeable future. The financial statements do not include the adjustments that would be required if the Parent Company and the Group were unable to continue as a going concern.

2. Revenue

Revenue recognised in the Group income statement is analysed as follows:

Geographical information

Revenues |

| Net assets | ||||||||||

2025 | 2024 |

| 2025 | 2024 |

| |||||||

$'000 | $'000 |

| $'000 | $'000 |

| |||||||

|

|

|

|

|

|

|

| |||||

North America | 6,537 | 4,555 |

| 4,266 | 2,990 |

| ||||||

Europe, Middle East and Africa | 3,962 | 1,938 |

| 4,212 | 6,343 |

| ||||||

Rest of World | - | 10 |

| - | - |

| ||||||

10,499 | 6,503 | 8,478 | 9,333 |

| ||||||||

The revenue information is based on the location of the customer. Net assets of the Group (being total assets less total liabilities) are attributable to geographical locations.

Segment information

The Group has four business segments. Itaconix® Performance Ingredients develops, produces and sells proprietary specialty polymers that are used as functional ingredients to meet customers' needs in cleaning, beauty and hygiene products. SPARX™ Formulated Solutions provides technical services and ingredient supplies for formulated products developed for customers based on Performance Ingredients. BIO*Asterix® develops, produces, and sells specialty itaconate monomers as a plant-based alternatives to acrylates and styrenes in paint, coating, and adhesive applications. These segments make up the continuing operations. Core Operations include development expense, general and administrative expense, professional fees, and governance costs to progress and grow the Groups operations.

| Itaconix® Performance Ingredients | SPARX™ Formulated Solutions | BIO*Asterix® | Core Operations | 2025 |

$'000 | $'000 | $'000 | $'000 | $'000 | |

|

|

| |||

Revenue |

|

|

| ||

Sale of goods | 7,638 | 2,861 | - | - | 10,499 |

Results: |

| ||||

Depreciation and amortisation | (185) | - | - | - | (185) |

Cost of sales | (4,294) | (2,378) | - | - | (6,672) |

Gross profit | 3,159 | 483 | - | - | 3,642 |

Administrative expense | - | - | - | (4,682) | (4,682) |

Impairment of intangible assets | - | - | - | (197) | (197) |

Other income | - | - | - | 27 | 27 |

Interest expense | - | - | - | (159) | (159) |

Taxation charge | - | - | - | (11) | (11) |

Segment performance | 3,159 | 483 | - | (5,022) | (1,380) |

Operating assets | 6,541 | 814 | 18 | 5,347 | 12,720 |

Operating liabilities | (2,807) | (523) | - | (1,393) | (4,723) |

Other disclosure: |

| ||||

Capital expenditure* | 116 | 207 | - | 307 | 630 |

| Itaconix® Performance Ingredients | SPARX™ Formulated Solutions | Core Operations | 2024 |

(Restated) | (Restated) | (Restated) | (Restated) | |

$'000 | $'000 | $'000 | $'000 | |

| ||||

Revenue |

| |||

Sale of goods | 4,773 | 1,730 | - | 6,503 |

Results: | ||||

Depreciation and amortisation | (203) | - | - | (203) |

Cost of sales | (2,502) | (1,538) | - | (4,040) |

Gross profit | 2,068 | 192 | - | 2,260 |

Administrative expense | - | - | (4,445) | (4,445) |

Other income | - | - | 330 | 330 |

Interest expense | - | - | (167) | (167) |

Taxation charge | - | - | - | - |

Segment performance | 2,068 | 192 | (4,282) | (2,022) |

Operating assets | 5,493 | 276 | 5,913 | 11,682 |

Operating liabilities | (2,420) | (237) | (1,188) | (3,845) |

Other disclosure: |

| |||

Capital expenditure* | 57 | - | 305 | 362 |

*Capital expenditure consists of additions of property, plant and equipment.

Customer concentration information

The Group has revenue concentration in three customers of 48% (2024: 40%).

3. Loss per share

Basic loss per share is calculated by dividing the loss attributable to ordinary shareholders by the weighted average number of ordinary shares in issue during the year.

| 2025 | 2024 | ||

|

| (Restated) | ||

Loss | $'000 | $'000 | ||

|

| |||

Loss for the purposes of basic and diluted loss per share | (1,379) | (2,022) | ||

Weighted average number of ordinary shares for the purposes of basic and diluted loss per share ('000) | 13,486 | 13,486 | ||

Basic and diluted loss per share | (10.2)¢ | (15.0)¢ | ||

Basic and diluted loss per share (post consolidation comparison) | (10.2)¢ | (15.0)¢ |

The loss for the period and the weighted average number of ordinary shares for calculating the diluted earnings per share for the period to 31 December 2025 are identical to those used for the basic earnings per share. This is because the outstanding share options would have the effect of reducing the loss per ordinary share and would therefore not be dilutive.

4. Cautionary Statement

This document contains certain forward-looking statements relating to Itaconix plc (the "Group"). The Group considers any statements that are not historical facts as "forward-looking statements". They relate to events and trends that are subject to risk and uncertainty that may cause actual results and the financial performance of the Company to differ materially from those contained in any forward-looking statement. These statements are made by the Directors in good faith based on information available to them and such statements should be treated with caution due to the inherent uncertainties, including both economic and business risk factors, underlying any such forward-looking information.

Related Shares:

Itaconix Plc